Aug

2023

Addressing water storage gap

DIY Investor

20 August 2023

Water availability is key to life but is increasingly under stress. Worsening droughts globally, aging water infrastructure and rising imbalances between water supply and demand are resulting in significant pressures on populations, industrial activities, and the agricultural sector to sustain the population by Christian Zilien | Andreas Fruschki

Key Takeaways

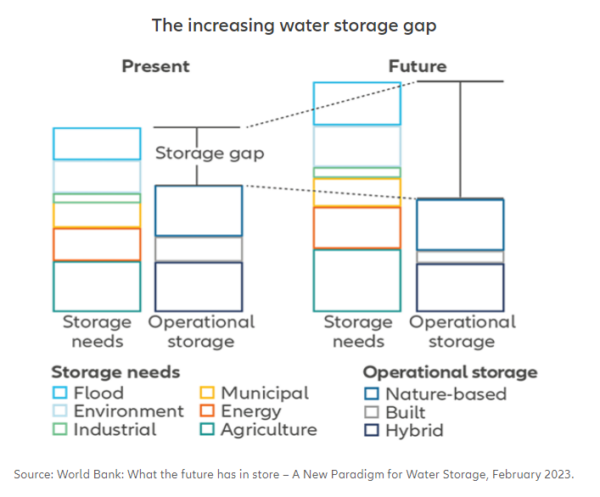

- Water storage is vital to protecting water availability against water scarcity

- Over the last fifty years natural water storage globally decreased by around 27,000 billion m³ 1

- Investments along the whole water-storage value chain can help to address water scarcity and associated hydropower challenges

To mitigate the impact of water stress, sustainable water supply and water storage solutions are needed that help enhancing water availability in water-scarce times.

Water storage, a critical cornerstone to water security

- Meeting different and evolving needs from the population and industry in drier periods

- Supporting Hydropower, which is the largest renewable energy source by capacity and generation

- Reducing the environmental and social risks from floods

- Ensuring waterway transport access through all seasons

Considering the benefits delivered by water storage to communities, businesses, and regions, it’s crucial to preserve and improve existing natural water storage (aquifers, lakes, wetlands) as well as to invest in the modernisation and development of built water storage systems.

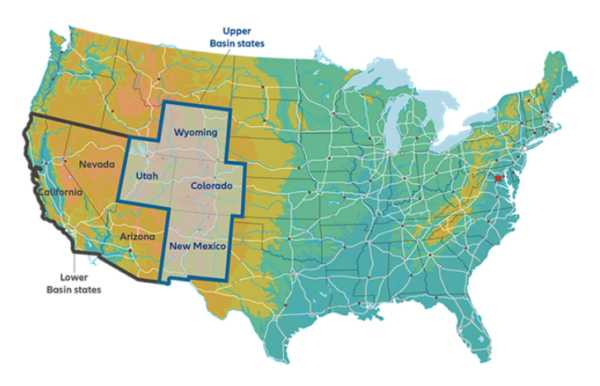

The Colorado River basin: a giant water storage in peril

Seven US states are highly dependent on the Colorado River, an already over-used waterway, and recently reached an agreement to cut consumption and help to save a stream that:

- provides drinking water for more than 40 million people

- is an irrigation resource for some of the country’s most important farmlands2

- creates hydropower for eight surrounding states.

- generates (approximately corresponding to the water needed to fill 6 million Olympic-sized swimming pools) around USD 60 billion per year in crops and livestock3

Under this agreement, the Inflation Reduction Act launched by the Biden Administration will compensate Colorado River Basin water districts, cities and indigenous communities with USD 1.2 billion for conserving 3 million acre-feet of water (corresponding approximately to the water necessary to fill 6 million Olympic-sized swimming pools) until 2026.4

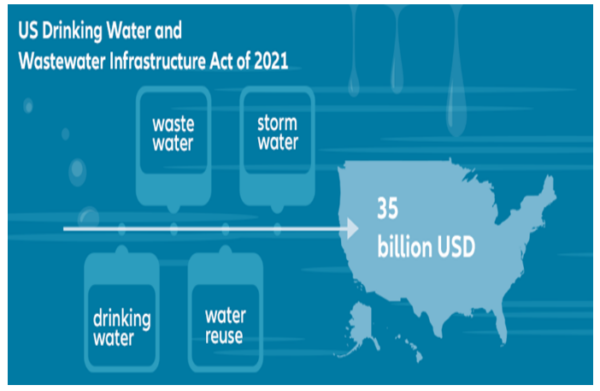

Overall, over USD 10 billion of Inflation Reduction Act funds are being directed at water, including drought relief, flood mitigation and climate resiliency of the domestic US water infrastructure. While USD 10 billion for water is great, especially in the context of more than 90 billion the U.S. government allocated for water through the Bipartisan Infrastructure Law (2021) and the Drinking Water and Wastewater Infrastructure Act (2021), it is important to get further evidence that water is finally getting the necessary attention it deserves.

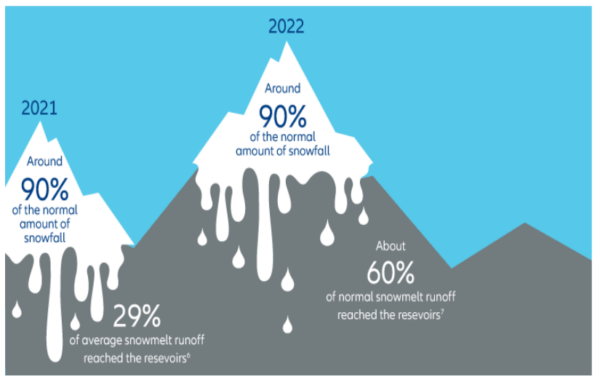

The recently accorded deal comes at the right time. The Colorado River basin has suffered a two-decades-long drought period5 while the drastically shrunken average snow runoff is accelerating the lowering of the river’s as well as of Lake Powell’s and Lake Mead’s – the two major reservoirs in the Colorado River basin – water levels.

Water storage issues’ impact on hydropower

This alarming development has far-reaching consequences as the river system is not only supplying water to the surrounding communities but is also a key economic factor for the region accounting for USD 1.4 trillion of the annual U.S. economy and supporting 16 million jobs in several neighbouring states8. Additionally, a drying-out of the Colorado River basin would very probably also have a significant impact on electricity and water bills which could increase at the same rate as water levels fall. Once the reservoirs’ hydropower capacities decrease while electricity demand is growing uninterruptedly, the region will have to examine building infrastructure for alternative renewable power sources, like solar and wind.

It’s worth noting that currently the Hoover Dam at Lake Mead and the Glen Canyon Dam at Lake Powell supply hydropower for around 4 million residents in the seven basin states.9

Looking at the implications of decreasing stream flows and shrinking reservoir levels not only in the Colorado River basin, from an US-level perspective it’s also worth mentioning that the hydropower share of total U.S. renewable electricity generation is currently at 28.7% and at around 6.2% of total U.S. electricity generation.10

Under these circumstances it becomes even more urgent that additional financial flows are redirected to the restoration of existing and the further build out of new hydropower capacities.

Investing across the entire water storage value chain

Comprehensively addressing water storage issues means going beyond feasible quick wins like fixing leakages in water tanks, freeing water storage from sediment deposits, managing the transportation of water from reservoirs to people and businesses, and addressing the lifecycle of water storage – though these measures are, of course, indispensable for ensuring a sufficient water supply.

Looking at sustainable water management from a broader and systematic perspective implies the identification of innovators and enablers along the entire value chain. This ranges from technologies that help to understand, monitor and preserve aquifers, wetlands and other natural water storage where the majority of freshwater is stored, to companies that design built water storage tailored to specific climate, local or regional requirements. Indeed, minimising the environmental impact and maximising the efficiency and variability of reservoirs is vital.

Not least, integrated solutions to combine natural, hybrid and built storage capacities and harmonise their differing dynamics are needed to follow a holistic approach to sustainably manage and restore existing and build new water storage capabilities.

1 JP Morgan Asia Credit Index (JACI) as at 31 March 2023

2 World Economic Outlook, April 2023: A Rocky Recovery (imf.org).

3 JP Morgan Asia Credit Index (JACI) as at 31 March 2023.

4 JP Morgan Asia Credit Index (JACI) as at 31 March 2023.

5 EBITDA – earnings before interest, taxes, depreciation, and amortisation – is a widely used measure of cash profit derived from a firm’s core operations.

6 JP Morgan, AllianzGI as at 31 March 2023.

7 The Liquidity Coverage Ratio (LCR) is a measure of banks’ short-term liquidity which measures a bank’s unencumbered high quality liquid assets relative to the net cash outflows it could encounter under a severe 30-day stress scenario.

8 Moody’s as at 31 March 2023.

9 Fitch Ratings as at 31 December 2022.

10 JP Morgan, AllianzGI as at 31 March 2023.

11 China’s looming property crisis threatens economic stability | PIIE

![]()

Leave a Reply

You must be logged in to post a comment.