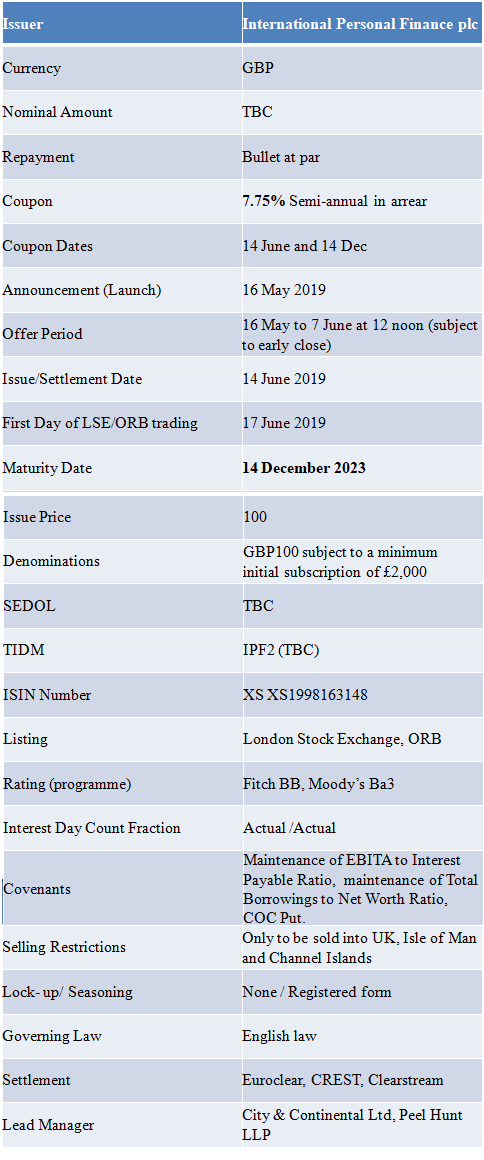

International Personal Finance Retail Bond – 7.75% Due 2023

International Personal Finance

Provider of home credit and digital lender International Personal Finance (IPF) is offering DIY investors a rare opportunity with a new retail bond offering an eye-catching coupon of 7.75% p.a.

The bonds will be traded on the LSE’s Order Book for Retail Bonds – ORB – exchange and will pay interest twice a year until the bonds are redemption at their issue price in December 2023.

A minimum investment of £2,000 is required with multiples of £100 thereafter; the offer period is now open and whilst it is planned to close on June 7th, experience tells that significant demand from investors can see that offer period shortened.

Describing itself as a ‘home credit service’ for people ‘who want to borrow money quickly and in a manageable and transparent way’, International Personal Finance (IPF) operates in Poland, the Czech Republic, Slovakia, Hungary, Mexico and Romania, and offers short-term cash loans of £50 to £1,000 as well as a home collection service.

IPF is FTSE 250 listed and was floated on the London Stock Exchange in July 2007; it has 2.4 million customers and more than 7,000 employees.

As described in a series of articles on Retail Bond Expert, IPF previously issued a retail bond offering 6.125% in 2013, and subsequently topped it up:

IPF hopes for high level of interest with 6.125% Retail Bond launch

IPF retail bond closes early at top end of expectation

A Loan Again, Naturally? IPF Seeks to Repeat 6.125% Retail Bond Success

The deal is open to new investment, with holders of the existing IPFLN6.125% 2020 offered the opportunity to extend into the new bond by offering a par-par switch with a fee payable of 1.5% to those extending their bonds. Rolling the fee into the price, this would be equivalent to exiting on a yield of 4.51% and locking in to 7.75% for the new four-and-half year bond.

The bonds are from the existing programme, senior unsecured and pari-passu with other debt; the expected rating is BB (Fitch) and BBa3 (Moody’s)

With the London Capital & Finance issue still raw, retail bonds are listed on the stock exchange and are considered to be safer than mini-bonds, which are unlisted and unregulated. However, investors’ money is not fully safe even with retail bonds as they are not covered by the Financial Services Compensation Scheme.

Michael Dyson of BondCap, a specialist bond provider, said the bond was not without its risks but its high interest rate was attractive.

Only a few new retail bonds have been offered to private investors in recent years; in July 2018 Regional Reit, an investment trust, issued a bond paying 4.5% and charity Belong listed a 4.5% to help fund dementia care and the construction of retirement villages.

Further details can be found in the prospectus, the supplementary prospectus, the cash offer document and the information booklet and are summarised hereunder:

To subscribe to this offer:

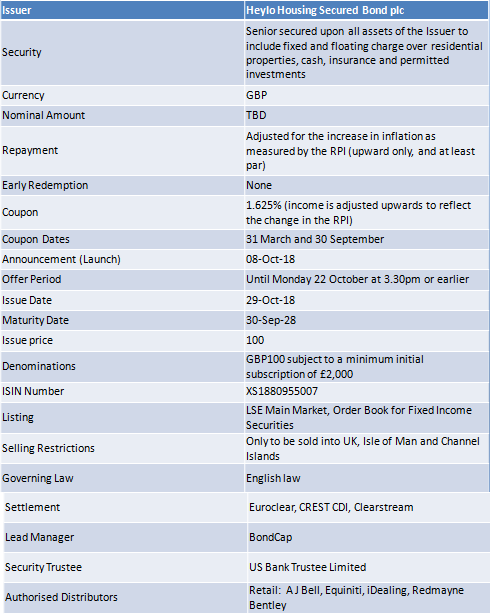

Heylo Housing

CLOSED

Unique inflation protected retail bond set to appeal to income investors comes with potential for long term capital growth with interest and redemption payments linked to RPI.

Heylo Housing Group Ltd is a residential property company with a long term investment strategy to provide affordable housing across the UK; the specialist in part buy – part rent residential properties, has announced the launch of a secured sterling bond via its wholly owned subsidiary Heylo Housing Secured Bond plc.

It is well worth investors spending some time to understand this offer becasuse the bonds have a structure that is unique in the sterling retail bond market in that over its ten year term the bonds will pay interest semi-annually at a real rate of interest of 1.625% per annum, adjusted to take account of changes in the level of the UK Retail Prices Index (RPI); protection from inflation is likely to prove attractive to those looking to protect their investments and any capital appreciation very welcome.

Interest will be paid semi-annually on 31st March and 30th September in each year starting 31st March 2019.

Ordinarily a bond pays a fixed coupon for its duration and the original loan will be repaid at ‘par’ – £100 nominal – per bond.

It is the nature of its coupon payments and its nominal value that make this bond unique; put simply, the coupon and the face value of the bonds may go up if there is inflation during the ten year term, but there are safeguards in place to ensure that you do not receive less than the initial interest rate, and do not receive less than the face value of the bond.

In this way the Heylo bond appears to enhance the core features that have made retail bonds so popular with investors – regular income payments and the return of the initial loan in full at the end of the term agreed.

‘the Heylo bond appears to enhance the core features that have made retail bonds so popular with investors’

Technically, the bonds are described as ‘limited’ in that that the adjusted nominal value and the income paid to investors, increases without limits during periods of inflation but is protected from decreases during periods of deflation.

Any adjustments to the income and redemption value are upward only, therefore on maturity the amount repayable to investors will be no less than the full value of the bonds, adjusted upwards if there has been inflation during the term of the bonds; in the vernacular, the bonds have potentially ‘unlimited upside’, but no ‘downside’.

The bonds form part of Heylo Housing Secured Bond plc’s Euro Medium Term Note Programme and are expected to be listed on the Official List of the UK Listing Authority and to trade on the London Stock Exchange’s Order Book for Fixed Income Securities (‘OFIS’) on 29th October 2018.

- The bonds have a minimum initial subscription amount of £2,000 and are available in multiples of £100 thereafter.

- The offer period is now open and is expected to close at or before 15.30hrs on 22nd October 2018; the issuer retains the right to close the offer early.

- During the life of the bonds, investors may sell them at any time (within market hours and in normal market conditions) on the open market through their stockbroker.

- Best bought within an ISA or SIPP wrapper as the RPI element is treated as income.

Heylo’s business generates low volatility, RPI linked cash flow which allows it to offer inflation matching investments with an enhanced risk return profile; it may not be the easiest concept at first glance, but is likely to tick a lot of boxes for those targeting long term income and capital growth potential.

The homes are covered by fully repairing and insuring leases and bondholders have first ranking security over the properties.

In announcing the issue Chris Hewitt, Chief Financial Officer, said:

‘We’re delighted to announce the launch of our first retail eligible bond. Demand for affordable housing continues to intensify and we see a significant opportunity to grow our portfolio of occupied, part buy – part rent residential properties.

We believe that the low volatility, long term and inflation-linked cash flows generated by this attractive asset class, enable us to offer investors stable returns protected against inflation, with no deflation risk. We intend to deploy the proceeds of the bonds quickly and build on our strong track record of growing the portfolio and providing greater access to affordable home ownership.’

The Authorised Offerors are:

AJ Bell Securities Limited

iDealing.com

Limited NCL Capital Markets, a registered trading name of King & Shaxson Limited (Institutional investors only)

Redmayne-Bentley LLP

RIA Capital Markets Limited (Institutional investors only)

Saga Personal Finance

Selftrade

Shareview

Winterflood Securities Limited (Institutional investors only)

About the Heylo Group

The Heylo Group was established in 2014 with the dual ambition of providing greater access to affordable home ownership, at the same time as providing inflation-linked returns, secured against residential property, for investors seeking to mitigate inflation risk.

It now has a portfolio to over 1,650 part buy – part rent residential properties worth in excess of £300 million and has a further 1,300 properties already under contract.

Part buy – part rent (sometimes ‘shared ownership’) is a type of affordable home ownership which allows the purchaser to buy a share in a property, while paying rent on the non-purchased share.

In 2016, in response to the significant level of public demand, the government announced a £4.1 billion grant funding programme, the Shared Ownership and Affordable Homes Programme 2016 to 2021 to deliver a further 135,000 such homes, a four-fold increase in annual delivery.

The Heylo Group employs multiple routes to grow its portfolio, predominantly through its strong relationships with over 50 house builders acquiring the affordable homes made available as part of planning obligations.

It also enables customers registered with Help to Buy to purchase existing properties in the second-hand market on a part buy – part rent basis; the company has a significant pipeline of investment opportunities with national and regional house builders and the issuer will use the proceeds of the bonds to grow a portfolio of part buy – part rent residential properties, occupied on 125-year leases with contractual, long term, inflation-linked rents with annual, upwards only reviews.

Some Context

Statistics in support of its business are strong – 86% of people say they want to get on the housing ladder but just 25% of under-35s manage to do so.

2.5 million private renters want to be part-owners – Heylo customers can buy between 25% – 75% of a property, and can increase their share at any time; most would save money when compared with renting, and would benefit from any increase in the value of their property.

Heylo has extensive and active stakeholder relationships with a who’s who of UK house builders and 8 of the top 10 are repeat partners – inter alia, Bovis Homes, Redrow, Barratt Homes, Taylor Wimpey and Persimmon; it has previously issued inflation linked long dated institutional bonds.

In its 2015 manifesto the Conservative party pledged to deliver increased affordable home ownership including 120,000 Help to Buy and 200,000 starter homes; currently supply is far outstripped by demand with more than 200,000 pre-approved buyers on waiting lists.

To subscribe to this offer visit:

IPO/Issue 3

DIY Investor brings you the latest issues, launches and initial public offerings (IPO) of a wide range of financial instruments.

DIY Investor brings you the latest issues, launches and initial public offerings (IPO) of a wide range of financial instruments.