May

2021

The stars are aligned for UK equities

DIY Investor

9 May 2021

With recovery in prospect, could this be UK equities’ moment?

With recovery in prospect, could this be UK equities’ moment?

We believe a rare set of events have combined to make the UK equity market a highly attractive prospect right now – and Claverhouse Investment Trust could provide an attractive vehicle to capitalise on it.

The income outcome

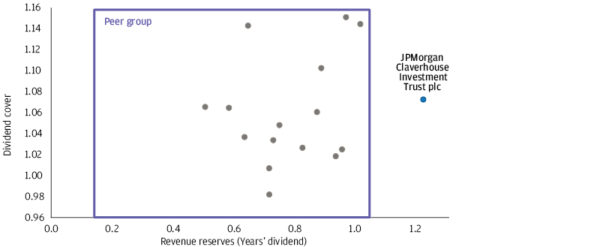

Investors around the world have grown accustomed to dark times. The effects of the pandemic continue to crush income hopes. In the UK, dividend values fell by 44% in the course of 2020, hitting their lowest level since 2011.1 Against this backdrop, rare chinks of good news shine even more brightly – notably the announcement in January by JP Morgan’s Claverhouse Investment Trust that it was increasing its dividend by 1.7%.

This remarkable achievement speaks to the in-built advantage of investment trusts. Unlike ‘open-ended’ funds, they can draw on a fixed pool of capital that allows them to plan for the long term, since they can retain 15% of their income. And Claverhouse’s enjoys especially strong reserves. In fact, the trust has now increased its dividend 48 years in a row. That’s among the longest record of unbroken rises of any UK equity-focused trust.

Exhibit A – UK Equity Income Investment Companies

The case for UK equities

Claverhouse managers firmly believe that having a UK focus will give investors a positive advantage in the market of early 2021. With Covid-19 vaccine programmes rolling out, recovery is tangible. The investment skies are clearing. Given the heavy fiscal support delivered by governments to bridge the pandemic, interest rates are likely to be suppressed for some time. But the US election and the long-awaited resolution of Brexit have bolstered political stability on either side of the Atlantic.

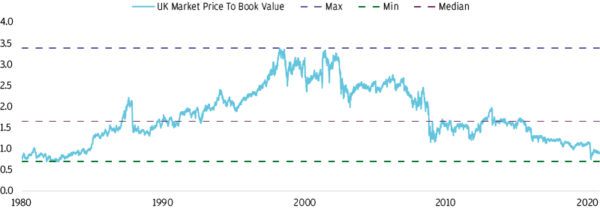

“At this pivotal point of the pandemic, UK stocks offer a tantalising prospect”, says Will Meadon, Claverhouse portfolio director. UK equity prices are currently trailing well below recent performance: a glance at the records shows them hovering near the lows of the 1980s. “They are not only historically cheap, but attractively valued compared to overseas markets – notably the US, which is dominated by sky-high tech valuations,” Meadon says.

Exhibit B – UK equities cheap vs. own history and cheap vs. other international equity markets

UK Market price to Book (x)

Past performance is not a reliable indicator of current and future results.

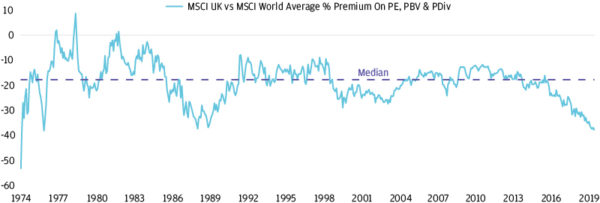

The >30% discount for MSCI UK vs. MSCI World is at over 40 year low

Past performance is not a reliable indicator of current and future results.

Under-performance in recent years has led many investors to avoid UK stocks. Yet the coming recovery might be their chance to shine. In particular, it could lift the currently unfashionable ‘value’ stocks – long-established sectors that appear to be undervalued compared to their performance and potential – such as construction, oil and gas and financial services. Claverhouse is well placed to capitalise on such a development: its portfolio includes a range of both blue-chip and mid-cap value stocks.

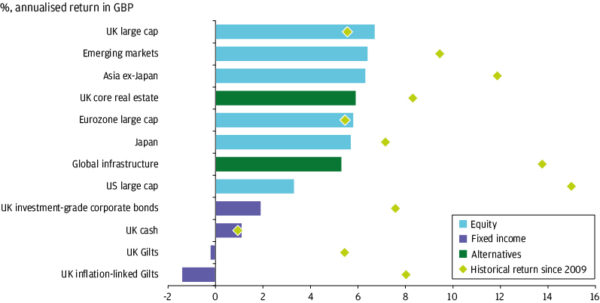

2021 Long-Term Capital Market Assumptions expected returns in coming 10-15 years

Past performance is not a reliable indicator of current and future results.

Buy UK, buy global

Investing in UK equities doesn’t mean turning your back on the rest of the world; quite the reverse. AstraZeneca’s UK-Swedish base and its international vaccine rollout is currently the most prominent example of the worldwide footprint of nominally UK companies. Like BP, Unilever or GlaxoSmithKline, it’s a global firm that happens to be UK-listed.

“In fact, 70% of the revenues of the UK’s top 100 stocks originate from overseas,” Meadon points out. “The UK economy is not the UK stock market, and the UK stock market is not the UK economy.

“So investing in UK equities is a way of buying into some of the best global companies without having to pay the inflated valuations you see in other equity markets. By opting for an investment trust, investors can exploit this anomaly in a diversified way, while benefiting from increased income.”

The case for investing now

Given the twists of the past year, the course of the recovery remains uncertain. We believe this underlines the case for investing in a structure such as Claverhouse, where future income is supported by a strong revenue reserve base. But a market that’s historically and globally cheap, and simultaneously well placed for recovery, is a singular event.

Even Meadon, who has spent much of his 38-year industry experience at JP Morgan, has rarely witnessed such an auspicious moment for UK equities. “This is a very unusual confluence of events: those stars don’t align very often,” he declares.

Like any heavenly collision, however, the opportunity to get involved is brief – and narrowing. “Investors globally are, for the first time in 10 years at least, starting to show interest in value stocks,” Meadon warns. In our view, that means there’s a limited time for informed investors to jump on board the UK equities craft before it takes off.

Find out more about JP Morgan Claverhouse Investment Trust >

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of The warning in brackets must be removed if the Marketing Communication has been released for General Public.

financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Annual Reports and Financial Statements, AIFMD art. 23 Investor Disclosure Document and PRIIPs Key Information Document can be obtained free of charge from JPMorgan Funds Limited or www.jpmam.co.uk/investmenttrust. This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

Commentary » Equities » Equities Commentary » investment trust commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.