May

2022

ShareScope: Helping private investors for 25 years

DIY Investor

15 May 2022

At ShareScope we are interested in education in a broad sense – both helping new investors and traders get a clear idea of how markets work (from the definition and understanding of the PE ratio to the fact that spreads are wider earlier in the day) but also developing more complex tools for experienced investors – writes Martin Stamp, CEO and Founder, Sharescope.

At ShareScope we are interested in education in a broad sense – both helping new investors and traders get a clear idea of how markets work (from the definition and understanding of the PE ratio to the fact that spreads are wider earlier in the day) but also developing more complex tools for experienced investors – writes Martin Stamp, CEO and Founder, Sharescope.

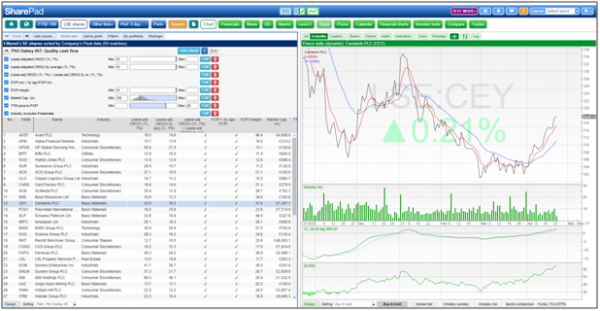

ShareScope is the UK’s most popular software for helping private investors and traders make well-informed investment decisions. ShareScope was written for Windows 95 in 1997; we created a web version – SharePad – in 2015. ShareScope has won many accolades including almost every Investors Chronicle’s award for best investment software since 2002.

(SharePad’s web application works across all devices)

A blast from the past

I wrote ShareScope’s first release. My work background is programming – my most significant previous job was with Psion (early tech company which briefly got into the FTSE 100 during the TMT – technology, media, and telecom – bubble) which I joined as employee number ten.

I wrote ShareScope’s first release. My work background is programming – my most significant previous job was with Psion (early tech company which briefly got into the FTSE 100 during the TMT – technology, media, and telecom – bubble) which I joined as employee number ten.

But I’d always been interested in the stock market – my father was a stockbroker and I bought my first shares aged 10 – so when I looked for software to help me diversify my Psion holding I was so underwhelmed that I decided to write my own program.

When ShareScope launched many people asked: why isn’t it web based? The World Wide Web (as we used to call it) was red hot, Yahoo dominated search, Google was just getting going, the standard way of connecting to the internet was dial-up 56Kbs modems and screens were 1/10th the size of today’s monitors.

The internet stock bubble was just getting going and had 4 years to run before painfully collapsing. The challenge to developing a world class financial information program (which is what I was aiming to do) was that the web was very primitive compared to what it is now.

To achieve the rich functionality, the flexible display options and the responsiveness would have been impossible on the web.

To achieve the rich functionality, the flexible display options and the responsiveness would have been impossible on the web.

With ShareScope almost every mouse click or key press appeared on the screen in less than 1/10th of a second – literally as fast as the blink of an eye. You could change the selected share to Marks & Spencer as fast as you could type ‘M’, ‘K’ and press Enter.

I wanted ShareScope to be something that investors and traders would be happy to pay for, that didn’t fill most of the screen with blinking ads and, I think this is very important, respected their time. The only way to meet this requirement was a well written program running on Windows.

It is noteworthy that the financial data we were distributing had only been made available to private investors a couple of years earlier. Before the 90’s investors relied on national newspapers, the Investors Chronicle and their stockbrokers – going back to when my father was a broker when there was a fixed 1.5% commission on all share purchases and sales.

An important difference between ShareScope and the competition – and there were competitors – was that we were both strong on fundamental data and tools but also strong on technical analysis. According to our surveys around 70% of our users were very interested in fundamental data and 70% were very interested in technical analysis. Clearly many were very interested in both.

How ShareScope developed

ShareScope today is a much richer experience than when we started. Partly it’s because more data has become available and partly because computers and the internet are far more capable than in 1997. Just to give a flavour of how things have evolved since then:

- Several updates a day of fundamental data – initially it was weekly

- Fundamental data now includes full P&L and balance sheet – initially it was just 4 numbers: Turnover, Profit, EPS and dividend

- Streaming real time and delayed price data

- Financial news that could easily focus on a single company or a portfolio

- Data mining and filtering on all data

- European and US prices and fundamentals – these were hard to come by in 1997

- Alarms on numerous criteria, Directors’ Dealings, Geographical spread, Analyst forecasts and Level 2 (showing market orders)

The big changes in the financial marketplace

Fees have reduced substantially and cost transparency has increased. Many investors didn’t realise just how much they were paying in fees, both hidden and transparent. Today’s situation is far better but still far from perfect – there are 17 different charges that Unit trusts charge and a number of them, bizarrely, are not included in TER (Total expense ratio).

Each group of funds seems to have its own unique way of charging but they can include entry charge (typically 5%), redemption fee, switching fee, annual management fee, platform fees, trading costs, custodian fees, valuation fee, trustee fee and several other. In my view many of these charges should be included in the management fee as they are essential to managing the fund and allow for a cleaner comparison of the cost of different offerings.

High fees is one of the reason I started ShareScope – if you take active control of your investments you have much better control of your costs.

Another major change is the greater emphasis on ethical investing which goes by many different names such as ESG (Environment, Social & Governance), directed investing or impact investing.

When ShareScope started some companies argued it was their obligation to maximise profits and if that involved sanction busting, bribery, or forced labour so be it. Though a few companies might still follow such practises none would now admit to it – among other things companies now have legal obligation to root out bribery and any form of slavery or child labour.

I expect further changes in companies’ ethical stance especially in the areas of climate change and pay & promotion relating to gender, race, disability and similar. Of course there will be companies that only pay lip service (e.g. greenwashing) but the direction of travel is set and such companies will, over time, be called out.

Money gives power and even smaller investors, if they act together, can have a significant influence on which companies flourish. This trend will continue to become more important but I would caution investors not to invest solely on ethical criteria – most companies today aim, or at least claim, to want to improve the world in some way.

For example Theranos (who claimed to be able to analyse blood from a pin prick of blood) would have been very ethical – if only the technology was real. It is also quite hard to be certain that a big company really is ethical. One might expect Credit Suisse to avoid criminals, fraudsters & corrupt politicians. Apparently they aren’t.

Tracker funds have grown dramatically. It is obvious that the average active fund is not going to beat the market very often if at all – taken together they are too big a percent of that market and then there are those pesky fees. It is interesting to ask why the financial sector makes up 8.6% of the national GDP (don’t trust me – google it).

A great innovation is ETFs (Exchange Traded Funds) which did not exist in 1997. They offer a fine way of diversifying your investments at low cost. But again, investors have to pay attention: ETFs are not always low cost.

And I would recommend to never use leveraged products – where you get 2 or 3 times the gain but also 2 or 3 times the loss on a daily basis. The way they are calculated means that if the price were to cycle between 101 and 100 for 20 days an investment will be 0.2% lower (x 2 leveraged) or 0.6% (x 3 leverage). This is true regardless of whether the ETF is long or short.

During ShareScope’s early existence the City of London was thriving and became (arguably) the world biggest financial hub. Since then the City’s rank has slipped and Brexit may hasten its relative decline.

During ShareScope’s 25 years hedge funds have become high profile. A friend of mine sold an industrial business and seriously considered founding a hedge fund even though he knew nothing about investing – the 2% + 20% (2% of funds invested and 20% of the upside every year) model is so attractive – the only challenge is to attract investors.

There is constant debate as to how successful they really are – mainly relating to survivor bias i.e. forgetting ignoring failed funds. While Hedge funds can hedge (e.g. go long some stocks and short others) they are not obliged to and some hedge funds are alarmingly narrow in their focus and then add leverage (borrowed money) so that they can easily do spectacularly one year and tank, or close, the following year.

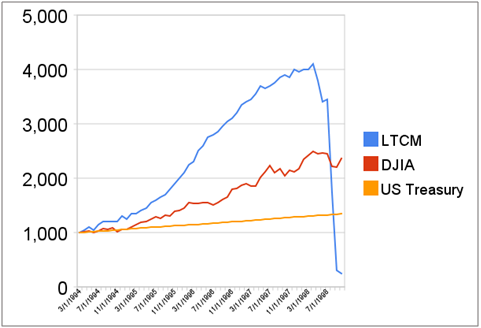

The archetypal example being Long Term Capital Management which had 2 Nobel prize winners on the board and a ton of clever, experienced executives. They went spectacularly bankrupt after just 4 years.

They even had the nerve to claim that what happened in the market was a 10 sigma event – a 10 sigma event would only happen once in the life of the universe but in their case it happened after 4 years. You decide. The fact was their risk model was just wrong.

(Long Term Capital Management (LTCM) performance 1994 – 1998. The value of $1,000 invested in LTCM, the Dow Jones Industrial Average and invested monthly in U.S. Treasuries at constant maturity. Source: Wikipedia)

A simple thought experiment shows off the 2% + 20% model’s weakness. A rich investor or institution sets up two hedge funds. They both follow the same high risk / high reward non-diversified strategy but in the opposite direction – if one buy’s an instrument (say oil) the other shorts it.

At the end of the first year one of the funds, let’s call it Fund 1, will (almost certainly) be in serious profit and the other one, Fund 2, in serious loss. For Fund 1 the managers get 2% of the bigger pot + 20 % of the upside; for the other fund it just gets 2% of the smaller pot. Providing both funds are able to attract funds this is an absolutely sure way to make money. Merge failing Fund 2 investors into successful Fund 1 and start Fund 3 quoting the great success of Fund 1. Repeat…

Of course, no fund would be this blatant, but it is a very tempting model isn’t it?

And the last major innovation: Crypto currencies.

Some of today’s crypto currencies will be around in ten years but the vast majority will be gone – it is said that there are currently over 40,000 crypto currencies. Block-chain technology is a hugely inefficient way to run huge databases.

For example, someone buys a coffee in El Salvador with Bitcoin and the information on the transaction is transmitted to tens of thousand computers around the world. This is madness. And the ‘mining’ of Bitcoin is very ecologically damaging. When will there be a major shakeout of cryptos? I would say anyone that claims to know is a fool or a liar.

The future

We have lots of ideas to continue keeping our existing subscribers happy and attracting new investors and traders. For example, getting a clearer idea of how risky a share or a portfolio is or to get a better idea of how ethical each company is.

![]()

Commentary » Equities » Equities Commentary » Equities Latest » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.