Jan

2023

Investment Outlook 2023

DIY Investor

8 January 2023

In brief: A bad year for the economy, a better year for markets

- Despite remaining above central bank targets, inflation should start to moderate as the economy slows, the labour market weakens, supply chain pressures continue to ease and Europe manages to diversify its energy supply.

- Our core scenario sees developed economies falling into a mild recession in 2023.

- However, both stocks and bonds have pre-empted the macro troubles set to unfold in 2023 and look increasingly attractive, and we are more excited about bonds than we have been in over a decade.

- The broad-based sell-off in equity markets has left some stocks with strong earnings potential trading at very low valuations; we think there are opportunities in climate-related stocks and the emerging markets.

- We have higher conviction in cheaper stocks which have already priced in a lot of bad news and are offering dependable dividends.

Developed world growth to slow with housing activity bearing the brunt

As we look to 2023 the most important question is actually quite straightforward: will inflation start to behave as economic activity slows? If so, central banks will stop raising rates, and recessions, where they occur, will likely be modest. If inflation does not start to slow, we are looking at an uglier scenario.

Fortunately, we believe there are already convincing signs that inflationary pressures are moderating and will continue to do so in 2023.

Housing markets are, as usual, the first to react to central banks touching the monetary brake. Materially higher new mortgage rates are crimping new housing demand and we think the ripples of weaker housing activity will permeate through the global economy in 2023. Construction will weaken, spending on furniture and other household durables will fall and falling house prices could weigh on consumer spending for the next few quarters. The decline in activity should have the intended effect of taming inflation.

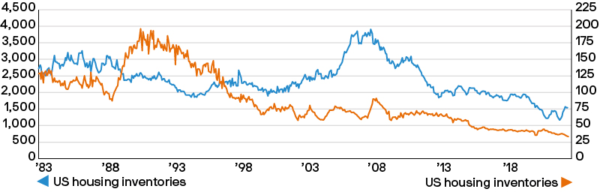

Thankfully, the risks of a deep, housing-led recession of the type experienced in 2008 are low. First, housing construction was relatively subdued for much of the last decade, which means we are unlikely to see a glut of oversupply driving house prices materially lower (Exhibit 1). Second, those that have recently bought at higher prices were still constrained by the banks’ more stringent loan-to-value and loan-to-income ratios.

Exhibit 1: Limited stock of housing for sale should prevent large house price declines

Housing inventories

Thousands (LHS); average stocks per surveyor (RHS)

Source: Haver Analytics, National Association of Realtors, Refinitiv Datastream, Royal Institute of Chartered Surveyors, US Census Bureau, J.P. Morgan Asset Management. US housing stocks include new and existing single-family homes for sale. Both series are seasonally adjusted. Data as of 31 October 2022.

Finally, the impact of higher rates on mortgage holders is likely to be less severe. In the US, households did a good job of locking in the low rates experienced a couple of years ago. Only about 5% of US mortgages are on adjustable rates today, compared with over 20% in 2007. In 2020 the 30-year mortgage rate in the US hit just 2.8%, prompting a flurry of refinancing activity. Unless those individuals seek to move, their disposable income won’t be impacted by the recent increase in interest rates.

In the UK, some households have similarly done a good job of protecting themselves from the near-term hike in rates. In 2005 – the start of the last significant tightening cycle – 70% of mortgages were variable rate. Today, variable rate mortgages account for only 14%. However, a further 25% of mortgages were fixed for only two years. This makes the UK more vulnerable than the US, albeit with a bit of a delay.

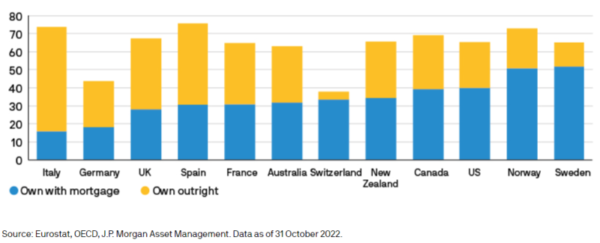

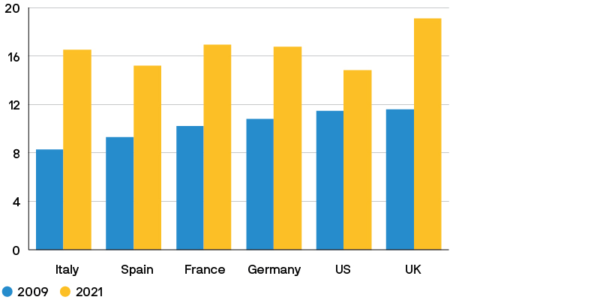

It’s also worth remembering that not everyone has a mortgage, while individuals that have cash savings will see their disposable income rise as interest rates increase. This factor is particularly important when thinking about the larger countries in continental Europe, where fewer households have a mortgage, and household savings as a percentage of GDP are higher than in the US and UK (Exhibit 2). The European Central Bank (ECB) was often warned that zero interest rates would be counterproductive because of the degree of savings in the region.

Exhibit 2: The main countries of Europe have less housing debt making them less vulnerable to higher ECB rates

Home ownership by mortgage status

% of households

Europe is weathering the energy crisis well

For Europe, the key risk is less about a housing bust and more about energy supply, given that Russia – the former supplier of 40% of Europe’s gas – stopped the bulk of its supplies this summer.

For the coming winter, at least, the risk to gas supplies is in fact diminishing due to a combination of good judgment and good luck. Europe managed to fill its gas tanks over the summer, largely replacing Russian gas with liquefied natural gas from the US.

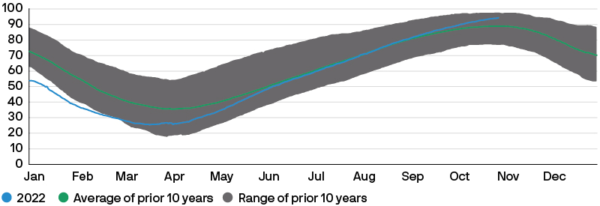

Since then, Europe has had the good fortune of a very mild autumn and, as a result, enters the three key winter months with storage tanks that are almost full (Exhibit 3). Unless temperatures turn and we face bitterly cold weather in the first months of 2023, Europe looks increasingly likely to make it through this winter without having to resort to energy rationing.

Exhibit 3: Europe enters the key winter months with full gas tanks

EU natural gas inventories

% capacity

Source: Bloomberg, Gas Infrastructure Europe, J.P. Morgan Asset Management. Data as of 31 October 2022.

The gas in storage was, of course, obtained at a very high price. However, governments are to a large extent shielding consumers from the bulk of higher energy prices. We will have to wait to the spring to see whether the cost to the public purse is proving too great for support to continue.

China to open up post Covid, easing global supply chain pressures

The Chinese economy has been faced with an entirely different set of challenges to the developed world with widespread lockdowns still in place to contain the spread of Covid-19. Low levels of vaccination, particularly among the elderly, coupled with a less comprehensive hospital network than in the west, have left the Chinese authorities reluctant to move towards a ‘living with Covid’ policy.

However, a prolonged period of lockdown also appears untenable and we expect China to experience an acceleration in activity as pent-up demand is released. While the timing of policy changes remains uncertain, the market’s performance has highlighted how sensitive investors are to any signs of a shift in approach.

Importantly, normalisation of the Chinese economy could significantly ease the supply chain disruptions that have contributed to rapidly rising goods inflation. Although a rebound in growth in China could also boost demand for global commodities, our assessment is that on balance this is another driver of lower inflation in 2023.

Inflation panic subsides, central banks pause

Signs of slowing activity in the west, and a return to full production in China, should ease inflation through the course of 2023, with the shrinking contributions from energy and goods sectors in particular helping price pressures to moderate in the months ahead.

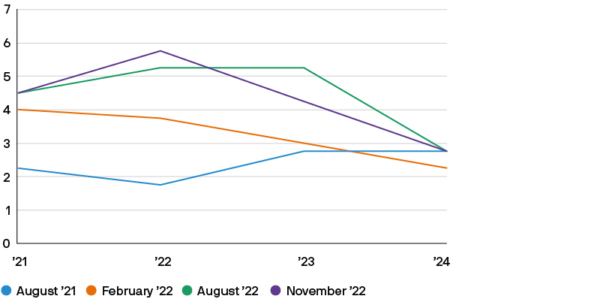

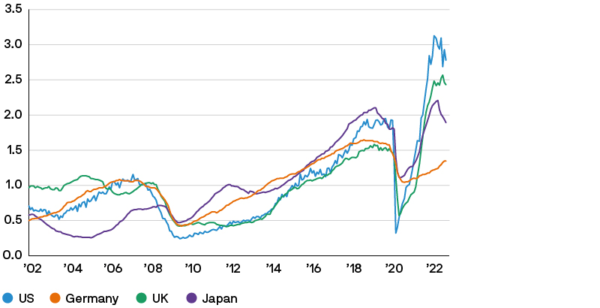

However, to be sure that we’re out of the inflationary woods, wage pressures also need to ease. This is where the central banks went wrong in assuming inflation would prove “transitory”, as they underestimated the extent to which labour market tightness would result in workers asking for more pay (Exhibit 4).

Exhibit 4: The central bank inflation errors are rooted in the labour markets

Bank of England average weekly earnings forecasts

% change year on year

Source: Bank of England, J.P. Morgan Asset Management. Forecasts are based on four-quarter growth in whole-economy total pay in Q4. Data as of 18 November 2022.

Job vacancies – which in all major regions still exceed the number of unemployed – will be a key indicator to watch in the next couple of months (Exhibit 5). Job hiring and quits are already rolling over and, given higher pay is one of the most common reasons for people moving jobs, we see this as a sign that wage growth should ease.

Exhibit 5: The labour market is still too hot

Job vacancies versus unemployment

x, vacancies as a multiple of unemployed, relative to average

Assuming headline inflation and wage inflation are easing, we see US interest rates rising to around 4.5%-5.0% in the first quarter of 2023 and stopping there. The ECB is similarly expected to pause at 2.5%-3.0% in the first quarter. The Bank of England may take slightly longer to reach a peak, given that inflation is likely to prove stickier in the UK. We see a peak UK interest rate of 4.0%-4.5% in the second quarter.

Central banks also have ambitions to reduce the size of their balance sheets by engaging in quantitative tightening, but we do not expect a particularly concerted effort, nor any significant disruption. Quantitative easing was designed to give central banks extra control and leverage over long-term interest rates, helping the market to absorb large scale government issuance. We expect quantitative tightening to operate under the same principle and, given bond supply is still expected to be meaningful in size in 2023 – and borrowing costs have already risen meaningfully – we expect central banks to be modest in their ambitions to reduce their balance sheets.

Recessions to be modest

Ultimately, our key judgment is that signs will emerge in the coming months that inflation is responding to weakening activity. Inflation may not be heading back quickly to 2%, but we suspect that the central banks will be happy to pause, so long as inflation is headed in the right direction.

Against this view, there are two types of bearish forecasters. Some still believe we have returned to a 1970s inflation problem, which will require a much deeper recession and much larger rise in unemployment than we expect to drive inflation away.

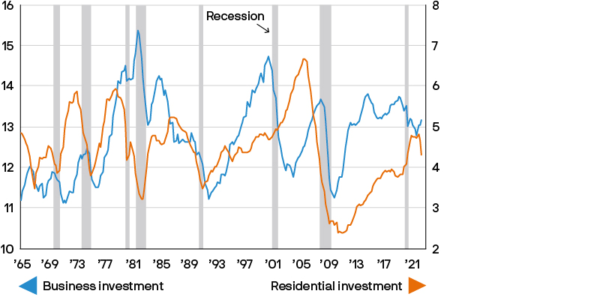

Others argue that moderate recessions are difficult to engineer because slowdowns take on a life of their own, with a tendency to spiral. This situation has been true in the past, when deep recessions were busts that followed a boom. Following excessive growth in one area of the economy – most commonly business investment or housing – it has often taken a long time for the economy to adjust and find alternative sources of growth. However, this time round, investment and housing growth has been more modest (Exhibit 6).

Exhibit 6: There wasn’t enough of a boom for us to worry about a bust

US residential and business investment

% of nominal GDP

In addition, bouts of excess enthusiasm have usually been fuelled by excessive bank lending, which has historically led to a period of weak credit growth, further compounding the downturn. This time round, however, more than a decade of regulation since the global financial crisis means that the commercial banks come into the current slowdown extremely well capitalised, and they have been thoroughly stress-tested to ensure they can absorb losses without triggering a credit crunch (Exhibit 7).

Exhibit 7: The health of the financial sector should prevent a credit crunch

Core tier 1 capital ratios

%, regulatory tier 1 capital to risk-weighted assets

In short, busts follow booms. But booms were notably absent in the last decade where activity across sectors was, if anything, too sluggish. Although economic activity does need to weaken to be sure inflation moderates, we do not expect a lengthy, or deep, period of contraction. Given the decline already seen in the price of both stocks and bonds, we believe that while 2023 will be a difficult year for economies, the worst of the market volatility is behind us and both stocks and bonds look increasingly attractive.

![]()

The Market Insights programme provides comprehensive data and commentary on global markets without reference to products. Designed as a tool to help clients understand the markets and support investment decision-making, the programme explores the implications of current economic data and changing market conditions. For the purposes of MiFID II, the JPM Market Insights and Portfolio Insights programmes are marketing communications and are not in scope for any MiFID II / MiFIR requirements specifically related to investment research. Furthermore, the J.P. Morgan Asset Management Market Insights and Portfolio Insights programmes, as non-independent research, have not been prepared in accordance with legal requirements designed to promote the independence of investment research, nor are they subject to any prohibition on dealing ahead of the dissemination of investment research.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not a reliable indicator of current and future results. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities: In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be.; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). For all other markets in APAC, to intended recipients only. For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance.

Brokers Commentary » Commentary » Investment trusts Commentary » Latest » Mutual funds Commentary » Take control of your finances commentary » Uncategorized

Leave a Reply

You must be logged in to post a comment.