Aug

2021

Global perspectives: Valuations in the ointment

DIY Investor

11 August 2021

During July, global consensus earnings estimates have re-accelerated to the upside, representing another bullish impulse in the tug of war between high valuations on the one hand and strong profits momentum on the other.

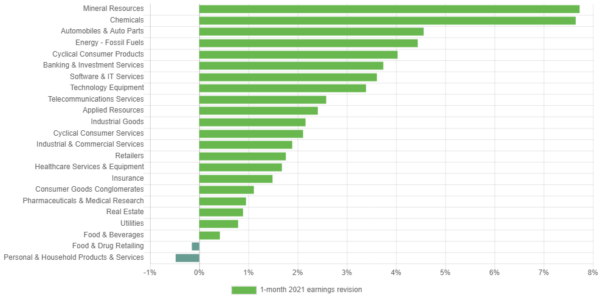

On a global basis, earnings forecasts have been especially strong in transportation, mining and chemical sectors. We maintain a neutral position on global equities, balancing valuation concerns against still strong earnings momentum but suggest heightened vigilance is in order for the autumn as the prospect of tighter monetary conditions draws closer. As developed market economies return to trend levels of activity, momentum is likely to slow just as central banks take their first steps on the path to policy normalisation.

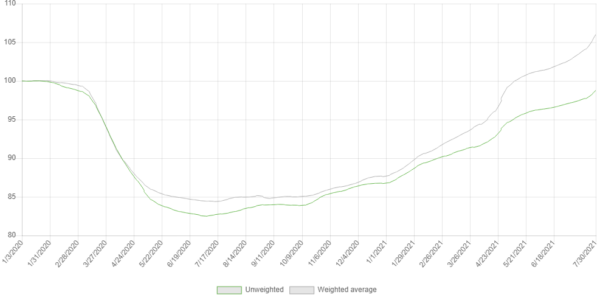

Exhibit 1: Global consensus earnings estimates re-accelerate to the upside

Click to visit:

![]()

Leave a Reply

You must be logged in to post a comment.