Aug

2021

Economic and Market Outlook: Cautious Optimism

DIY Investor

11 August 2021

We currently expect at least two more years of above trend economic and earnings growth as the recovery from the pandemic becomes more entrenched.

We currently expect at least two more years of above trend economic and earnings growth as the recovery from the pandemic becomes more entrenched.

That in turn should help underpin further gains in risk assets. But with assets well priced for our outlook, expectations for returns are lower than at the beginning of the recovery. And with a variety of alternative scenarios that could throw markets off course, we are keeping some portfolio risk budget available to take advantage of periods of heightened volatility.

At the time of our last Global Outlook, the consensus view in markets was that equity prices and government bond yields were set to keep grinding higher. Risk appetite would be buoyed by faster economic and earnings growth as vaccine deployment accelerated, economies re-opened more permanently and central banks and governments kept policy supportive.

And bond prices would come under further pressure as inflation rates picked up amidst the lax policy environment. Yet while equity markets did carry on their merry way, long-term bond yields dropped significantly in the major markets. And that was despite inflation readings surprising to the upside and central bank rhetoric being more hawkish than expected.

So, what happened? Well, the dynamics in equity markets are fairly easy to explain. Global financial conditions remain accommodative despite the marginal shift in the monetary policy mood music. Corporate profits have tended to surprise positively, with strong earnings news and expectations, amplified by the return of share buy-backs. This environment has also been conducive to the maintenance of low corporate bond spreads.

Corporate profits have tended to surprise positively, with strong earnings news and expectations, amplified by the return of share buy-backs.

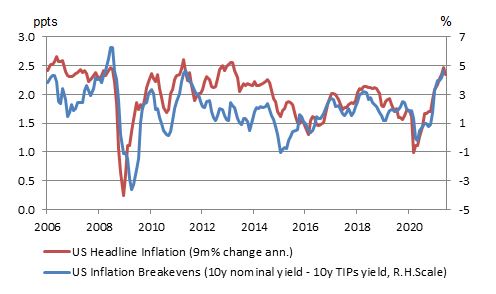

But the price action in government bond markets requires more careful parsing. Earlier in the year we noted that investor positioning and sentiment was very bearish. But historically, this has often been a contrarian buy signal. In a similar vein, while the airwaves have been filled with the news of core inflation reaching multi-decade highs in the US, market expectations for long-term inflation tend to rise and fall slightly in advance of official inflation readings.

Meanwhile, net bond supply is on a moderating trajectory and markets are pricing in a peak in growth momentum. These factors partly account for why the House View portfolio has been broadly neutral to slightly overweight global government bonds over recent months, though diversification against overweight positions in equities and credit also played a role in that allocation.

Plenty of room on the economic runway

Looking ahead, we expect the relatively favourable environment for risk assets to continue, albeit it with future returns likely more modest than seen over the past year. Our macroeconomic forecasts are a key underpin for this optimistic market outlook. We are forecasting at least two more years of above trend global growth. Despite the more transmissible and virulent Delta strain of the Covid virus taking hold in many countries, early evidence suggests that the variant has not escaped vaccines.

Thus while Covid remains a near-term headwind to the recovery in countries where vaccination has been slow, the more important signal is coming from the broad-based pick-up in vaccination rates. This should provide a durable path out of the pandemic, first in the advanced economies and then in the emerging world with a lag. That in turn is likely to facilitate a strong rotation from global goods demand to global services demand.

Policy settings are also set to remain accommodative, even if the peak in the policy impulse is now behind us. The US Federal Open Markets Committee (FOMC) did catch markets off-guard at its June meeting when the average member brought forward the date they thought that policy rates should rise. But the main decision makers within the Committee remain committed to waiting to see the whites in the eyes of inflation before substantively tightening policy.

Elsewhere, Chinese financial conditions are neutralising. But this reflects the advanced state of the recovery rather than a desire to dramatically slow economic or credit growth. And in economies ranging from the Eurozone, to Japan and Australia, inflation is simply too far from target to even contemplate formal policy tightening.

Those emerging economies, like Brazil and Mexico, where central banks have been forced to respond to higher near-term inflation are the exception to this broadly relaxed policy outlook. However, even here we think that these responses will not halt recoveries and to the extent that they stabilise inflation expectations, they are a positive signal for emerging market debt returns.

While our baseline forecasts anchor our House View, we also make use of alternative scenarios to balance our allocation. This is an acknowledgement of the considerable uncertainties affecting the outlook and our desire not to have a portfolio that is pointed at just one potential state of the world.

Other than a vaccine escape scenario, which would be the most destructive to risk assets, we are most concerned about scenarios that generate more persistent inflation pressures that our forecasts allow for.

There are good reasons why some of the recent attention grabbing price increases – such as for used cars — are likely to prove transitory; demand should moderate just as new supply is coming online. Indeed, we have already seen lumber prices fall from their peaks. But we cannot rule out bottlenecks broadening from goods to services.

And though we expect labour supply constraints to ease as re-opening gathers pace and government support policies are dismantled, gauging supply capacity in the economy and labour market is very difficult.

It is therefore plausible that inflation pressures prove more persistent, forcing central banks to bring forward more meaningful policy tightening, or in what would ultimately be the worst long-term outcome, shy away from that tightening just when it is needed.

Given the importance of inflation to the outlook we are closely monitoring wage outcomes, firms’ pricing power and different measures of inflation expectations for signs that our benign inflation forecasts need to change.

Relationship between long-term inflation breakevens and headline inflation in the US

Source: BLS, FRB, Haver, Aberdeen Standard Investments, as of July 2021

Maintaining a moderate pro-risk stance

Given this macro backdrop, our House View portfolio continues to be overweight risk assets. We do note that the recent strong performance from both risk and risk-free assets implies that our positive outlook is fairly consensual and broadly reflected in the price of assets. Investors are (just) being paid to take equity risk.

However, within the market, plentiful economic and earnings growth, allied with some valuation support suggests a continued attraction of some of the more cyclical areas of the market – although the recent falls in the discount rate, allied with continued strong earnings, talks to care in tilting too far away from quality and growth.

Government bond markets have recovered their poise following their fiscal and inflation driven ‘wobbles’ at the end of the first quarter. This recovery leaves them once again offering little value, and in addition leaves them vulnerable any periods of heightened inflationary concerns. That said, the House View maintains a modest overweight to duration, largely for diversification.

The largest change to the House View portfolio has been in UK real estate. Value has become apparent in some of the less popular areas of the market such as retail, with clearing prices starting to emerge. In addition, high construction prices are likely to limit future supply across the market.

While stock selection remains important, we are forecasting returns that broadly match the long-run expectations of equity markets. Though there is uncertainty about what the post-pandemic property market might look like for sectors such as offices, retail and leisure, there are attractive opportunities, with good tenants and attractive leases.

The views and conclusions expressed in this communication are for general interest only and should not be taken as investment advice or as an invitation to purchase or sell any specific security.

Any data contained herein which is attributed to a third party (“Third Party Data”) is the property of (a) third party supplier(s) (the “Owner”) and is licensed for use by Standard Life Aberdeen**. Third Party Data may not be copied or distributed. Third Party Data is provided “as is” and is not warranted to be accurate, complete or timely.

To the extent permitted by applicable law, none of the Owner, Standard Life Aberdeen** or any other third party (including any third party involved in providing and/or compiling Third Party Data) shall have any liability for Third Party Data or for any use made of Third Party Data. Past performance is no guarantee of future results. Neither the Owner nor any other third party sponsors, endorses or promotes the fund or product to which Third Party Data relates.

**Standard Life Aberdeen means the relevant member of Standard Life Aberdeen group, being Standard Life Aberdeen plc together with its subsidiaries, subsidiary undertakings and associated companies (whether direct or indirect) from time to time.

Brokers Commentary » Brokers Latest » Commentary » Equities Commentary » Investment trusts Commentary » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.