Sep

2020

Global perspectives- Global growth stocks over-hyped in 2020?

DIY Investor

20 September 2020

![]()

Growth investing has been fabulously successful in recent years as the strong operating performance of Web 2.0 digital economy franchises combined with steady multiple expansion.

In consequence, since 2015 global “value” indices have underperformed “growth” indices by a historically large margin. This lead has only widened during 2020 as the digital economy benefits from the acceleration of trends towards digital living and working from home.

Furthermore, the perceived quasi-monopoly status of these growing technology franchises have become even more highly valued on a relative basis as long-term interest rates have been pushed lower by central bank policy. Nevertheless, there are some similarities with the Y2K era which are worthy of discussion.

In the US, large-cap growth indices have in the past decade outperformed similarly constructed value indices by over 150%, after the prior decade of underperformance.

It is not the principle of outperformance but the recent extent which raises questions for prospective returns for growth stocks. As the growth segment of the stock market is qualitatively riskier, a tendency for long-term outperformance by growth stocks at the price of higher volatility should be expected.

However the degree of recent outperformance is quite unusual, at least over the past 25 years. The previous speculative peak in growth stocks occurred in 1999 and gave rise to a 75% outperformance which was fully unwound over the following cycle up to 2008. The magnitude of growth stock outperformance of 40% just in 2020 is therefore not entirely dissimilar to that of the dot-com bubble.

The dot-com comparison is not perfect but certainly sufficiently close to justify discussion in our view, rather than the “it’s different this time” dismissal.

The dot-com bubble seen through the eyes of history now appears as an obvious speculative mania, but not every outperformer in the original dot-com boom was a speculative stock, nor were the investment ideas always wrong and it was not easy to trade without hindsight.

Technology and the internet did prove to be the defining technology of the 21st century. The integration of technology, telecom networks and media (TMT) proved to be the correct business model.

The high market value placed on search and eyeballs was hardly a mistake in hindsight. That the gains from the internet would end up concentrated in the hands of just a few global players barely a decade later, in what was originally thought to be a competitive arena with no barriers to entry, would however have been a surprise to many start-up investors.

In addition to start-ups, the original internet bubble also resulted in an ultimately transient but large surge in valuations of a wide variety of large-cap and profitable stocks deemed relevant to the new economy, spanning the TMT sectors.

An underlying corporate investment bubble in technology infrastructure generated supernormal but temporary profits and margins for a narrow range of hardware suppliers.

Yet the collapse of the hardware investment cycle in 2001 vaporised this supernormal profitability of many technology manufacturers in a matter of a few quarters, while revenues from the advent of social media and the rapid growth of e-commerce had to wait for several further rounds of broadband and mobile handset innovation.

The challenge for value investors remains that while it is relatively easy to spot periods of high (or low) valuations in hindsight, in real-time there are few indications that sentiment will stage a reversal.

The trigger may only be visible after the event. Nevertheless, we are increasingly concerned that on a global basis valuations of the fastest-growing large-cap stocks are becoming disconnected from the remainder of the stock market and the accidental benefit from the COVID-19 pandemic is unlikely to be repeated.

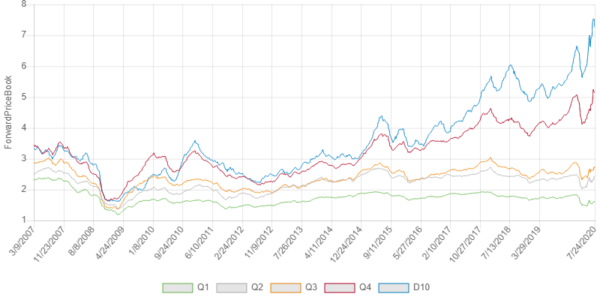

We have divided the largest 2000 global corporations into quartiles based on forecast revenue growth rates and plotted the prospective price/book multiple in Exhibit 1.

Exhibit 1: Price/book valuations of faster-growing global stocks have surged since 2015

Source: Refinitiv, Edison calculations. Chart shows median p/book multiple by growth quintile

While the median forward price/book multiples for slower-growing companies has remained close to the average for the period, the median forward price/book multiple for the fastest growing quintile is now over 2 standard deviations above its long-term average.

Furthermore, Exhibit 1 also shows the re-rating has been even sharper for the top decile of growth stocks (D10). In absolute terms, the median large-cap growth stock was valued at 3x book value in 2015 and is valued at 5x book value today.

It is a testament to the power of modern monetary and fiscal policies that this exuberance is being observed just ahead of the largest global recession since WWII.

Clearly, this situation has not arisen by chance and there have been good reasons for favouring growth stocks in the past. At the core of the growth stock phenomenon of recent years has been the new class of digital defensives – scale and high margin software and hardware businesses which have grown at multiples of GDP growth rates.

Execution has been strong and these businesses have determinedly invested to see off competitive threats. Digital trends have only accelerated as a result of COVID-19. The qualitative investment case has therefore remained compelling for many investors.

Nevertheless, balanced against these attractive qualitative elements of growth stock investing are the quantitative valuations now several standard deviations above average. These appear to indicate the merits of this segment of the stock market are now firmly embedded in current market pricing.

Click to visit:

![]()

Commentary » Equities » Equities Commentary » Equities Latest » Latest » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.