Nov

2017

Would you like that in a small, medium or large, Sir?

DIY Investor

1 November 2017

Three pretty compelling reasons why investing in smaller firms can be more lucrative than large – Neil Hermon, Henderson Smaller Companies Investment Trust

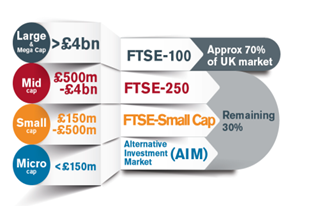

UK investors have tended to fill their portfolios with funds investing in the large, liquid firms of the FTSE 100. They are easy to buy in large amounts, well established in their sectors, have strong governance and long histories of creating shareholder value.

But history points to even stronger returns in the UK’s smaller companies; firms in the bottom 30% of the UK stock market by market capitalisation – the FTSE 250 and smaller, or less than around £4bn.

Source: Janus Henderson Investors

Their volatility likely contributes greatly to small-cap reluctance – share prices tend to swing more wildly, and they’ve been known to disappear from time-to-time on account of poor management.

But the long-term numbers – where investors should be focused – speak for themselves: if you’d put £100 in the FTSE all-share in 1955, by 2016 you would’ve received £96,792; for the FTSE-Small-Cap it would’ve been £597,433. The latter is quite remarkable at six times the former.

Why is small – mighty?

Professors’ Elroy Dimson and Paul Marsh of London Business School developed the theory behind why small-cap firms outperform larger ones.

1) Organic growth – The growth potential tends to be greater because it’s much easier for small, ambitious companies, with profits in the millions rather than billions of pounds, to double their business; a firm earning £1 million one year could feasibly double that the following year, but one that earned £1 billion would have to generate an additional billion pounds over that time to achieve the same growth rate.

Small companies also have more options for increasing business; they are more nimble, dynamic and innovative, are able to expand into new parts of the country or overseas, and can more easily, launch new products or services. In contrast, new initiatives for giant multinationals are likely to affect only one of many subsidiaries or product lines.

And it’s a self-fulfilling prophecy – a company that repeatedly delivers on its earnings increasingly satisfies investors who then place a higher value on the business. This is known a momentum.

2) Lack of research – The stock market is a pricing mechanism that takes into account all of the publicly available information there is regarding a firm’s finances and its operations, interpreted by analysts. Big companies tend to be followed by lots of analysts: it averages 24 per firm for those over £10bn. Because they are so extensively scrutinised it’s very unlikely any great corporate initiatives or managerial shake-ups will pass under the radar, so the share price tends to reflect the business realities fairly accurately, making it harder for fund managers to find pricing anomalies.

In contrast smaller firms have fewer analysts following them, with those under £500m averaging only 2, so there’s more opportunity to spot mispricing. Academics call this the ‘neglected effect’.

3) Mergers & Acquisitions – A big attraction of investing in smaller companies is the likelihood of a corporate action, usually when a larger firm snaps them up. For large, slow-growing companies, taking over an attractive small firm is the easiest way to expand the business in a lucrative new direction.

M&A deals are usually viewed as good news for shareholders in the acquired company because as owners of the business they receive payment – either cash or shares, or both, in the acquiring company.

Many companies built up a war-chest of cash following the financial crisis, reluctant to commit to major investments in such an uncertain environment – but as confidence has recovered they’ve been spending. Dealogic says records were broken in 2015, with $4.7trn of deals with 2016 still high at $3.8trn.

A rich history

The Henderson Smaller Companies Investment Trust has not always been in the business of smaller companies. It was founded in 1887 as the Trustees Executors and Securities Insurance Corporation, aiming to beat UK government bonds. Its original Chairman branched out into accountancy services eventually forming Touche Ross, now part of Deloitte – one of the biggest accountancy firms in the world.

In 1992 it started investing in smaller companies and in 2000 only those from the UK; it is one of the oldest investment trusts there is: surviving, adapting and evolving.

In 2002, in the wake if the dotcom crash, I became the Trust’s fund manager; since then – 4 prime ministers; various polarising US presidents; oil prices bucking between $30 and $140 a barrel; Harry Potter and his famous scar; a Middle-Eastern melt-down; a searing global financial crisis; and the explosion of social media, smartphones and apps.

Throughout these market twists and turns we have delivered an average annual return of 17.9%, outperforming the benchmark in 13 of the last 14 years. The past doesn’t predict the future, but this would have transformed £1,000 of your cash into over £12,000.

We’ve done it through consistency, consistency….you get the idea – the method has never changed.

Now supported by Indriatti van Hien, our focus is on finding exceptional management teams and good quality businesses, buying them at prices we think are value for money (other small-cap managers care less about firms priced expensively against history or otherwise, but we think this is a key mistake). With Brexit-this and interest rate-that, the UK market seems on a more cautious footing: probably now has never been a better time for stock picking.

Fund Manager Neil Hermon introduces The Henderson Smaller Companies Investment Trust (HSL), explaining the Trust’s objective and how the team works towards achieving this.

The information should not be construed as investment advice. Before entering into an investment agreement please consult a professional investment adviser.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which Henderson Global Investors Limited (reg. no. 906355), Henderson Fund Management Limited (reg. no. 2607112), Henderson Investment Funds Limited (reg. no. 2678531), Henderson Investment Management Limited (reg. no. 1795354), AlphaGen Capital Limited (reg. no. 962757), Henderson Equity Partners Limited (reg. no.2606646), Gartmore Investment Limited (reg. no. 1508030), (each incorporated and registered in England and Wales with registered office at 201 Bishopsgate, London EC2M 3AE) are authorised and regulated by the Financial Conduct Authority to provide investment products and services.

Leave a Reply

You must be logged in to post a comment.