Apr

2023

Will China smile again? Reasons to be hopeful in 2023

DIY Investor

1 April 2023

China is once again open for business! The managers of abrdn China Investment Company here discuss four reasons investors have to be optimistic – by Elizabeth Kwik and Nicholas Yeo

China is once again open for business! The accelerated reopening timeline was a welcome development ahead of the recent Chinese New Year holidays. Millions of people were able to reunite with their families following a lengthy period of strict Covid curbs and travel restrictions in the country.

However, there are some near-term risks to this positive development that we will need to monitor. The unrestricted movement of people throughout China could result in higher numbers of infection cases in the rural areas, where healthcare infrastructure is less developed compared to the Tier 1 cities where cases are already high.

That said, authorities appear to be preparing for any potential surge in Covid cases throughout rural China in the coming weeks. On a positive note, hybrid immunity in China’s population is happening at a faster-than-expected pace. Together with the accelerated reopening timeline, it is possible that economic growth can rebound faster than initially expected.

An event to watch out for would be the Two Sessions in March, where China’s main pair of political bodies, the National People’s Congress and the National Committee of the Chinese People’s Political Consultative Conference, are due to meet and the 2023 GDP target will be set.

Performance has been promising so far

The MSCI China A Onshore index is already up 23% from October lows – midcap stocks are on a roll (+40%), with the consumer discretionary sector up 60%, consumer staples up 44% and financials up 50%.

Though reopening has been on the agenda since last November when China first announced its plans, we think this rally has a longer, more sustainable runaway ahead for several reasons:

1) Chinese consumer stocks have been unloved by the market and are trading at historical discounts;

2) Households have excess savings that can fuel demand recovery across sectors as confidence in the economy is gradually restored; and

3) the fiscal and monetary environment remains supportive contrary to the rest of the world.

Over the hump of infections?

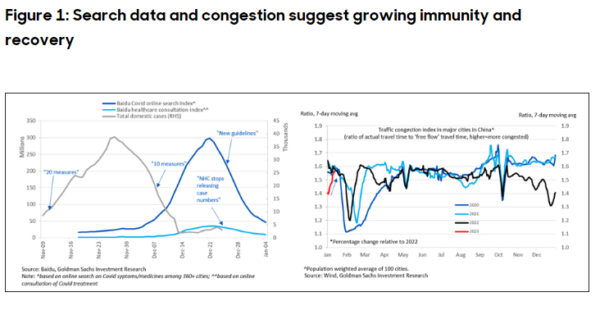

The eye-watering rise in the number of Covid infection cases in a population with low herd immunity is not all doom and gloom when it comes to sentiment on the ground. Even as the virus runs freely through China, with nearly 60,000 people with Covid having died in hospitals since the abrupt U-turn on zero-Covid last month, a majority of the 1.4 billion population appear to be unafraid of infection/re-infection.

Wanting to get out and about, they have flocked to major airports, train stations and highways ahead of the recent Lunar New Year holidays (Figure 1, right chart). This bodes extremely well for travel and tourism sectors where the likes of China Tourism Group Duty Free and China’s major airports will benefit.

The best is yet to come?…

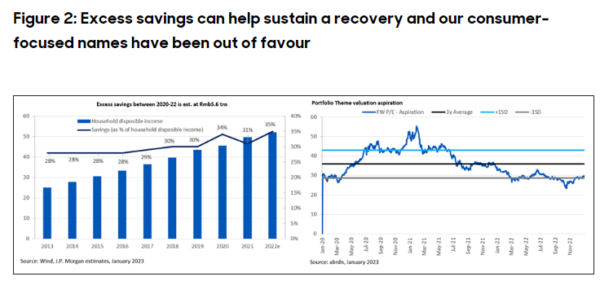

The reopening is just the initial spike and we think the market is under-appreciating the overall impact of rolling back Covid curbs on the economy. We expect a multi-stage recovery in China where domestic consumption normalisation has a long runway ahead, supported by excess savings (Figure 2, left chart) among households and depressed valuations (Figure 2, right chart).

Since the pandemic started in 2020, Chinese households have turned more cautious due to the heavy economic toll seen over the past few years. They have accumulated a significant amount of excess savings – the additional amount of disposable income saved vis-à-vis the pre-pandemic trend. In the near term, some of that excess savings, particularly in households that have had a steady stream of income through the pandemic, will contribute towards pent-up demand.

We are likely to see a spike in spending on discretionary, big-ticket items such as autos, luxury goods and tourism that households have put off due to zero-Covid-related uncertainties in recent years. Over this year, we expect the jobs market and income prospects to get better, supported by accommodative fiscal and monetary policies, which in turn will lead to a normalisation of the domestic consumption trend and drive growth recovery.

It will also benefit a number of other sectors that we discuss below. It is worth noting that the market currently remains focused on direct reopening plays and therefore other opportunities may get overlooked, which is where our bottom-up fundamental research driven stock picking can be a major advantage.

Recovery in confidence

As the reopening benefits fully materialise, and as jobs and income prospects improve in China, we expect positive impact on a number of other crucial sectors of the economy:

Tourism and travel

Property – The rollback of zero-Covid removes one of the major Covid-related headwinds facing the property sector. As one of the largest sectors of the Chinese economy and a major consumption driver, stabilisation and broad based recovery in the housing market is crucial for economic growth to bounce back. We expect this to happen in stages and, encouragingly, last year we saw a plethora of policy support for the developers. This year, we are likely to see more demand side support, which will be a positive in our view.

Healthcare – As Covid infections peak gradually across China, the sector will likely see rising demand for healthcare services that may have previously been postponed by patients (e.g. non-life threatening surgeries) in light of the surge in infection cases.

Banks – Better income prospects and improvement in the property sector could restore consumer confidence. That can potentially have a positive impact on credit demand and improve interest margins for lenders.

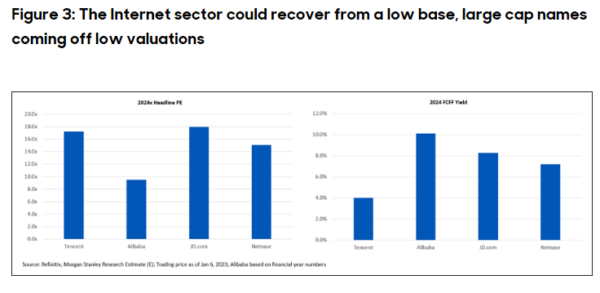

Internet names to benefit

We expect China internet – where valuations are still not stretched – to see three-pronged benefits of

1) reopening;

2) easing regulation; and

3) a newly developed focus on shareholder returns.

The reopening will spur direct segments like online travel and local services as well as indirect ones like e-commerce and eventually advertising. Regulatory headwinds eased last year. In a major de-escalation of the American Depositary Receipts (ADR) delisting threat, US auditors declared that they have gained sufficient access to audit documents of Chinese firms listed on American exchanges.

Chinese regulators have also indicated that their regulatory crackdown on internet companies is likely coming to an end. Further, companies have shifted their focus towards better shareholder returns through improved profitability, cashflow generation and share buybacks – last year, Alibaba announced a share buyback programme of $25 billion over a two-year period.

As much of the consumption in China is now done online, these companies have become highly correlated with consumer spending at the macro level. As the latter improves, revenue for internet companies are expected to also get better.

We hold various Chinese internet names in the abrdn China Investment Company portfolio, including Tencent, Alibaba, NetEase and JD.com.

Companies selected for illustrative purposes only to demonstrate the investment management style described herein, and not as an investment recommendation or indication of performance.

![]()

Important information

Risk factors you should consider prior to investing:

-

The value of investments, and the income from them, can go down as well as up and investors may get back less than the amount invested.

-

Past performance is not a guide to future results.

-

Investment in the Company may not be appropriate for investors who plan to withdraw their money within 5 years.

-

The Company may borrow to finance further investment (gearing). The use of gearing is likely to lead to volatility in the Net Asset Value (NAV) meaning that any movement in the value of the company’s assets will result in a magnified movement in the NAV.

-

Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. This may mean your money is at greater risk.

-

The Company invests in emerging markets which tend to be more volatile than mature markets and the value of your investment could move sharply up or down.

-

As with all stock exchange investments the value of the Company’s shares purchased will immediately fall by the difference between the buying and selling prices, the bid-offer spread. If trading volumes fall, the bid-offer spread can widen.

-

There is no guarantee that the market price of the Company’s shares will fully reflect their underlying Net Asset Value.

-

Yields are estimated figures and may fluctuate, there are no guarantees that future dividends will match or exceed historic dividends and certain investors may be subject to further tax on dividends.

-

The Company may accumulate investment positions which represent more than normal trading volumes which may make it difficult to realise investments and may lead to volatility in the market price of the Company’s shares.

-

Movements in exchange rates will impact on both the level of income received and the capital value of your investment.

-

The Company invests into other funds which themselves invest in assets such as bonds, company shares, cash and currencies. The objectives and risk profiles of these underlying funds may not be fully in line with those of this Company

Other important information

Issued by abrdn Fund Managers Limited, registered in England and Wales (740118) at 280 Bishopsgate, London EC2M 4AG. abrdn Investments Limited, registered in Scotland (No. 108419), 10 Queen’s Terrace, Aberdeen AB10 1XL. Both companies are authorised and regulated by the Financial Conduct Authority in the UK.

Find out more at www.abrdnchina.co.uk or by registering for updates. You can also follow us on social media: Twitter and LinkedIn.

Brokers Commentary » Commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.