Jul

2022

Why now could be the time to buy UK equities

DIY Investor

10 July 2022

Alex Wright, portfolio manager of Fidelity Special Situations & Special Values PLC, shares his latest outlook for UK equities. As investor sentiment shows signs of turning overly pessimistic, he outlines why, as a contrarian investor with a value focus, he is growing increasingly optimistic about certain areas of the domestic market.

Key points

- The deteriorating economic backdrop at home and abroad has led us to reduce our exposure to Gross Domestic Product (GDP) sensitive areas of the UK market, while adding to more defensive businesses.

- We believe investors sentiment is now showing signs of becoming excessively downbeat, with mid/small caps and some cyclicals derating significantly. This could present attractive opportunities.

- We are optimistic about the prospects of the companies we own. In aggregate, our portfolio holdings are trading at a significant discount to the broader market, with lower levels of debt and underappreciated growth potential.

We have seen very volatile markets so far in 2022, reflecting concerns over inflationary pressures and interest rate rises. The conflict in Ukraine as well as severe Covid-related lockdowns in China have intensified inflationary headwinds and added significant uncertainty to the outlook at both the macro and micro level.

Time for value?

The recent sell-off in some parts of the UK market has been sharp and indiscriminate. While the near-term economic outlook looks challenging as central banks seek to tackle inflation and recession risk, a downturn is already priced in. We believe sentiment has recently become overly pessimistic. Cyclicals and mid/small-caps, for example, have significantly derated reflecting excessively negative outlooks, which is starting to present us with attractive opportunities given our contrarian value approach.

It is also important to recognise that UK equities remain undervalued compared to global markets and reasonably valued in absolute terms. And while the outlook for returns across all asset classes looks more challenging, the UK market remains relatively well placed, mainly due to its sector exposure and the low valuation starting point. In comparison to other developed markets and the US in particular, the UK market is still cheap – for example, it is currently trading around 10 times 2023 forward earnings versus the US which is on 16 times.

Over the past decade and a half since the global financial crisis, we have had a very unusual period where rates have been kept at such low levels, favouring growth stocks and acting as a headwind for value stocks. This near-zero interest rate environment is changing rapidly as rising inflation is forcing the hand of central banks. This should be a better environment for value investing and companies whose valuations reflect to a greater extent nearer-term potential earnings.

Portfolio positioning

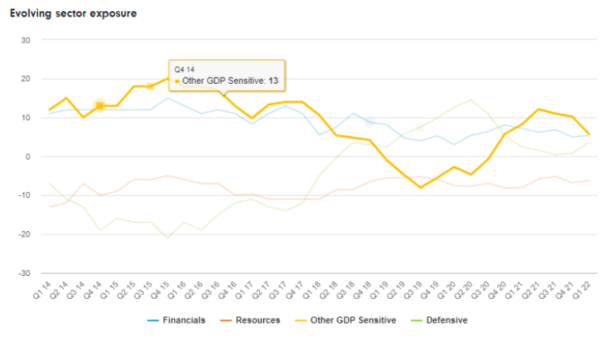

An undeniably more challenging environment for the consumer has led us to reduce our overweight exposure to GDP sensitive areas over the past six months, especially stocks that had performed well but looked more vulnerable. For example, we have trimmed our exposure in Inchcape and Tyman and sold out of Frasers, Currys and WPP.

Source: Fidelity International, 31 March 2022. Macro weightings chart for illustration purposes only. Sector/stock categorisation is at Fidelity’s discretion. Representative portfolio FIF Special Situations shown on chart. Special Values PLC’s relative exposure on 31 March 2022: Defensive +4.4%; Financials +7.2%; GDP Sensitive +6.9% and Resources -6.3%.

Within financials, we have taken some profits out of life insurers (although they still remain a large overweight position) and recycled this into banks, which are now an overweight position in the portfolio. Barclays, for example, is trading at crisis-like levels despite delivering a solid return on tangible equity. Banks will not only benefit from rising interest rates, but also from expanding loan books at a time when most consumers and large corporates have ample ability to borrow and may need to do so to meet rising costs.

We also took advantage of the market volatility in late February to add to defensive holdings that had sold off heavily, despite these stocks having little or no exposure to the war in Ukraine – Serco and Imperial being the biggest purchases here- as well as adding to some high conviction stocks such as Ryanair and consumer finance firm Kaspi.

Benefitting from takeover activity

Our focus on undervalued companies with sound or improving fundamentals has meant that many of our portfolio holdings have been the subject of M&A bids. Indeed, in aggregate our portfolio holdings are trading at a significant discount to the broader UK market, without having to sacrifice quality, profitability or return on capital. Given this, it is of little surprise that 10 of our holdings have been the subject of bids over the past 18 months, with power generation company ContourGlobal the latest to receive an all-cash offer from private equity group KKR.

Significantly, a sizeable percentage of our holdings are either actively engaged in buying-back their own stock or considering buybacks over the next 12 months. This highlights their robust balance sheet position following last year’s big earnings recovery and attractive valuations. From our perspective, these buybacks boost returns on invested capital and earnings per share.

Overall, we continue to see strong potential for upside given the higher quality profile of companies in the portfolio, which carry low levels of debts, and are thus relatively well placed to navigate an uncertain near-term environment.

Important information

The value of investments can go down as well as up so you may get back less than you invest. Investments in emerging markets can be more volatile than other more developed markets. Changes in currency exchange rates may affect the value of investments in overseas markets. Fidelity Asian Values PLC can use financial derivative instruments for investment purposes, which may expose them to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The shares in the investment trust are listed on the London Stock Exchange and their price is affected by supply and demand. The investment trust can gain additional exposure to the market, known as gearing, potentially increasing volatility. Investments in smaller companies can carry a higher risk because their share prices may be more volatile than those of larger companies. Reference to specific securities should not be construed as a recommendation to buy or sell these securities and is included for the purposes of illustration only. Investors should note that the views expressed may no longer be current and may have already been acted upon. This information is not a personal recommendation for any particular investment. If you are unsure about the suitability of an investment you should speak to an authorised financial adviser.

Brokers Commentary » Commentary » Investment trusts Commentary » Investment trusts Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.