Feb

2021

What happens when the party starts back up?

DIY Investor

23 February 2021

There are many signs of pent-up demand in the UK economy which should give investors cause for encouragement – writes Jean Roche

There are many signs of pent-up demand in the UK economy which should give investors cause for encouragement – writes Jean Roche

As the nights have drawn in over the past few weeks I’ve found myself thinking back to a beautifully dressed but redundant wedding reception room that I saw in a hotel over the summer.

I now picture the thousands of unused party venues around the country, and all the enormous expenditure that will come when they are filled with people once more. Such scenes, for me, symbolise the pent-up demand in the economy and fill me with encouragement.

So, while the recent pick-up in Covid-19 infections is very concerning for us all, from an investment perspective there remains cause for optimism. From all the data we trawl, analysis we read and conversations we have its clear there remain plenty of sources of pent-up demand in the UK economy waiting to be realised.

Missed by official statistics

The sudden onset of the pandemic has left us mourning the loss of the carefree life we used to live, filled with holidays, cinemas, cafes, restaurants and pubs, weddings and house parties, where only six attendees would be an embarrassment. But not all is lost.

What’s more, events on the ground can sometimes be missed by the official statistics, overlooked by our newspapers, TV stations and social feeds. Keeping your eyes open to what’s happening right in front of you can be really useful.

I wasn’t at all surprised by the news the UK economy grew by 6.6% in July. After all, pay fell by just 1.6% in the second quarter of 2020 which was obscured by a narrow focus on a predictably poor GDP number (whose calculation methodology has some shortcomings).

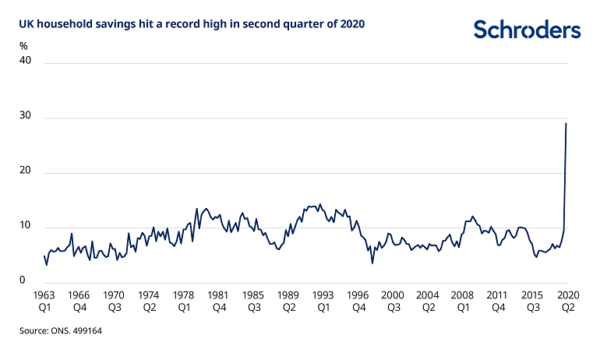

We all had a feeling that bank deposits must have surged as people could not spend their money as planned this year. The data have, obligingly, shown this to be the case, with UK household savings hitting a record high in the second quarter of 2020 (see below).

Meanwhile, job losses at some of the country’s largest employers have continued to dominate the headlines, while it has gone unnoticed that many small companies are creating new jobs. Don’t forget we’ve seen the acceleration of many trends in the UK’s flourishing digital economy during Covid-19 (see The “homebody economy” – investing in your digital back yard).

As seasoned investors we are well practiced in avoiding knee-jerk reactions – back in March when the devastating implications of the Covid-19 pandemic were becoming clear we kept faith in our homework.

We felt the crisis would not fundamentally change the investment outlook for many of the strongest companies. Although the outlook may be uncertain for the near term, a year or even 18 months of disrupted business should not significantly alter their “true” value.

This is because the companies in the best financial position, with strong balance sheets, are able to weather short-term disruption and focus on long-term performance.

In contrast, markets tend to overreact, to both good and bad news. This is precisely why knee-jerk reactions to headlines that encourage us to catastrophise about the future are never advisable.

Long march higher

If Covid-19 has accelerated trends in the digital economy, it has also brought some difficult decisions forward. Casual dining specialist The Restaurant Group (TRG) pointed out in its recent interim results that there has been around a 30% reduction in capacity in this market so far this year, including brands such as Bill’s, Pizza Express, Pizza Hut and its own Chiquito.

One could argue that given previous rapid capacity growth, events merely accelerated the inevitable for these brands.

In terms of TRG’s other brands, I was reassured when recently peeking through the glass of my local Wagamama to see hundreds of takeaway bags lined up on the tables (one of which was mine) – a small observation of a pivot to takeaways and click and collect.

Meanwhile, the implications of e-commerce adoption racing ahead by years should continue to help fuel demand for light commercial vans. One such van recently arrived outside my house plastered with a “ready for use” depot sign across the windscreen – this drove home how much demand from UK consumers has not gone away during this crisis, only changed in nature.

The global financial crisis (GFC) was as traumatic for many mid-cap companies as Covid-19 is today. At an individual level, just think how your day has changed. For many of us the daily commute has got a lot shorter and the money we used to spend on public transport, a coffee and croissant on the way into the office and a Pret or Leon for lunch has been redirected.

The worst-hit companies have had to adapt very quickly and that pain is not only felt by them but by all the companies that supply them. Rent appears to have become optional as tenants encourage landlords to share the pain.

What does this mean for property values and the financial institutions that lend to them? These events will play out over the months to come.

But it’s important to keep some investment perspective in what feels like an increasingly short-term world. While the recovery following the GFC felt painfully slow, many mid-caps that had genuine competitive advantages emerged stronger. In hindsight, 2007-09 now appears as a minor blip in the long march higher in their share prices.

Huge uncertainties remain for the economy as the Coronavirus Job Retention Scheme comes to an end and the chancellor’s “Winter Economy Plan” kicks in, for instance. However, we suspect the investment impact of Covid-19 to be transitory for many companies – another blip in their share price charts when we look back in five years’ time.

Strong get stronger

In the early stages of the pandemic, we spent much time analysing how much cash companies had and what their survival prospects were. Since lockdown has been eased, activity has recovered well, allowing many companies to consolidate their strong competitive positions.

In the short term a lot will hinge on Covid-19 and the management of a second phase of lockdowns as winter approaches and recent developments underline how fluid the situation remains.

With a cautiously optimistic eye on the UK economy, we’ve continued to work as always, seeking out the best mid-cap companies which are able to thrive. The UK consumer will not be restricted to a party of six forever.

Click to visit:

![]()

Important Information:

This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.

Commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.