Aug

2018

400,000 orphan clients ‘trapped’: Watchdog encourages shift to cheaper DIY investing platforms

DIY Investor

1 August 2018

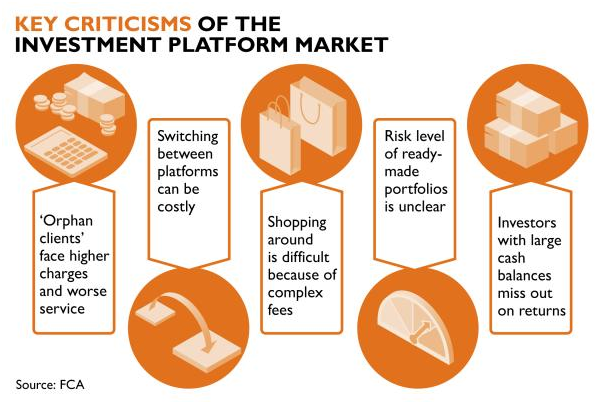

In a damning report, financial watchdog the Financial Conduct Authority (FCA) has said that anything up to 400,000 clients could be ‘trapped’, and in some cases paying thousands of pounds worth of fees, because they remain on an investment platform recommended to them by a financial adviser with whom they no longer have any contact.

These so called ‘orphan clients’ have either decided not to pay for advice, or been deemed unprofitable by their adviser; however, they remain on ‘advised platforms’ – which are generally more expensive less flexible than DIY platforms — even though they no longer receive advice.

FCA says that they could be paying up to 0.55% a year on an advised platform – more than double the amount if they were on a DIY investing platform.

‘paying up to 0.55% a year on an advised platform – more than double the amount if they were on a DIY investing platform’

FCA found that up to 10,000 orphan clients are charged additional fees of about £1.2m year for no longer having an adviser; although the regulator did not name the firms involved, according to the Times, 6,000 of the customers affected are with just three platforms: AJ Bell, Transact and Novia Financial.

- £2bn – Value of funds that ‘orphans’ have under management

- 7,500 – Number of Standard Life ‘orphans’, with average portfolio of £30,000

This issue was among various shortcomings of the £500bn investment platform market highlighted by the FCA in an interim report published last week as part of a two-year investigation that began last summer – see more details of the report here – City Watchdog challenges DIY investment platforms on fees and transparency.

The regulator found competition between providers was ‘not working as well as it should’, that barriers to switching are ‘significant’ and ‘could limit the pressure on platforms to provide continued value for money’.

‘This is a market that has seen significant growth in the past five years, with more customers than ever deciding to use a platform to manage their money,’ said Christopher Woolard, executive director of strategy and competition at the FCA.

FCA said that the orphan clients were particularly badly served by the industry.

According to Times Money, in most cases, they will have found themselves in this position because they were introduced by an adviser to an affiliated platform, but have since stopped receiving advice — either by choosing to no longer pay for advice, because their adviser has gone bust or now considers the client unprofitable, or they have simply lost touch.

Many stick with the platform they were introduced to, and continue to pay higher fees; this could be because of inertia, or because they don’t feel sufficiently well informed or confident to make the right choice.

‘a 9% rise in the number of clients orphaned between 2016 and 2017, and that they collectively now have about £10bn of funds’

FCA is considering banning the extra charges faced by non-advised customers, and said the problem was growing; it found a 9% rise in the number of clients orphaned between 2016 and 2017, and that they collectively now have about £10bn of funds under management.

It said it would require firms to encourage them to switch to cheaper DIY investment platforms, which have boomed in recent years as more people conduct their own research online rather than rely on an adviser; the idea that clients should be charged an additional fee when they no longer have an adviser flies in the face of FCA’s push for competition and transparency.

How the charges work

FCA says that 83% of adviser fees – ranging from 0.5% to 1% p.a. – are paid by clients via their investment platform rather than directly; investors can stop paying them at any point by notifying their platform, but although the adviser fee is switched off, the platform may then levy an additional charge.

Times Money says that Transact charges its 3,700 adviser-free clients 1% a year for investments or pension pots worth up to £60,000, but only 0.5% for those who use an adviser.

New investments for non-advised clients also incur a chunky 3% charge while advised clients pay only 0.05%; effectively charging typical financial advice fees, while giving no advice.

Transact says the additional cost covers ‘extra administrative charges’ it incurs in handling non-advised clients.

Novia charges its 900 non-advised clients 1% on investments up to £250,000, but 0.5% for those still using an adviser; it said the extra fees were also to cover the additional admin the platform takes on:

‘When an investor has previously relied on an adviser the level of communication tends to be high.

‘Transact says the additional cost covers ‘extra administrative charges’ it incurs in handling non-advised clients’

‘Also, investments are not simple and staff handling investor queries need to be highly trained. We tell clients on numerous occasions Novia are an advised platform so please find another adviser in order to receive value for money.’

Meanwhile, AJ Bell charges a £200 annual fee to its 1,400 clients who have stopped using an adviser but remain on its ‘advised’, Investcentre; the company told the Times that orphaned clients constituted less than 2% of its client base and it encouraged them to appoint a new adviser or transfer to a DIY platform:

‘Where they do not, we make an additional charge of £50 per quarter to cover the additional administration costs as a result of there being no adviser,’ it said.

Novia and Transact charge no fees to transfer funds elsewhere and say they actively encourage orphan customers to seek another adviser or switch to a DIY platform, AJ Bell charges £75 to transfer cash to another platform and £25 per holding for funds; customers should be diligent in transferring to lower-cost platforms if they no longer use nor need advice.

Most orphan clients are with providers that do not charge extra for not having an adviser, but do levy significantly higher charges compared with DIY platforms.

One of the biggest, Standard Life, told Money it had about 7,500 orphaned clients with an average portfolio size of £30,000. It does not charge them more if they no longer receive advice, and there are no penalties for transferring, but those that stay can be paying up to 0.55% annual platform fee.

According to a calculator on the Candid Money website, a client stuck with Standard Life with a £30,000 portfolio on its Wrap platform, achieving 6% annual growth, would accrue £51,002 in 10 years, after fees of £2,724,

By moving to a DIY platform such as Charles Stanley Direct, which charges 0.25% a year for the first £250,000 invested, they would pay £1,254 in charges, making their pot worth £52,471, excluding dealing commissions and other account fees.

Standard Life said it actively encouraged orphan clients to seek a new adviser if they no longer want advice and that most of its orphaned clients were on its Elevate platform, with a maximum annual charge of 0.36%.

Hargreaves Lansdown, Britain’s largest DIY investment platform, charges a maximum 0.45% on investments up to £250,000, falling to 0.1% on funds above £1m and 0% on sums above £2m.

How to choose a platform

There are a range of considerations for those choosing an investment platform and the key is to find the one that best fits your personal circumstances.

Fundamentally, do you require financial advice, or are you comfortable as a DIY investor? How many times you will trade each year? Will you buy funds or shares? Are you are investing in an ISA or a SIPP and what is the value of your holdings?

If you want to switch between platforms, it is generally more expensive if you want to move funds rather than cash; eg Hargreaves Lansdown charges £25 to transfer each fund but a total of £25 to transfer cash.

It can be cheaper to convert funds to cash before transferring, although you will be out of the market while the transfer takes place; some levy account closure fees. Some providers offer both an advised and non-advised platform and the former can be cheaper.

With a wide range of platforms available, and the variations in the fee structure, it is worth investing some time in researching before you take the plunge because it may be a difficult situation to unpick later.

One thing’s for sure, if you are stuck on a platform and paying too much in fees despite not having an adviser, you should be diligent in transferring out because however much they say they intend to inform you, the platform will not be begging you to stop paying those fees.

Brokers Commentary » Brokers Latest » Commentary » Equities » Equities Commentary » Equities Latest » Latest » Mutual funds Commentary » Mutual funds Latest

Leave a Reply

You must be logged in to post a comment.