Jul

2023

UK shares: the 70% shot at beating cash

DIY Investor

5 July 2023

While the UK’s official Bank Rate may have hit 5%, being boring and sticking with UK shares over the long term will give you the better chance of beating inflation – by Graham Ashby

With savings rates rising rapidly we know many conversations are being had about long-term investing versus cash deposits (see With cash earning 5%, why risk money on the stock market?). As a fund manager investing in UK shares, you can expect me to keep making the case for them.

The circumstances of every saver are different, and some may have excellent reasons to be holding cash. But it’s worth reiterating that just because the Bank of England increased the Bank Rate to 5% last month, it does not mean that cash will give you the best chance of keeping pace with inflation and preserve its spending power.

These are some of the thoughts I’m having when observing sky-high demand for “cash” products – including a current clamour for cash ISAs or indeed “money market funds”. The latter invest in products with cash-like properties and certain bonds, including UK gilts, on which it is hard to imagine the British government reneging on coupons.

When a “boring” investment philosophy gets interesting

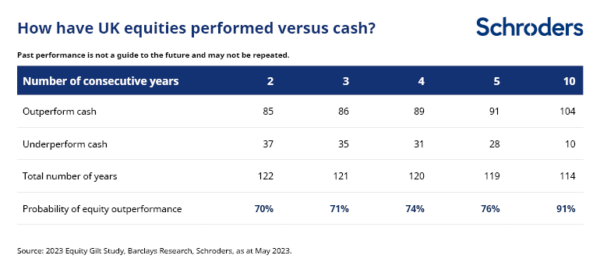

The below table is taken from the latest annual refresh of the 123-year Equity Gilt Study. As the report pinged into my inbox it was a timely reminder of the power of UK shares to outperform UK cash over the long term, and give the better chance of beating inflation.

The study is a comparison of UK shares, or equities, versus UK cash and UK bonds. Other studies draw similar conclusions for other territories.

For me, the standout stat of the 2023 report is the 91% probability of UK equities outperforming cash over any 10-year period in the past 123 years. Meanwhile, over two, three, four and five years, the equivalent probability was 70% or above (and more than 60% versus gilts for all of the aforementioned consecutive, or “rolling” timeframes).

This data is very interesting and supportive of a “boring” investment philosophy.

Being focussed on UK shares offering the prospect of a reliable and growing stream of dividends, my team and I often think in terms of decades, rather than years.

It’s what could be seen as a boring investment philosophy – versus some investors who are more focussed on companies with fast-growing toplines, rather than profitability and cashflows, out of which dividends, ultimately, are paid.

It’s a philosophy, however, where it also pays to think probabilistically, and to look at data over very long and varying periods of time. Hence the idea of rolling periods, encompassing all variety of past investment environments, rather than just the “last” 10, or 20 years.

The latter can provide enticing headline statistics, but may be misleading if you’re heading into a entirely new investment regime.

Looking at the world in a “probabilistic” manner

Looking at the investment world in this way also suggests that the balance of probabilities supports the idea that UK equities give you a better chance of beating inflation over the long term than cash.

So they are more likely to help your spending power to hold up over time (although shares are more volatile, so investors who opt for stock markets over cash need to be prepared for a bumpy ride).

The message is simple: be boring, stick with UK equities over the long term and you’ll have a better chance of beating inflation, on the balance of probabilities.

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.