Aug

2022

UK interest rates: What next?

DIY Investor

10 August 2022

Interest rates in the UK and elsewhere are forecast to continue rising as central banks battle to contain inflation. We keep track of what these changes mean for markets and economies – by Simon Keane

TUESDAY 9 August – oil majors: an investment bright spot amid high inflation, rising interest rates and slowing growth?

The UK oil sector increased dividends by 41% in the second quarter of 2022 compared to the second quarter of 2021 (see UK Dividend Monitor Q2 2022).

This arguably makes it an investment bright spot at a time when many countries, including the UK, are grappling with an inflation problem. Interest rates may need to rise significantly, possibly tipping economies into recession.

All the while, geopolitical uncertainties seem unlikely to abate soon (see What is the outlook for UK dividends in a less certain world?).

Sue Noffke, Head of UK Equities, said: “Many companies are now seeing inflation all the way through the supply chain from transport costs to materials prices, as well as higher wages, which they are struggling to pass on to their end customers, including under-pressure consumers.

“Investors in these businesses also have to consider the impact of taxes, including one-off levies, such as the 25% windfall tax on profits of oil companies operating in the UK and UK Continental Shelf, to apply until the end of 2025.

“We could see ‘stagflation’ when growth is low or slowing at the same time as inflation remaining high or rising. Major oil companies are highly cash generative businesses when oil prices are high and benefit from inflationary or stagflationary economic environments.

“The windfall tax reduces the attractiveness of investment in the UK at a crucial time for both energy security and funding energy transition. That said, as a proportion of their total size, the UK operations of the oil majors is small, and the impact on their share prices and values has been small too.”

THURSDAY 4 August – inflation unlikely to fall back as much as the BoE forecasting

The Bank of England (BoE) has raised its main policy interest rate, or the Bank Rate, from 1.25% to 1.75%. The Bank also published new economic forecasts. It expects consumer prices inflation (CPI) to rise to more than 13% in the fourth quarter of 2022 (more than when it last updated its forecasts in May) and eventually fall back after the UK enters a recession.

Azad Zangana, Senior European Economist and Strategist, said: “Looking ahead, the Bank is likely to keep raising interest rates even if it believes it has already done enough already. It may then be able to pause once inflation peaks, and the focus of the public turns towards the recessionary environment.

“Where we differ from the Bank in its assessment is that we do not believe that inflation will fall back by anywhere near as much as the BoE is forecasting. We see greater domestic inflationary pressures building, which will require even higher interest rates.

This is likely to stop the Bank cutting interest rates in 2023/24, as suggested by its forecast, but instead continue to maintain above neutral rates for longer, with the hope that inflation returns to target over a longer period of time.”

WEDNESDAY 13 July – UK’s return to growth piles rate rise pressure on BoE

The Office for National Statistics confirmed today the UK economy enjoyed a strong month in May, growing by 0.5%, after shrinking 0.2% in April. This has potential implications for monetary policy.

The Bank of England (BoE) has to essentially “tighten” monetary policy, including raising interest rates, to restore balance between demand and supply of goods and services.

Schroders experts believe today’s news should further pressure the BoE to up the pace of interest rate rises.

Azad Zangana, Senior European Economist and Strategist, said: “This news should raise pressure on the BoE to raise interest rates faster to combat heightened inflation.

“The next BoE Monetary Policy Committee meeting on 4 August should deliver at least a 0.25% increase in interest rates.

“The argument for a larger rise, however, is strengthening.”

FRIDAY 1 July – rates for new mortgages rise 30% in six months

The “effective” interest rate – the actual interest rate paid – on newly drawn mortgages rose from 1.5% in November to 1.95% at the end of May, according to Bank of England data published today.

In December the Bank of England (BoE) became the first central bank of a G7 economy to raise interest rates since the pandemic. Mortgage costs, which are linked to Bank Rate, have risen as a result.

How significant is this to the UK housing market?

Azad Zangana, Senior European Economist and Strategist, said: “It is no surprise to see mortgage rates rise following the start of the rate hiking cycle by the Bank of England.

“Moreover, expectations of further rate rises are already feeding into the mortgage market.

“However, with the demographics of homeowners aging considerably over the past decade, the majority of households are mortgage free. In addition, most households have been able to take advantage of those low interest rates and had fixed their mortgages.

“This means that it will take longer for rising mortgage rates to have an impact on households and therefore house prices, though first time buyers are the first to feel the pain.”

WEDNESDAY 22 June

UK consumer inflation edged up to 9.1% in May, according to the Office for National Statistics. This is based on the annual change the Consumer Prices Index (CPI), as used to track the price changes facing end consumers of goods and services.

The Bank of England (BoE) raised the Bank Rate by 0.25% last week to 1.25%, but warned it may have to “act forcefully” to tame inflation.

Our economists here at Schroders currently see UK base rates peaking at 2.25% in the first quarter of 2023.

Interest rates, however, may rise more than they’re anticipating in order to head off “second round” effects, they caution.

As the UK grapples with a national rail strike over pay and conditions, there is a risk the dispute may have wider implications for wages and inflation in other industries.

Our investment experts, however, remind us that not all companies are equally affected by inflationary pressures.

Those with “pricing power” may be better placed to recoup higher production costs by successfully raising prices for consumers.

How do second round inflation effects drive interest rates higher?

Azad Zangana, Senior European Economist and Strategist, said: “The risk is skewed towards even more rate rises, as signs of second round inflation pressures are becoming more evident, even if the BoE is not concerned by them yet.

“Second round pressures can occur as higher wages drive inflation higher still, at risk of round after round of wage and price rises, with expectations of inflation becoming a self-fulfilling prophesy.

“Because of the UK energy price cap we have not seen the full pass-through yet of energy price inflation. Most forecasters are looking for inflation to head to around 10% by the end of this year and stay quite elevated for most of next year as well.

“If you look at the consensus figures for next year, the UK is again forecast to be one of the highest in the developed world.

“The biggest area of risk with regards to worker disputes is going to be the public sector because a lot of the public sector pay settlements have been around 1-3%. And given where inflation is heading, that means very big pay cuts in real terms.

“On the private sector side the risks are less. Companies have been able to offer at least temporary bonuses to help with the cost of living, and we’ve seen a number of companies do that in recent weeks.

“That’s helpful since it reduces the pressure on the workforce in the near-term but at the same time doesn’t lock the companies into a permanent pay increase for following years. “

What are the implications of high inflation for investors?

Jean Roche, UK mid cap fund manager, said: “There are UK businesses with sufficient pricing power to withstand inflation raging at 9%.

“Despite the dire headlines we’ve seen companies in the retail, housebuilding and construction sectors report upbeat trading in recent months.

“There are plenty of specialist retailers catering to better-off households with cash to spend. Some of these companies with very niche products will be better able to pass on their own rising costs further supporting their earnings.

“Meanwhile, some areas which may appear discretionary are, to a degree, essential items, such as pet services, for instance.”

“Those companies with pricing power could come into their own as they’re better able to mitigate the impact of shortages and higher costs being experienced in many major economies at present.”

TUESDAY 7 June

Prime Minister Boris Johnson last night won a no-confidence vote, albeit by a smaller margin than expected (211 to 148 votes). The result is not anticipated to have immediate economic or market consequences.

However, at a time of high inflation and interest rate rises, investors are closely watching how political uncertainty might impact government spending plans.

Sue Noffke, head of UK equities, said: “The vote result is not a sea change as markets have already been pricing in political uncertainty. It wasn’t, however, the comfortable win he would have hoped for.

“We are asking ourselves if the government might bring forward spending plans to improve its popularity in the polls. The chancellor has scope to bring forward spending that he might have otherwise left until the autumn.

“If this were to happen, it might stoke inflation, which would make the Bank of England’s (BoE) job more difficult. Like most central banks around the world, the BoE is slightly behind the curve with raising interest rates.

“The Bank is assuming, however, that economic growth cools as inflation eats into real incomes and demand. Were the government to decide to accelerate its spending it may make it harder for the bank to control inflation.”

Azad Zangana, senior European economist and strategist, said: “Yesterday’s result was pretty poor, but it’s likely the prime minister will survive given he has a strong and loyal cabinet behind him.

“Also, we’re not expecting any change to the rules prohibiting another vote in the next 12 months.

“The government has lots of spending plans coming at a time when it’s under pressure due to high inflation and rates rising.”

“Longer term, however, we’ve not seen the tax cuts it will need to deliver to keep the party faithful onside. “

FRIDAY 27 May

As the Bank of England raises interest rates to cool inflationary pressures the UK government is simultaneously taking steps to alleviate the squeeze on the consumer.

On 26 May Chancellor Rishi Sunak unveiled an additional package to help households facing an expected further rise in energy bills this autumn.

How will markets react?

Sue Noffke, head of UK equities, says: “The chancellor’s measures will offset some of the impact of higher energy prices later this year, particularly for the hardest hit UK households.

“The ‘squeezed middle’ is getting a little bit more help to muddle through and then we have the better off able to draw on savings accumulated during the pandemic. There’s a dichotomy in the market.

“So, we’re seeing discount retailers which offer value for money for the ‘have less’ holding up well while luxury sectors serving the ‘haves’ are also proving resilient.

“More broadly, the strongest companies may well increase their market share. And don’t forget valuations – the shares of many consumer discretionary companies are already discounting tougher times ahead.

“The de-ratings we have seen are somewhat indiscriminate, affecting both companies whose earnings have proven resilient as well those in the more exposed sub sectors.”

Jean Roche, UK mid cap fund manager, says: “Household goods spend tends to be more resilient than, say, clothing in a downturn.

“At the moment, we can see this sub sector holding up well in retail sales data, despite the dire headlines.

“Strong demand for both new and second hand homes, as well as ongoing working from home trends are supporting the sub-sector.

“Meanwhile, don’t forget UK households overall have accumulated c.£200 billion of excess savings over the last two years.”

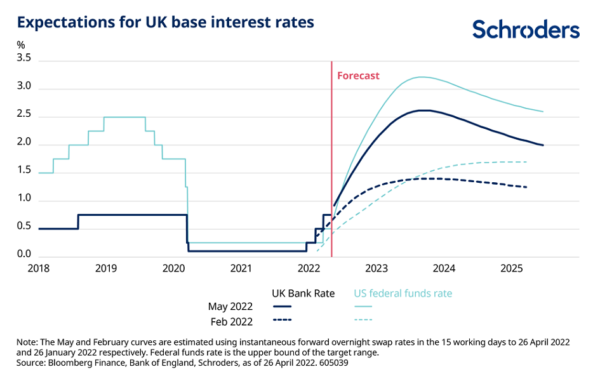

UK interest rates: current position and forecast

The Bank of England (BoE) raised UK base interest rates – the so-called “Bank Rate” – from 0.75% to 1% at the start of May.

At the same time, it published market expectations for where rates might be heading, as shown below.

Compared to February when the BoE conducted the same exercise (see the dotted line), the Bank Rate is expected – on average – to be around one percentage point higher over the next three years.

Higher rates of course mean higher borrowing costs. The move is designed to dampen economic activity by reducing consumer demand for goods and services, as well as the amount companies spend and invest.

Our economists here at Schroders currently see UK base rates rising to 2.25% in the first quarter of 2023 – more than twice their present level.

Super-high interest rates: will a re-run of the 1970s be avoided?

Given the current inflation problem, the central bank may need to keep raising rates even at risk of economic activity. The cost of not taking action could be a situation not seen since the 1970s, when the only way to bring inflation back under control was to aggressively raise interest rates and cause a very deep recession.

“After much dithering, policymakers at the Bank of England appear to have decided that interest rates need to rise significantly in order to tackle inflation, even if it means tipping the economy into recession”, said Azad Zangana, senior European Economist and Strategist.

“They will, of course, want to avoid a recession, but even with its own forecast, the BoE has inflation peaking at around 10% at the end of the year, and the economy contracting. It will hope that it can reduce domestic demand and ease wage pressures without causing too much damage to the economy.”

The BoE’s 10% peak annual consumer price inflation forecast is causing understandable alarm and its governor Andrew Bailey has described food supplies currently trapped at port in Ukraine as a “major concern”. But this headline rate is not the one most occupying the thoughts of economists. They are focused on “core” inflation in the economy, and what’s driving it.

Getting to the “core” of inflation

By stripping out volatile items such as oil and food, core inflation gives a clearer picture of underlying price trends. Core items include essentials such as education, telecoms and healthcare costs, as well as “discretionary” or non-essential items, such as meals in restaurants and other entertainment costs.

Without careful economic management, there is a risk we could see round after round of wage and price rises of core items resulting in destabilising “wage price spirals”. Here, expectations of inflation become a self-fulfilling prophesy. Prices climb – or become “unanchored” – as a result.

“The main risk for the UK economy is that the largely external price shock caused by higher energy prices causes domestic prices to respond, followed by wages,” said Zangana. “To some extent, we are already seeing evidence of this occurring.”

When does the Bank of England next meet to decide on interest rates?

The next key date for UK interest rates will be 16 June when the BoE’s Monetary Policy Committee (MPC) convenes again to debate further changes in the Bank Rate.

The UK labour market is currently “tight”, meaning unemployment is low and there are many job vacancies that companies are struggling to fill. This is due to a variety of reasons, a number of them related to the pandemic, which have prompted some workers to withdraw from work.

The latest data show that for the first time on record there are more unfilled job vacancies in the UK than unemployed people available to fill those jobs.

“In the past, higher demand for labour would have been met by migrants, particularly from the EU,” said Zangana. “Covid can take some responsibility for the recent slowdown in immigration, in addition to Brexit. This is making it easier for domestic workers to demand higher wages. The risk of course is that higher wage growth leads to ongoing strong demand, and further inflation.”

“After one member of the MPC voted to not raise rates at all in the March rate-setting meeting, three members voted for a half-point increase in the Bank Rate in May,” said Zangana. “Despite their hawkish rhetoric, we doubt that policymakers will actually hike the economy into recession.”

Five key questions about interest rates answered

Why have interest rates been rising?

In December 2021, the BoE became the first central bank of a G7 economy to raise interest rates since the pandemic. This formally began the process of these major industrialised nations “normalising” base rates, or “monetary policy”, from the emergency settings introduced in response to Covid-19, when they were cut close to zero to support economic activity.

As vaccines were deployed, economies re-opened and demand for good and services reignited. However, there have been shortages of materials, energy and transport due to Covid disruptions. This has resulted in delays, increased costs for producers of goods and services, and fed through into higher consumer prices, as tracked by the Consumer Prices Index (CPI) in the UK.

Covid is also continuing to play a role through the recent mass lockdowns in China, while Russia’s invasion of Ukraine is disrupting energy and food markets.

Why do higher interest rates matter?

On the assumption that inflation will eventually be tamed, monetary policy normalisation has driven up long-term return expectations for interest rates in real (adjusted for inflation) terms. During the closing months of 2021, markets began to price in higher base rates (reflected in higher rates on government bonds,and deposit accounts) even before the central banks began actually raising rates.

For many years investors have become used to the idea that cash left on deposit will lose value in real terms. That is, the interest gleaned will not keep pace with inflation. By the end of 2021, however, the expected annual return over the next 30 years on sterling cash had crept 0.1% higher (to -0.3% per annum) than where it had stood at the end of 2020 (Schroders forecasts).

True, -0.3% is capable of reducing the real value of £100,000 today to something closer to £90,000 worth of equivalent goods and services three decades in the future. Still, it’s been a small step in a more positive direction for long-term savers. That is assuming central banks are increasing interest rates to restore so-called “price stability” and bring inflation back under control, but at what cost?

Could higher interest rates result in a recession?

The BoE has to essentially “tighten” monetary policy, including raising interest rates, to restore balance between demand and supply of goods and services. This is required to ease wage pressures and avoid a threatened “wage price spiral”, where inflation expectations become a self-fulfilling prophesy. There are, however, questions about whether inflation can be tamed with only gradual tightening to deliver a hoped-for soft economic landing without crashing the economy.

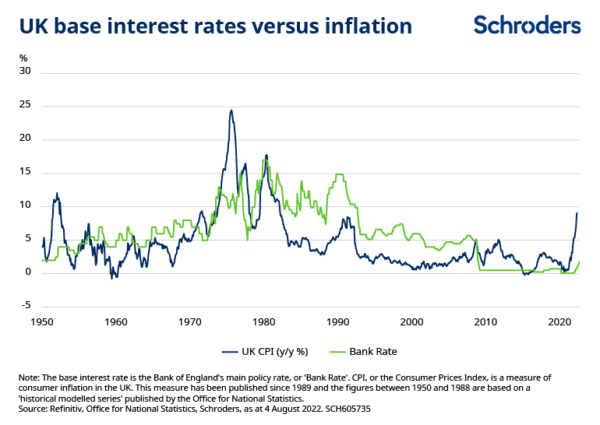

Parallels are being drawn with the 1970s – what happened then?

Experts say if policymakers are not careful, the country could end up in a situation akin to the 1970s. At that time inflation was only brought back under control after interest rates were aggressively increased at the cost of a very deep recession in the early 1980s.

Many of the world’s major economies suffered from a combination of slow growth and high inflation, or “stagflation” during the 1970s. Oil prices rose sharply due to external events (two oil shocks resulting from war and then revolution in the Middle East) and wages were rising in Western economies as they struggled to adjust to the new realities. Wage-price spirals resulted and prices became unanchored.

In the UK, this meant CPI inflation peaking at 24.5% in August 1975 as the country was enduring its second recession in two years. There were seemingly few solutions to a dismal decade which culminated in the so-called Winter of Discontent of 1978/79.

Then the second oil shock of 1979 coincided with some major political changes in the West, culminating in the UK with the election of a new Conservative government in May 1979. As part of these changes, “monetarist” policies were adopted and interest rates were increased by 5% within six months, from 12% to 17% (the high in the period since 1950) which was maintained until July 1980.

UK inflation subsequently began a very long retreat, from a second peak of 17.8% in May 1980. The missed opportunities of the 1970s, however, arguably, came at the greater cost later to an economy forced into a deep recession, with millions left unemployed.

What is quantitative tightening (QT)?

All major central banks deployed unconventional policies in the wake of the global financial crisis of 2008, when conventional ones such as cutting interest rates were exhausted. They then reactivated these programmes in response to pandemic-related economic shutdowns. Most have either ended these schemes, or are poised to reverse them.

Central banks have accumulated large quantities of government bonds under quantitative easing (QE) programmes – the purchase of such bonds was used to inject money directly into the financial system and lower the cost of borrowing for households and businesses. These bonds on their balance sheets now look set to be gradually run down; to be sold back into the market in a process of quantitative tightening, or QT, which will raise the cost of borrowing in the economy.

![]()

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.