Jul

2021

Time to back Britain?

DIY Investor

21 July 2021

After a challenging period for the United Kingdom, we wonder if it could be the most exciting market on a five-year view…

After a challenging period for the United Kingdom, we wonder if it could be the most exciting market on a five-year view…

The UK was the most unloved market among fund managers during the post-referendum period. From 23 June 2016 to the end of September 2020 (just before the vaccine rally), the FTSE All Share fell 3.5% in dollar terms, with the MSCI AC World Index up 50.5%, thanks in part to the pound falling 12.9% in USD.

Even as late as April this year, fund managers were underweight the FTSE All Share, according to the BofA ML Fund Managers Survey – managers were around 1.5 standard deviations below their historical average positioning. This was despite the market being one of the best performers in the reflationary rally. Since 1 October 2020, the FTSE All Share is up 37% in dollar terms compared to 27.2% for the FTSE World ex UK, helped by a 7.9% jump in sterling versus the dollar.

Remarkably, the same survey in May found that fund managers were 1.5 standard deviations overweight versus their historical average. Why are fund managers suddenly so positive on ‘plague island’, as the charmers at the New York Times dubbed their favourite holiday destination?

A shot in the arm

In the short term there may have been a vaccine boost to sentiment towards the UK, as its faster rollout allowed it to open up some activities earlier than countries on the continent. However, current restrictions in EU countries are now very close to the remaining restrictions in the UK, despite lower vaccination rates. In the US, California and New York are the latest states to remove virtually all restrictions – including ‘social distancing’ for businesses.

This is particularly notable as they are blue states, hitherto more cautious on reopening than Republican-controlled states. UK businesses may have the benefit of some momentum due to relaxing restrictions earlier than the EU and some US states, but this seems unlikely to be an advantage from now on or a good reason to buy UK equities now.

Under-owned = under-valued

Crises tend to make a mess of valuations, and this one certainly has. Many businesses were effectively ordered to cease operations, with current earnings disappearing and future earnings in doubt. There was a spike in P/E ratios during 2020 as earnings collapsed.

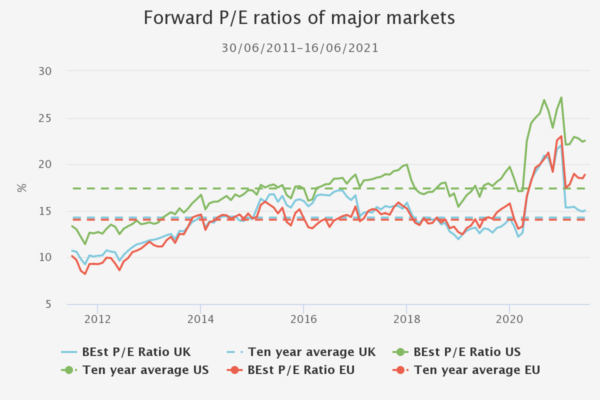

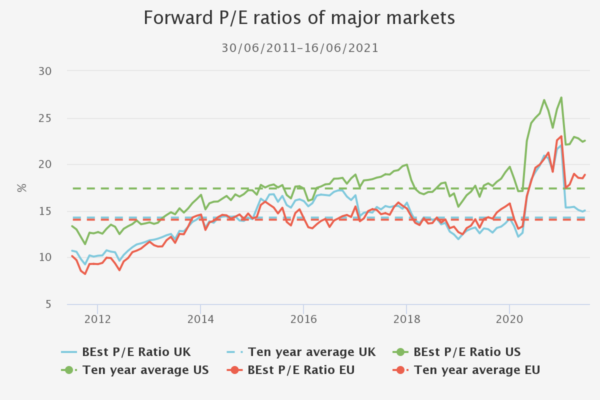

To some extent looking at a forward P/E helps deal with this issue, although if analysts think they have to forecast depressed earnings given their lack of visibility on non-economic developments (i.e. the pandemic) then even this metric can be hard to take too seriously. The graph below shows the ten-year history of this metric for the UK, US and Europe. Valuations are above their long-term average for all three markets, although the UK is much closer to the average than the two major peers.

Source: Bloomberg

This seems to be because the UK market is not reflecting a better earnings outlook. The below graph shows the earnings on an index level according to Bloomberg’s estimates. The UK, US and EU have all seen similar upgrades to estimates since the end of 2020 as an exit from the pandemic seems more assured. But despite the UK’s faster share price appreciation, it has still not closed the valuation gap.

One thing that stands out to us, is that the period just prior to the Brexit referendum was a bit of an anomaly. The UK market’s valuation exceeded Europe’s and closed in on that of the US. The UK economy was booming in this period – in 2014 the unemployment rate fell below 6% and in 2015 below 5% – which may have helped boost sentiment. Forward earnings on the market had also been higher for some years, with UK companies enjoying improving profitability. However, there was generally a very healthy economic environment in the developed world too – i.e. in the UK’s major trading partners such as the US and the Eurozone. We consider whether there might be some parallels to the current situation later on.

The Home Guard

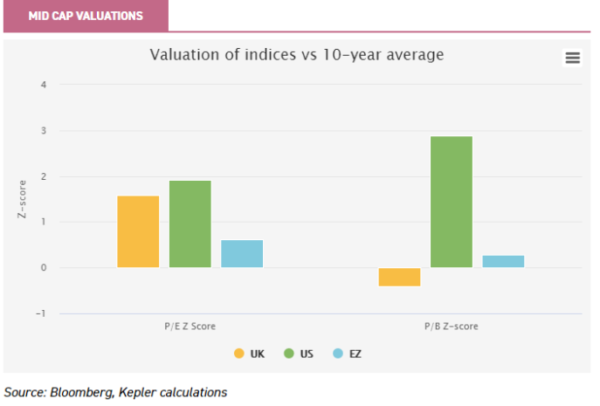

Looking at valuations then, there still appears to be a case to be made for over-weighting the UK on those grounds. Interestingly, the largest valuation discount appears in the small cap segment of the market. This may reflect a lingering effect of Brexit uncertainty, with the more domestic leaning of the SMIDs leading them to be on a wider valuation discount. We note that it is wrong to see the FTSE 250 or even small caps as domestic indices, however. The FTSE 250 has historically had around 50% of its revenues earnt abroad, as has the Numis Smaller Companies Index. This throws up good stock specific opportunities when the market sells off indiscriminately on concerns about the domestic economy.

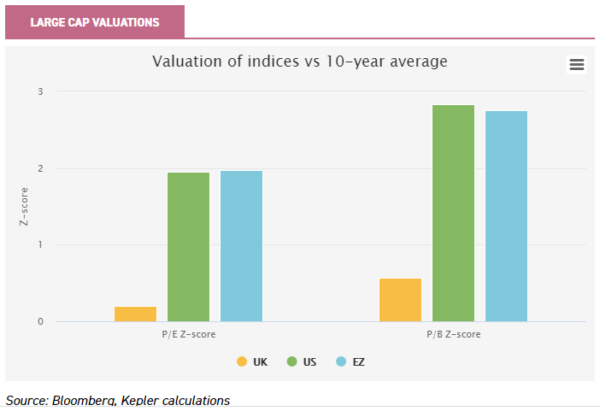

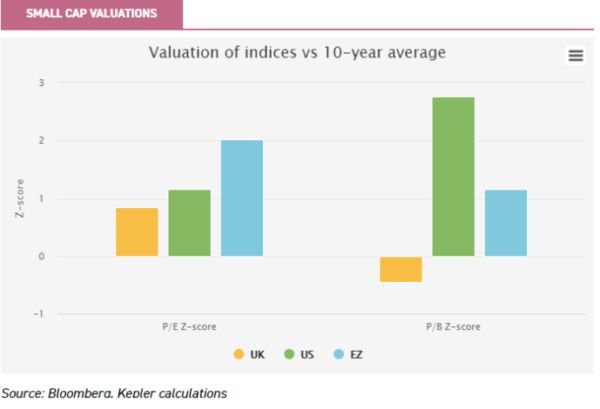

UK large caps may be on less advantageous valuations because of their inherent cyclicality and value bias (which we analyse further below). Indeed, the recent improvement in the UK’s relative performance may be a result of this drawing more investor attention in the reflationary environment following the successful vaccine trials. Commodities, banks and GBP were among the consensus overweights in May this year, as well as the FTSE. Even so, the resurgence in interest towards value and towards cyclicality has not left UK large caps looking expensive relative to their history or their peers, which could mean there is plenty to run in this trend. We would expect foreign investors who become positive on the UK to invest in large cap or all cap indices first, and then perhaps look to increase their weighting to the SMIDs later on. In the below charts we look at the relative valuations of major markets, considering price to book as well as forward P/Es, which reduces the impact of analysts’ forecasts on valuations. There is a similar picture, although the UK still looks cheap relative to history on this metric rather than simply compared to peers.

Source: Bloomberg, Kepler calculations

Closing the lingering Brexit discount is one potential source of excess returns from the UK market. We think getting any sort of Brexit deal reduced uncertainty and led to sentiment starting to return towards UK equities. However, investors still have to bear in mind the potential for the unravelling of the Northern Ireland Protocol, which could put tariff-free trade with the EU in doubt.

If the protocol were to last four years, then the Assembly could vote to repeal it and the UK and EU would have to renegotiate it. It seems it may not last that long though, given its unpopularity with Unionists. The UK may be considering invoking Article 16, allowing it to unilaterally take measures in contradiction of the protocol before the four years are up. In that event, the whole trade agreement with the EU may well come into doubt, which could see some investor aversion to investing in the UK.

For this reason we think sentiment is probably still more depressed towards the UK than it could be, which is potentially both an opportunity and a threat. As and when more trade deals are signed by the UK (following the agreement reached with Australia), this could have less and less importance, and so we think the discount is still likely to dissipate over the medium to long term.

The wheel turns

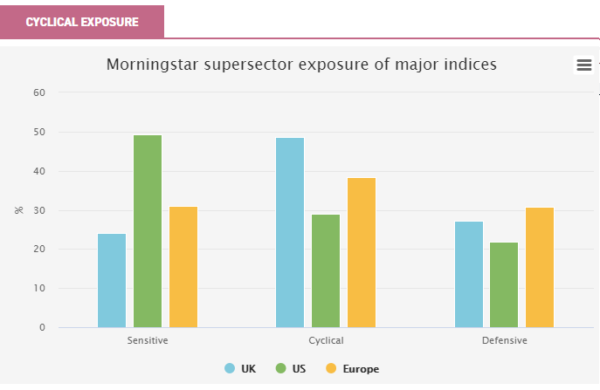

The cyclicality of the UK stock market is a key element to consider, and it may help explain why the UK is suddenly in favour with fund managers, and why the earnings outlook is so much better than our global peers. Looking at Morningstar’s ‘super-sector’ classification, almost half of the FTSE 100 is in cyclical sectors (48.6% to be precise). For the S&P 500 the figure is just 28.9% and the MSCI Europe index it is 38.3% (see chart below). These don’t perfectly correlate with the traditional value sectors, but this is an interlinked exposure. The FTSE’s exposure to energy, basic materials and financials is worth 40.2% of the whole index compared to just 16.8% in the S&P 500 (and 29% in the MSCI Europe). Perhaps this helps explain why the UK market has performed strongly in the reflationary rally since Q3 2020.

This cyclicality and the weighting to value stocks led earnings to come under pressure during the pandemic, but now we are in the recovery phase, this has turned into a tailwind. Indeed, the UK’s earnings recovery is one reason why the latest JPMorgan Long Term Capital Market Assumptions now forecast the UK market to have the highest return potential out of all developed world markets over the next five years – and only marginally below the expected return from emerging markets. A second reason is the lower starting valuations.

As we show above, it is not that the UK is necessarily cheap relative to its history, but that valuations are less expensive, and so long-term returns won’t be as hindered as other markets by any reversion towards the mean. The US in particular is likely to see its starting valuations bring down prospective returns according to JPMorgan, after a current cycle of US outperformance which has lasted over ten years.

Given the high weighting to traditional value areas and low weighting to growth, the UK could be a beneficiary if we see a change of regime to a period of high inflation or if we see an interest rate hiking cycle. On the other hand, current inflation numbers are being exaggerated by base effects, as the initial impact of the pandemic saw a cratering in economic activity and commodity prices.

Once that has washed out of the numbers, there will be lingering effects of unemployment (not everyone will survive furlough) and behaviour change (not everyone will go back to their old consumption patterns) which may depress prices. In the meantime, businesses will have debts to pay off from periods of closure or restricted trading, rather than investing for the future. It is quite plausible that we see a period of relatively sluggish growth which keeps rates low, and that inflation numbers come down close to policymakers’ 2% targets. In which case the UK will have to offer more than just value and cyclicality to attract buyers, but growth too.

Is the UK just a value story?

We think it is meaningful that in the final quarter of 2020 three fund managers attempted to launch new investment trusts investing in the UK, even if demand was there for only one of them in the end (Schroder British Opportunities). Clearly professionals see a real opportunity in the market over the medium to long term. Starting valuations are one part of this picture, as we have seen above.

In recent months, the cyclicality of the UK market has also attracted flows. We think the UK still looks attractive as a recovery story, with international investors only now looking at the market more seriously after years of under-owning it. That said, some of the global reflationary/recovery trends which have been supportive in recent months may have peaked, with industrial commodities weak in recent weeks and CPI numbers possibly at their peak – given the base effects from weak comparable months in 2020 are at their height.

This means that it is probably wiser to look for growth stories and individual stock picks than hoping to make easy gains by buying the index. In particular, the small and mid-cap space looks interesting on valuation grounds. It is here perhaps that there may be the best stock-specific opportunities in companies that have been weighed down by sentiment towards UK plc as a whole, after the Brexit vote and the pandemic hit the country hard.

Join us live to discuss the outlook for UK equities

In our live online event on 1 July we will hear from six UK fund managers about their view on the opportunities in the UK market and how their portfolios stand to benefit. The event will kick off with a roundtable, which provides you with an opportunity to put your questions to the experts about the FTSE and the health of UK plc.

EVENT SCHEDULE

| MORNING | AFTERNOON | ||||

| 0900 | ROUNDTABLE | What now for UK plc? | 1300 | ROUNDTABLE | Small is beautiful |

| 1000 | Rory Bateman | Schroder British Opportunities | 1400 | Dan Whitestone | BlackRock Throgmorton |

| 1100 | James Henderson | Henderson Opportunities | 1500 | Judith MacKenzie | Downing Strategic MicroCap |

| 1200 | James de Uphaugh | Edinburgh Investment Trust | 1600 | Georgina Brittain | JPMorgan Smaller Companies |

Date: Thursday 1 July 2021

Time: 0900 – 1700

Place: Online via your browser

The event is free to attend and CPD points will be made available to professional viewers.

Disclaimer – Material produced by Kepler Trust Intelligence should be considered as factual information only and not an indication as to the desirability or appropriateness of investing in the security discussed. Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771. Full terms and conditions can be found on www.trustintelligence.co.uk/investor

Commentary » Investment trusts Commentary » Investment trusts Latest » Mutual funds Commentary » Uncategorized

Leave a Reply

You must be logged in to post a comment.