Jul

2020

The Power of Equality

DIY Investor

21 July 2020

Exchange-traded funds can provide investors with equal-weighted exposure to equity markets, rather than exposure weighted by market capitalisation – Vincent Denoiseux explains the approach

Passive investing in markets is now commonplace. Many investors use exchange-traded funds (ETFs), which track well-known market indexes such as the FTSE100 Index and the S&P 500 Index. The idea is simple. Instead of trying to beat the market return by placing money with a professional portfolio manager who, for a fee, will attempt to outperform the index, you instead pay a relatively low fee to garner roughly the index return.

The concept of passive investing is, therefore, straight forward enough. That said, how many of us think through how the underlying index that is being tracked works? How is the index put together? What rules does it follow, and how might that impact my investment?

Most indexes that track equity markets tend to be weighted by market capitalisation, which means the biggest companies according to what the market prices the company to be worth. The bigger the company by its market value the higher its weighting in the index. Price moves in the largest companies in a capitalisation-weighted index will, therefore, have a bigger impact on the index than price moves in smaller companies that are included.

In recent years, index and ETF providers have started to look at alternatives to weighting by capitalisation as a way to alter the overall risk and return potential of passive investing. These alternatives can be grouped into a category known as ‘strategic beta’ (index investing using a market capitalisation-weighted approach delivers the market return, which is technically termed ‘beta’, as distinguished from returns beyond what the market provides, which is called ‘alpha’).

‘index investing using a market capitalisation-weighted approach delivers the market return, which is technically termed ‘beta’, as distinguished from returns beyond what the market provides, which is called ‘alpha’’

Strategic beta indexes can take many forms – indeed, developing strategic beta indexes has become something of a small industry. The common feature is that such indexes do not use market-capitalisation as the basis for their weighting methodology and that they re-weight the index periodically based on an alternative but fixed methodology. One of the most straight forward strategic beta methodologies is equal weighting.

As the name suggests equal weighted strategies weight the component companies of an index equally, regardless of one company’s size relative to another. An equal weight approach therefore aims to:

- De-concentrate the underlying reference index and therefore reduce the representation of the largest companies.

- Provide exposure to the smaller-cap companies by increasing the weight towards the smaller capitalisation part of the reference index.

- Benefit from a ‘sell high, buy low’ methodology, because companies whose price has increased substantially will automatically have their weighting reduced to maintain an equal-weight presence in the index, and vice versa for companies whose prices have fallen substantially in a short time.

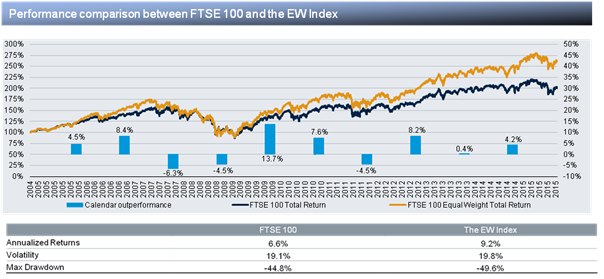

We can see what this means in practice by looking at the FTSE 100 Semi Annual Equal Weighted Index, and in particular by analysing the difference in stock weightings between the FTSE 100 Index and the equal weight version. We found that the equal weight version of the index under-weights around a quarter of the stocks in the FTSE 100 Index (ie, the big-caps), and significantly under-weights some of the really big companies, while providing a small over-weight on the remaining three-quarters of companies in the index. The large-cap bias is therefore removed.

‘The annualised returns of the equal weight index (since 2004) is 9.2 %, compared with 6.6% for the FTSE 100 Index’

The greater diversification of the equal weight index means there is a reduction in single-stock risk. The equal weight methodology also alters the sector weighting. Certain sectors, such as energy for instance, have a relatively high weighting in the FTSE 100 Index thanks to the presence of some extremely large oil majors in the index.

The equal weight version lowers the weighting of the big majors compared with the standard FTSE 100 Index, which also lowers the weighting of the energy sector overall. Other sectors, such as consumer discretionary, get a relatively higher weighting in the equal weight version of the FTSE 100 Index.

So what does all this mean for performance? No one can predict future performance, but we did analyse how the theoretical equal weight index would have performed historically compared with the FTSE 100 Index. The graph below shows this performance comparison going back to 2004. The annualised returns of the equal weight index over this time period is 9.2 %, compared with 6.6% for the FTSE 100 Index. Note however that the equal weight index underperformed during the 2008 and 2011 market corrections.

Note: Past performance, actual or simulated, is not a reliable indicator of future results. The FTSE 100 Semi Annual Equal Weighted Index has no prior operating history before 1 July 2015. All performance data is simulated and calculated by means of a retrospective application of the index methodology before the live launch date.

One important technical feature of equal weighted indexes is how often they re-balance. The index has to be re-balanced often enough to stay close to the equal weighting, but if it re-balances too frequently then transaction costs could significantly impact overall returns.

The FTSE 100 Semi Annual Equal Weighted Index re-weights the underlying stocks every six months (as opposed to, say, re-weighting quarterly), which our research shows strikes a good balance between keeping the stocks equally weighted but without incurring substantial transaction costs for re-balancing the portfolio.

‘Simplicity is the ultimate sophistication’

There is a good chance that more equal weight ETFs will come onto the market in future, especially if more investors start to see the potential benefits of alternatively-weighted indexes.

There is a famous quote by Leonardo da Vinci, which goes: “Simplicity is the ultimate sophistication.” It is an apt quote in relation to equal weighted index investing.

From a straight forward idea to a sophisticated methodology to implement that idea, equal weighting offers an investment solution that is dramatically different to traditional market-cap weighted passive investing.

Commentary » Exchange traded products Commentary » Exchange traded products Latest » Latest » Uncategorized

Leave a Reply

You must be logged in to post a comment.