Jul

2018

The Lady’s not for Investing: Survey reveals 56% of women are failing to save for retirement

DIY Investor

24 July 2018

A YouGov survey commissioned by digital investment manager Scalable Capital found that just 44% of women surveyed had started saving for their future, citing insufficient financial knowledge and fear of unexpected losses as two main barriers.

The company undertook the survey in both the UK and Germany as part of its Women’s Initiative to research the ways in which British and German women are, or are not, saving for their retirement.

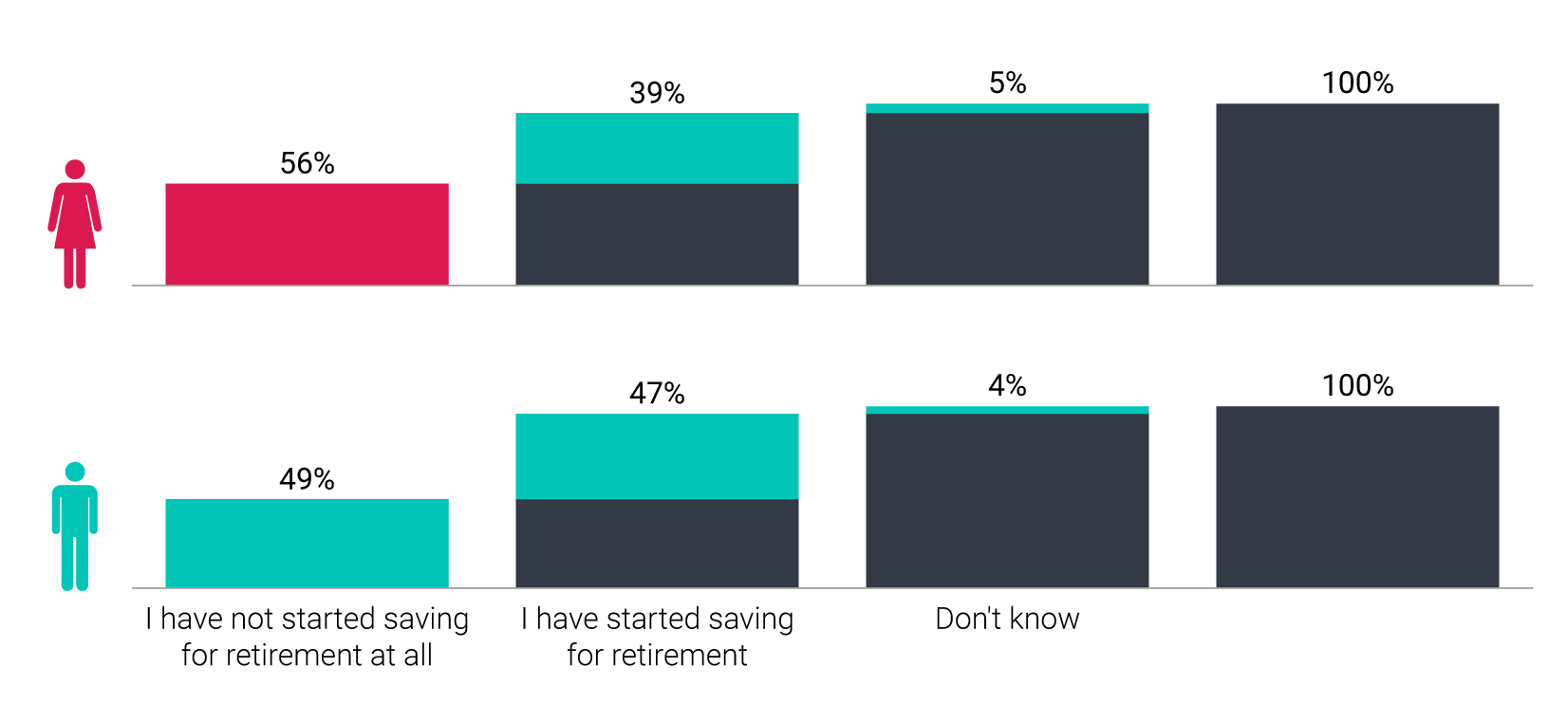

The research revealed that the main concern for over 44% of both men and women in the UK was not having enough money to fund a comfortable retirement; however, 56% of pre-retirement women haven’t yet started saving for their retirement and only 17% of women have ever invested in shares, bonds or other long-term investments.

According to research by Aviva* the fears of the 44% could be well founded as it identified a UK pension gap of £311 billion per year – what is actually being saved vs what would be needed to fund an adequate standard of living in retirement.

In order to close the gap, an average 40-year-old would have to put aside £4,100 each year to achieve the lifestyle they aspire to, yet 56% of pre-retirement women surveyed haven’t even started to save for their retirement.

In truth, men fare little better with 49% yet to take the plunge suggesting that there could be significant societal problems down the line.

Share of All Pre-Retirement Respondents Asked About Their Retirement Savings*

Source: YouGov, February 2017

Men and Women Both Fear Losses

Just 17% of all women surveyed have ever invested in capital markets, compared to 31% of men, meaning that women are disproportionately missing out on long-term growth opportunities.

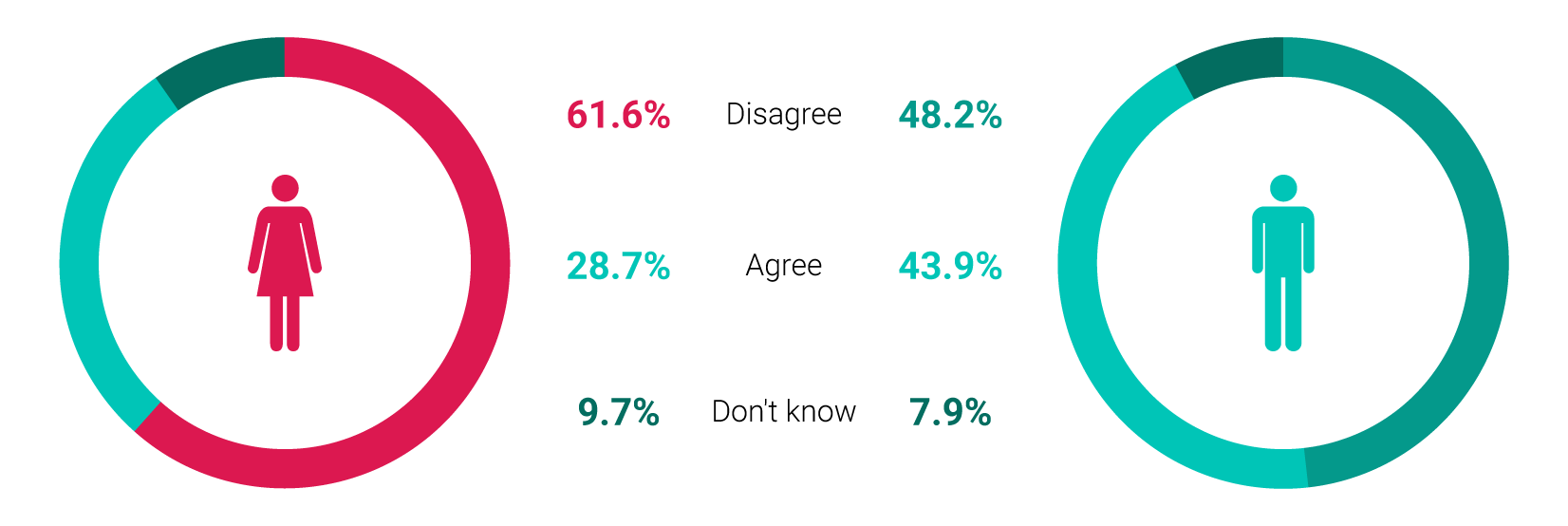

By far the most important reason given for this lack of engagement was the women’s perception of their own financial knowledge; 62% said they do not feel sufficiently knowledgeable to be comfortable with investing, compared to 48% of men – a significant gender variation.

However, the results did not confirm the widely held belief that women were more afraid of incurring unexpectedly high losses than men; 23% of women cited this as a barrier to investing, almost identical to the 22% of men who responded in the same way.

Share of Respondents Who Disagree and Agree That Their Financial Knowledge Is Sufficient*

Source: YouGov, February 2017

The survey did not confirm that women are more risk-averse than men when it comes to investing, rather that the different investment behaviour of men and women was due to the unequal financial resources at their disposal, and the relative lack of financial knowledge of women.

The conclusion is that women aren’t making adequate provision for their retirement and miss out on the long-term growth potential offered by stockmarket investments; the challenge for financial services providers, including the survey’s sponsor, is to make their products accessible in the way that they are presented and attainable by offering affordable levels of entry.

Greater Transparency Required

When asked what would make them more likely to invest in capital markets in the future, most women cited greater transparency around fees and performance, as well as a better understanding of risk.

Women were apparently less cost-conscious than men, with only 13% citing lower fees as a motivation to invest more, compared to 19% of men.

In response to the results of the survey, founder and CEO of Scalable Capital, Adam French, said: ‘Wealth managers need to help investors better understand investment risk. For example, at Scalable Capital we ask clients to select, in percentage terms, how much they are prepared to lose in a bad year. Our technology-driven approach means every portfolio is customised to the individual risk tolerance of each investor. Portfolios are then adjusted according to risk, ensuring that the risk of the portfolio remains constant in all market conditions, limiting unexpected fluctuations. By providing a professional, transparent, low-cost investment service, we can overcome some of the concerns women have about capital market investments and can help them achieve their financial goals.’

Scalable Capital has set out to address the results of its survey by offering discretionary investment management at a large discount to traditional wealth management; it improves accessibility with a fully managed portfolio available with a minimum investment of £10,000 and total costs of less than 1% p.a.

DIY Investor and sister site Muckle exist to improve levels of financial literacy; informing experienced investors and engaging those new to investing.

At one level the results of the YouGov survey are extremely troubling, yet by identifying the problem we are able to address it, and improved financial education is key to ensuring that the current shortfall does not turn into a crisis.

With uncertain levels of future state provision, spiralling student debt, the rocketing cost of accommodation, the need for income in retirement and funding later life care, the magnitude of the challenge cannot possibly be underestimated.

With Cash ISA rates eclipsed by inflation, despite the fact that they may have believed they were doing the ‘right thing’ savers are currently getting poorer in real terms which may prove to be just the motivation required to get them to consider a long-term investment regime.

However daunting it may appear to those yet to engage, self-determination will be the key to financial emancipation, and improved levels of financial literacy will be the catalyst.

Whether you decide to take full control and ‘Do it Yourself’, work with an adviser – ‘Do it With me’, or instruct a company such as Scalable Capital to manage your investments on your behalf – ‘Do it For me’, there will be an option out there for everyone.

Whichever route you choose, there are common threads to achieving a successful outcome to an investment strategy; start early, invest for a long time, and keep costs to a minimum; even if the chance to start early has escaped you, you can only start from wherever you are, but as we say with a nodding apology to Nike – ‘Just Don’t do Nothing’

*Source: https://www.aviva.com/media/upload/Aviva_Mind_the_Gap_2016_Quantifying_the_pension_savings_gap_in_Europe_HJ9aexB.pdf

The YouGov survey was conducted in the UK and Germany in February 2017, with a sample size of more than 2,000 adults in each market. All figures, unless otherwise stated, are from YouGov Plc. Total sample size for the UK was 2,085 adults. Fieldwork was undertaken between 3rd – 6th February 2017. The survey was carried out online. The figures have been weighted and are representative of all UK adults (aged 18+).

Leave a Reply

You must be logged in to post a comment.