Nov

2020

Strategic Fixed Income: from bond glut to bond drought

DIY Investor

7 November 2020

Nicholas Ware, Portfolio Manager in the Strategic Fixed Income Team, explains why he believes the second half of 2020 will see lower net issuance in corporate bond markets following the dizzying volume of new bond issues in the first half.

Nicholas Ware, Portfolio Manager in the Strategic Fixed Income Team, explains why he believes the second half of 2020 will see lower net issuance in corporate bond markets following the dizzying volume of new bond issues in the first half.

Key takeaways:

- The second half of 2020 will likely see lower net corporate bond issuance due to bond buybacks and repayments as companies, having raised sufficient funds in the first half, will be more aggressive in managing their credit ratings and leverage levels in order to ensure they qualify for central bank‑backed bailouts in the future.

- We believe companies will be working hard to protect their investment grade ratings; and may even see high yield entities ahead of the next crisis trying to be upgraded to investment grade — similar to 2016, when the ECB’s corporate bond buying facility was launched.

- The steps that companies have taken so far to shore up their credit rating will not fully offset the impact of weaker earnings due to the crisis, but it should set them up nicely for 2021. In addition, lower issuance for the remainder of 2020, could help support the asset class.

Following US$1.2tn of corporate bond issuance since the start of 2020, which is up 95% versus 2019*, we are now making an argument for lower investment grade net issuance in the second half of the year, helped by bond buybacks and repayments.

We feel companies will be more aggressive in managing their credit ratings (ie, seeking to maintain or improve their current ratings) and leverage levels (ie, avoiding excessive borrowing), post the Covid‑19 pandemic, to ensure they qualify for central bank‑backed bailouts.

Value in being investment grade in the next downturn

The US Federal Reserve (Fed) has set up two Covid crisis facilities: the Primary Market Corporate Credit Facility (PMCCF) for new bond issues and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds, and which will be part of a toolbox for the next recession if needed.

The requirement to qualify for those facilities is that corporates needed to be rated at least BBB-/Baa3 by at least two major credit ratings agencies as of 22 March 2020.

Similarly, the European Central Bank (ECB) has been using its existing corporate sector purchase programme (CSPP) and a newly created pandemic emergency purchase programme (PEPP), which requires the corporate to be rated investment grade by at least one agency to qualify.

So, if you are a chief financial officer (CFO) of a company, you know that you are going to be much safer being ‘investment grade’ heading into the next downturn, where you will be able to access these tools.

We believe companies will be working hard to protect their investment grade ratings; we may even see high yield companies trying to be upgraded to investment grade in the next few years (also known as rising stars).

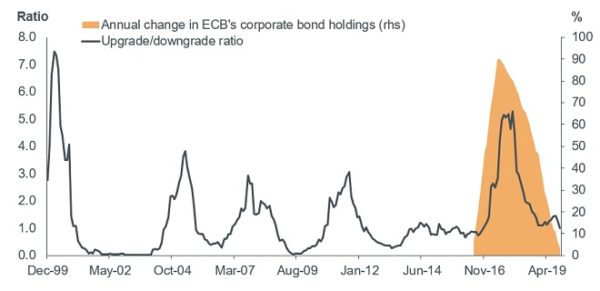

We saw this in Europe, in June 2016, when CSPP was launched and many companies realised that it was beneficial to be rated investment grade. Chart 1 shows the changing pattern in ratings that followed the ECB’s bond purchases.

Chart 1: ECB bond purchases and changes in ratings

Source: BofA Global Research, data from December 1999 to October 2019, as at July 2020

Larger companies are more likely to be diversified, have greater access to capital and have proven that they can adapt to crises. This is evident through the significant cuts that have been made to dividends, employees and capex in order to shore up credit rating positions.

Hence, we are in a sweet spot in the credit cycle and this is why we continue to remain constructive on corporate credit.

Investors catching up with the change in behaviour

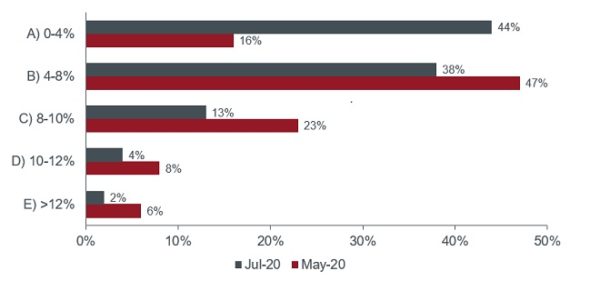

It looks like investors are now catching up with this change in behaviour. The investment bank, Bank of America, recently conducted an investor survey and found that clients’ expectations to see fallen angels (investment grade companies downgraded to sub-investment grade) over the next 12 months are now much lower than even a couple of months ago.

Chart 2: percentage of BBB rated companies expected to be downgraded to high yield

Source: BofA US Credit Investor Survey, as at 13 July 2020

Of course, there will be some fallen angels (investment grade bonds downgraded to sub-investment grade) but we believe that the story might be overhyped given the actions taken by many corporates and the support, both monetary and fiscal, from authorities.

Between March and May this year, companies raised sufficient funding for their operations. We now expect them to try and reduce leverage on their balance sheets and buy back bonds in the second half of the year and into next year.

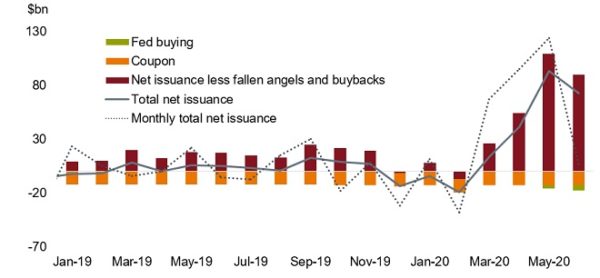

In addition, the Fed remains in the background, buying up bonds too. While the Fed has had a huge impact on sentiment, it has not needed to buy many bonds in the new issue market, as shown in chart 3.

The data, from BNP Paribas, shows that strong bond buybacks by US companies in June brought the total net issuance (dotted line) to a mere $6.5bn for the month, although gross issuance was north of $100bn — a real slowdown versus the period March-May.

Chart 3: US investment grade non‑financial issuance patterns

Source: BNP Paribas, Bloomberg, monthly data, as at 30 June 2020

Note: Coupon, net issuance less fallen angels and buybacks and total net issuance: 3‑months moving averages; net issuance data from February 2004 to June 2020; Fed buying: US Federal Reserve May and June 2020

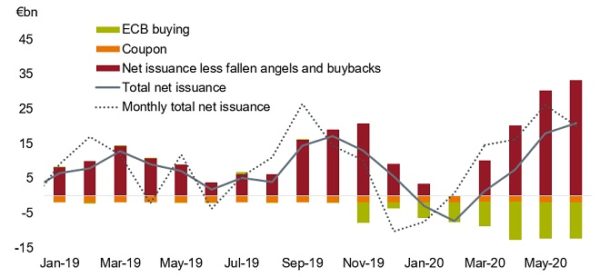

There was also robust issuance in the European investment grade market in the second quarter as companies focused on hoarding cash. Heading into the summer, we expect issuance to slow while a dominant ECB plays its part in buying corporate bonds at roughly €11bn per month.

Chart 4: European investment grade non‑financial issuance patterns

Source: BNP Paribas, Bloomberg, monthly data, as at 30 June 2020

Note: Coupon, net issuance less fallen angels and buybacks and total net issuance: 3‑months moving averages; net issuance data from February 2004 to June 2020.

Concluding thought

The fact that corporations have taken several steps, such as front-loading issuance, cutting investments and shareholder payouts, does not fully offset the impact from weaker earnings going forward (due to the twin shocks of COVID‑19 and the oil crisis), but it should set them up nicely for 2021.

We believe lower issuance for the remainder of 2020 will be an important story leading to corporate bonds remaining a well‑supported asset class.

*As at 19 June 2020

Notes:

Credit cycle: a recurring economic cycle, which refers to the phases of access to credit by borrowers; from periods where funds are relatively easily available to a contraction period when there is less credit available to borrowers.

Credit ratings: corporate borrowers or bonds are often rated by credit rating agencies. Investment grade: investment grade corporate bonds are issued by companies that are rated by credit rating agencies as being high quality. Sub-investment grade or high yield: a high yield bond is a bond with a lower credit rating than investment grade corporate bonds. The higher risk of not meeting their repayment obligations to investors means these bonds typically pay a higher yield than investment grade bonds.

Fiscal policy: a government policy relating to setting tax rates and spending levels. It is separate from monetary policy, which is typically set by a central bank.

Leverage: the level of borrowing or debt of a company. This is typically measured relative to its assets or earnings, so the higher the leverage, the more indebted a company.

Liquidity: the ability to buy or sell a particular security or asset in the market. Assets that can be easily traded in the market (without causing a major price move) are referred to as ‘liquid’.

Monetary policy: the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Commentary » Fixed income Commentary » Fixed income Latest » Henderson Partner Page » Mutual funds Commentary » Mutual funds Latest

Leave a Reply

You must be logged in to post a comment.