Jun

2021

So…what about inflation?

DIY Investor

26 June 2021

John Pattullo, Co-Head of Strategic Fixed  Income, shares his views on the most frequently asked question by clients these days: ‘what about inflation?’

Income, shares his views on the most frequently asked question by clients these days: ‘what about inflation?’

Key takeaways:

- There are lots of definitions of inflation: core/headline, cyclical/acyclical, wage/asset price, demand‑pull/cost‑push, and importantly, structural inflation. While the term is used rather loosely, an important aspect is often left out — the time horizon.

- Given the large demand shock experienced by economies during the shutdown, we expect low levels of both headline and core inflation going forward; though headline inflation should crater even more and is likely to be negative and more volatile because of the oil price crash.

- In the very short term, we expect deflation; in the medium term, we expect some cyclical reflation with price volatility. However, it is important not to confuse shorter‑term cyclical inflation with longer‑term structural factors, which could result from a possible and probable regime change.

Two crises (Covid‑19 and oil) within the existing global financial crisis! Is now really the time for persistent inflation?

The most frequently asked question that Jenna (Barnard) and I receive currently is: “So… what about inflation?”

We always find this a particularly vague question and I hope by highlighting some of the definitions and nuances, I can attempt to answer it properly in this article. I will also map out our shorter‑term cyclical thinking against longer‑term structural threats.

Last summer I penned “Do you remember the Great Financial Crisis? Ahh — you mean the one we are still in…”. I wrote it slightly in annoyance to the junior, and rather overconfident, investment bank salesperson who seemed to be of the opinion that the Great Financial Crisis (GFC) was over.

The article highlighted that most nations had accumulated much more debt than even before the GFC, that monetary policy used as a substitute to fiscal policy was broadly ineffective and hence, the malaise of low growth, low inflation and low bonds yields would continue to persist.

I said in the article that we expected even lower bond yields, given the Japanification of the Western world. Some investors ridiculed this view and remained heavily underweight bonds, further choosing to overweight alternative investments such as exotic/illiquid/esoteric credit products — the so‑called fool’s yield*.

I remember being invited to a ‘Finding yield in structural complexity’ conference, which I was wise enough not to attend! Unfortunately, much of this ‘fool’s yield’ has performed very poorly recently, which was of no surprise to us.

That article also cited one of our heroes, the economist, Richard Koo. In a book published in 2008, he made the point that the real solution to help the world to grow again was a wartime policy response; ie, using substantial fiscal policy as a complement to loose monetary policy.

Pre‑coronavirus, such a response was not politically justified but, fortunately, it is now, and various authorities around the globe have done a great job of bridge‑financing individual and corporate balance sheets.

We did not anticipate the Covid‑19 crisis, and the lurch down in sovereign bonds and short‑term interest rates; but we were not surprised by the direction of travel, rather just the timing.

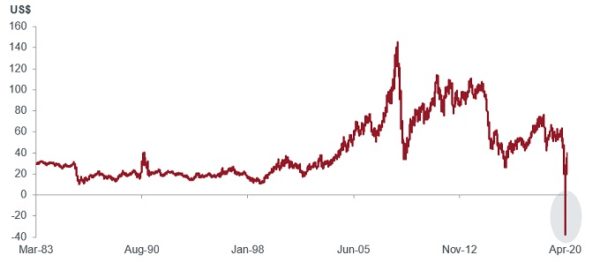

Meanwhile, so many people seem to forget that we are in the midst of an oil crisis, which kicked off in late February just before the Covid‑19 pandemic broke out in Europe. The oil shock alone is a massive deflationary force as well as being destabilising — akin to the events in 2016. Who could have ever imagined negative oil prices?

Chart 1: US oil’s historic fall into negative territory

Source: Bloomberg, generic West Texas Intermediate (WTI) futures price, daily data, year to date to 18 June 2020.

Note: the oil price turned negative briefly on 20 April 2020.

So, where does this leave inflation?

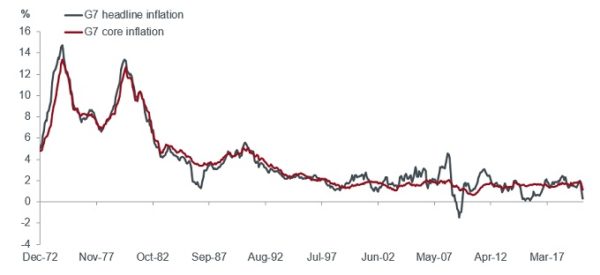

There are of course lots of definitions of inflation and people use the term rather loosely. We have core and headline, cyclical and acyclical, wage and asset price, demand‑pull and cost‑push inflation, and so on. More importantly we have structural inflation. Also, what time horizon are we talking about?

Chart 2 shows the decline in the most commonly watched data — headline inflation and core (ex‑volatile food and energy items) inflation — in the developed economies over the last few decades.

Chart 2: G7 inflation

Source: Bloomberg, G7 countries (Canada, France, Germany, Italy, Japan, the UK and the US), headline and core inflation, monthly data, as at 31 May 2020.

…in the very short term (the next six months or so)…

Given the large demand shock experienced by economies during the shutdown, we expect low levels of both headline and core inflation going forward; though headline inflation should crater even more and is likely to be negative and more volatile because of the oil price crash.

Remember that inflation indices are 12‑month rolling averages; the negative and low oil price months will remain in the averages for many months until eventually they drop out.

Thus, base effects matter a great deal. Demand has fallen off a cliff, while supply has adjusted with a lag. It is perfectly reasonable to argue the opposite as we open up again and supply is constrained in the short term.

…in the short to medium term (nine months to three years)…

Given, that supply chains and inventory builds/drawdowns are all over the place, we expect bottlenecks in food and various commodity markets. So, if you like, the rate of change of consumption will outpace the rate of change in industrial production.

Janus Henderson’s Economic Adviser, Simon Ward, is bullish on ‘commodities and housing’ inflation, especially over the next few years. We tend to agree. The pandemic has highlighted the desire to reshore certain industries for obvious reasons.

Such deglobalisation will mean things will cost more — cost‑push inflation if you like. Most of the historic inflation in the US in recent years has been in non‑discretionary items such as rent costs (called shelter costs), healthcare and education, while most goods inflation is actually negative or very low.

Another type of short‑term inflation is imported cost inflation, which the UK experienced rather nastily in 2011 when the consumer price index (CPI) inflation rose to 5.2% in September 2011, due to the lagged effects of sterling falling materially post the GFC.

Sensibly, the Bank of England looked through this imported inflation, which was a temporary phenomenon, and fortunately did not raise interest rates in response. That would have been disastrous for the economy at the time.

… and in the longer term (three years +)?

In the very short term, we expect deflation; in the medium term, we expect some cyclical reflation with price volatility (in various guises) subject to the local constraints of the respective countries, which could well be stagflationary.

However, it is important not to confuse shorter‑term cyclical inflation with longer‑term structural factors, which could result from a possible and probable regime change.

We feel there is a pretty good case to be made for a longer‑term paradigm shift. Many, often elderly commentators (who had experienced the inflation of the 70s and 80s), forecasted inflation as a result of the money printing by the authorities post the GFC; and were fantastically wrong.

We were also wrong with a short duration bias in 2010‑11, agreeing with the consensus view, which would have necessitated hikes in interest rates.

Then we read Richard Koo’s book and have been long duration ever since — up until the recent pandemic crisis hit the markets — as we saw a world trapped in a low interest rate environment.

Back then, most of the money printing was either trapped in the banking system or found its way into financial markets, resulting in asset price inflation but not Main Street inflation. This time, it is a little different, so we remain open‑minded.

Nowadays, banks are well capitalised, and willing and able to lend money (much of it underwritten by the government, or should I say taxpayers!). There has also been fiscal and monetary stimulus on an unprecedented scale. Further, there does seem to be genuine demand for corporations to borrow money, in both Europe and America.

This is where it gets quite nuanced.

The explosion of corporate borrowing in America is to build a safety net/cash buffer. Some of the biggest and safest companies are raising longer‑term ‘bond’ money to repay shorter‑term revolving credit lines. More precarious companies are simply terming out short‑term debt.

Time will tell what happens to the excess cash raised. Optimists say the money will tide the companies over and may get invested. It may be returned to bondholders or it may even be used to buy back shares; it all depends on confidence and the economic outlook, of course. In the same way, will the US government’s gifted cheques be used to pay down debt, consumed or invested? That is a tougher argument.

Too much personal savings are a leakage on the economy

Again, Koo economics suggests this surplus should be captured and spent by the government via fiscal policy. Along these lines, there is much discussion on the ‘velocity’ of circulation (how quickly money turns over in an economy in a given period of time) in the MV=PT** monetary equation.

In theory, the amount of money in the economy, multiplied by how fast it turns over, is a proxy for aggregate demand. Simon Ward believes that velocity has fallen, for a number of structural reasons.

He argues that the trend decline in broad money velocity reflects a rising wealth to income ratio; ie, money has outpaced nominal gross domestic product (GDP) not because of ‘hoarding’ but because of an additional demand for money due to rising wealth.

The current money supply explosion is massive in a historical context. Simon feels that the velocity decline is unlikely to fall enough to offset the money supply expansion, and hence this could be inflationary. Again, if this is correct, the longevity of this impulse is up for debate.

Simon’s longer‑term growth and inflation argument is further supported by some of his ‘economic cycle’ work (in relation to the inventory, capital expenditure (capex) and most pertinently, the housing cycle). Other commentators dismiss the potential for excess demand out of hand. You could argue that it is hard to have excess demand (demand‑pull inflation) with a massive output gap. It is hard to find businesses which are short of capacity, apart from the short‑term bottlenecks discussed earlier.

Remaining pragmatic and open‑minded

Thus, on this point — inflation in the longer term — we remain open‑minded or at least try to be! We have remained very sceptical of other mainstream economic folklore such as the Phillips curve for years now.

We do have serious concerns about the now apparent and broadly accepted monetisation of fiscal deficits and an emerging Modern Monetary Theory (MMT — or even the Magic Money Tree!) paradigm shift and yield curve control (YCC).

Complete currency debasement (lowering the value of the currency) and helicopter money for all could certainly bring excess demand inflation (by closing the output gap).

Moreover, this could change inflation expectations as well, especially as the credibility of central banks wears thin. We have written on this before. We expect yet more financial repression with negative real yields all over the developed world. Post‑World War II, financial repression was very common in trying to shrink government deficits relative to GDP.

The gold bugs are loving this debasement of money. Why? Gold correlates well with falling real yields. Also, in a relative sense, gold is quite ‘yieldy’ as we have negative real yields in most countries; and it is in short supply, unlike paper money.

This is a nastier environment for sovereign bond investing, which is why we are now almost fully invested in quality corporate bonds. Beware cyclical inflation pops and price volatility for now but do not confuse that with a paradigm shift, not yet anyway!

Notes

*Dan Rasmussen, Portfolio Manager, US-based Verdad Advisor. ‘Fool’s yield and the wild west of private credit’ interview on Real Vision, 22 January 2020.

**MV=PT: Fisher Equation, Quantity Theory of Money. M = Money supply, V= Velocity of circulation, P= Price level and T = Transactions.

Glossary

Broad money: money in any form including bank or other deposits, as well as notes and coins

Deflation: a decrease in the price of goods and services across the economy, usually indicating that the economy is weakening. The opposite of inflation.

Financial repression: in simple terms, using regulations and policies to force down interest rates below the rate of inflation; also known as a stealth tax that rewards debtors but punishes savers.

Fiscal policy: a government policy relating to setting tax rates and spending levels. It is separate from monetary policy, which is typically set by a central bank.

Gross domestic product: a measure of the size of the economy.

Main Street: a reference to small businesses, locally owned banks, the working and middle classes and the economy.

Modern Monetary Theory (MMT): an unorthodox approach to economic management, which in simple terms argues that countries that issue their own currencies can ‘never run out of money’ the way people or businesses can.

Monetisation of fiscal deficits: in simple terms, central banks buying government bonds by printing money to finance it.

Output gap: the amount by which the actual output of an economy falls short of its potential output due to underemployment of labour and capital.

Reshoring: transferring business operations that were moved overseas back to the home country.

Stagflation: a relatively rare situation where rising inflation coincides with anaemic economic growth.

Structural inflation: a permanent change in inflation/inflation expectations.

Yield curve control (YCC): where a central bank targets a longer-term rate, pledging to buy enough long-term bonds to keep the rate from rising above its target, hoping to stimulate the economy.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Click to visit:

Commentary » Equities Commentary » Exchange traded products Commentary » Fixed income Commentary » Henderson Partner Page » Investment trusts Commentary » Investment trusts Latest » Mutual funds Commentary » Mutual funds Latest

Leave a Reply

You must be logged in to post a comment.