Dec

2021

Scrap – the greener side of steel

DIY Investor

15 December 2021

Increased scrap use can help reduce emissions

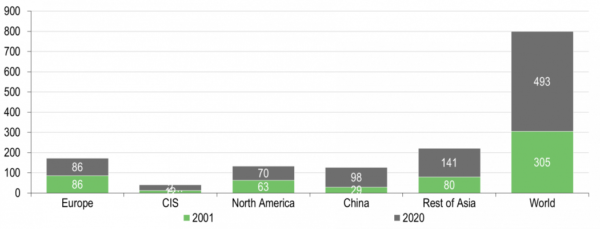

![]() Steel making is an energy (mainly from coal and electricity) intensive industry. For each ton of carbon steel produced, 1.83t of CO2 is emitted. Annually, it contributes 5% to C02 global emissions and the only way to reduce these is to improve steel-making efficiencies, maximize the use of scrap and use or develop new technology.

Steel making is an energy (mainly from coal and electricity) intensive industry. For each ton of carbon steel produced, 1.83t of CO2 is emitted. Annually, it contributes 5% to C02 global emissions and the only way to reduce these is to improve steel-making efficiencies, maximize the use of scrap and use or develop new technology.

Globally, coal contributes more than 40% of fossil fuel emissions, followed by oil (35%) and the balance from gas. The main industrial sectors of release are electricity and heat production (50%), transport (20%), and the manufacturing and construction industries (20%). Roughly 50% of all emissions worldwide stems from five countries, namely China (25%), the United States (12%), India (6%), Russia (4%) and Japan (3%). (Source: United States Environmental Protection Agency.)

Simplistically, steel production is either based on iron ore, produced via blast furnace and an oxygen converter, or via an electric arc or electric induction process, based largely on scrap metal. The latter has a major advantage as it is a cleaner steel-making process, with estimated emission savings of 40% relative to the blast furnace process.

Increasing use of electric arc capacity will gradually reduce steel industry emissions. Meanwhile, measures to encourage the use of scrap by way of export and pricing controls by a number of producing countries will have the effect of securing steel scrap reservoirs in domestic markets. This should help keep scrap costs at economic levels, making its future use for lower emission steel production more attractive.

![]()

Leave a Reply

You must be logged in to post a comment.