Apr

2024

Schroder UK Mid Cap Fund plc: UK equities – what’s the catalyst?

DIY Investor

16 April 2024

Mid caps particularly well poised for a UK renaissance – Jean Roche, portfolio manager

After several years of disappointing relative performance, it is now widely acknowledged that the UK represents one of the cheapest regional equity markets in the world, with mid cap stocks looking especially attractive. This ought to bode well for future long-term returns, but the roots of the UK’s under-performance can be traced back to before Brexit, so when can we expect things to change? Here, we examine whether there is anything on the horizon that has the potential to change the UK stock market’s relative fortunes, and find several reasons for positivity, particularly for UK mid caps.

‘the UK represents one of the cheapest regional equity markets in the world’

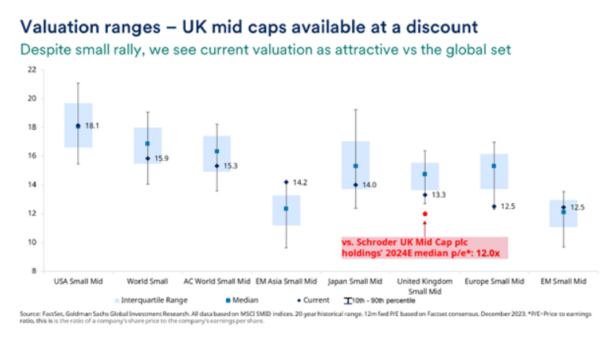

According to data from Morgan Stanley, UK equities currently trade at a near 40% discount to their global peers, which is close to the steepest valuation gap observed since the mid-1970s. Meanwhile, within the UK stock market, mid cap stocks look remarkably undervalued, with the FTSE 250 now trading at a small but persistent discount to the FTSE 100, as well as to most other small and mid cap markets around the world.

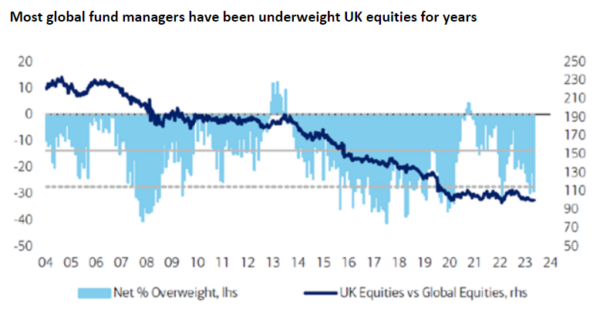

Despite the extent of this under-valuation, UK equities remain unloved. As the chart below demonstrates, global fund managers have been consistently underweight UK equities since July 2021, and indeed, they have tended to be significantly underweight the domestic market for most of the last decade. This has coincided with a period of under-performance from the UK stock market, particularly in the years from 2014 to 2020, as illustrated by the dark blue line.

Source: BofA Merrill Lynch Global Fund Manager Survey, January 2024. Past performance is not a guide to future performance and may not be repeated.

Inflation benefit

Fortunately, there are reasons to believe that this may now be in the process of changing, particularly as far as UK small and mid-sized companies are concerned. Global equity markets performed well in the fourth quarter of 2023, with domestically-focused UK mid-caps outperforming.

‘Given the extent of undervaluation that we see, this could be the start of a much longer-term trend’

This is a part of the market that is particularly sensitive to inflation and interest rates, so it seems likely that the growing belief in markets that UK and US interest rates have now peaked, has played a role in the recent resurgence of interest in UK mid cap stocks. Jean Roche, portfolio manager of the Schroder UK Mid Cap Fund plc, explains:

“UK mid caps are an inflation-sensitive part of the market, so the recent decline in consumer price inflation data both here in the UK and in the US, is seen as a positive for our sector. Most economists now expect interest rates to fall, with the average forecast now for a 1% rate cut this year, followed by another 1% in 2025. This appears to have prompted renewed interest in UK mid caps in recent weeks but, given the extent of undervaluation that we see, this could be the start of a much longer-term trend.”

Bid premium

Jean also points to the prospect of continued merger & acquisition (M&A) activity as a reason for optimism. M&A activity has been elevated in recent years, as foreign buyers and private equity have been keen to take advantage of the UK’s depressed valuations. Indeed, in 2023, UK M&A transactions carried an average price premium of 51%, which reflects how under-valued UK equities have become.

Due to their size, small and mid-sized companies are much more likely to become acquisition targets than large companies. Despite this, the number of bids being received by UK mid cap companies was surprisingly low last year. This may signal pent-up demand, which could point to greater M&A activity among UK mid caps over the next couple of years.

Shrinking market

UK businesses are also showing tremendous capital discipline in buying back their own shares to take advantage of their current undervaluation. Jean is positive on share buybacks, as long as they are done at the right price.

“Of all the uses of cash flow, share buybacks are among the most attractive if they are conducted when a company’s share price is depressed. We are delighted to see more share buybacks among selected UK mid caps because it demonstrates sensible capital allocation decision-making in the current environment.

‘this could be a catalyst for improved share price performance because share buybacks mean more demand for UK equities, along with a diminishing supply’

Within the Schroder UK Mid Cap portfolio, financial holdings Man Group and Paragon have both been actively buying back their shares recently and generating high returns from doing so. Meanwhile, industrial business Bodycote was intending to acquire another company but has subsequently decided to buy back its own shares instead, because the return it can generate from doing so is even greater. This demonstrates excellent capital discipline, which we believe is reflected across much of the portfolio.”

Nearly a quarter of UK mid cap stocks bought back at least 1% of their outstanding shares in 2023, which is significantly higher than the historical average. In its own right this could be a catalyst for improved share price performance because share buybacks mean more demand for UK equities, along with a diminishing supply. In simple economic terms, increased demand and lower supply tends to be reflected in higher prices. Share buybacks in aggregate could, therefore, represent a very significant buyer of UK equities, which the chart above suggests has been absent for many years.

Beyond the catalyst

Investors often wish to see the presence of a catalyst before taking advantage of an evident valuation opportunity, but this can mean missing out on the early gains. Catalysts are, by their very nature, short-term market factors, but it pays to take a long-term view when it comes to equity investing. Ultimately, financial markets have an uncanny habit of becoming more rational in the end, and the presence of shorter-term valuation anomalies will always present opportunities for disciplined active investors to try to capture.

In the meantime, Jean is keen to point out that shareholders in Schroder UK Mid Cap Fund are being well-rewarded for their patience.

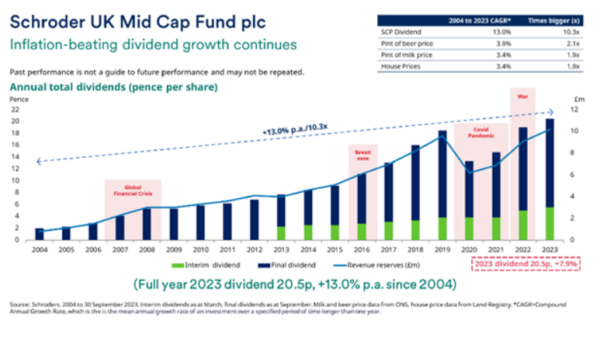

“The fund aims to deliver an attractive total return to shareholders, and we’re confident that it is well-positioned to do that. An important element of that total return comes from the income that flows from the companies in the portfolio. The current yield is 3.5% and the level of dividend growth has been exceptional too. We’ve delivered 13% annualised growth in the dividend since 2004.

This means shareholders are being paid to wait for UK equities to enjoy their moment in the sun again. We believe this will happen in the end, but the timing is, as ever, uncertain. Longer-term, if we continue to focus on identifying high quality, financially robust, well-managed businesses with solid growth prospects, we believe the market will ultimately value them more appropriately. Investors have historically been well-rewarded by this approach, despite the UK being increasingly unloved over the last ten years. This leaves us feeling very optimistic about what we can deliver in the years ahead, with a more favourable valuation tailwind behind us.”

Click here to find out more about the Schroder UK Mid Cap Fund plc >

Schroder UK Mid Cap Fund plc risk considerations:

The trust Invests in smaller companies that may be less liquid than larger companies and price swings may therefore be greater than investment trusts that invest in larger companies.

The trust will invest solely in the companies of one country or region. This can carry more risk than investments spread over a number of countries or regions.

As a result of the fees and finance costs being charged partially to capital, the distributable income of the trust may be higher but there is the potential that performance or capital value may be eroded.

The trust may borrow money to invest in further investments, this is known as gearing. Gearing will increase returns if the value of the investments purchased increase in value by more than the cost of borrowing, or reduce returns if they fail to do so.

FTSE third party data disclaimer: FTSE International Limited (‘FTSE’) © FTSE (2024). FTSE®’ is a trade mark of London Stock Exchange Plc and The Financial Times Limited and is used by FTSE International Limited under licence. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

For help in understanding any terms used, please visit address https://www.schroders.com/en/insights/invest-iq/investiq/education-hub/glossary/

We recommend you seek financial advice from an Independent Adviser before making an investment decision. If you don’t already have an Adviser, you can find one at www.unbiased.co.uk or www.vouchedfor.co.uk. Before investing in an Investment Trust, refer to the prospectus, the latest Key Information Document (KID) and Key Features Document (KFD) at www.schroders.co.uk/investor or on request.

![]()

Schroder UK Mid Cap Fund plc update

UK Mid-caps are positioned in a sweet spot for innovation, disruption and growth. This is why the UK Mid Cap index has beaten most other developed market indices over the long term.

The FTSE 250 is an incubator for growth in that it is home to many businesses that are riding the wave of long-term structural growth trends. Although they have proven products and services, they can have ahead of them a much longer and steeper growth trajectory than their large cap counterparts.

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority

Commentary » Equities » Equities Latest » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.