Apr

2021

Powerful factors coalescing for a rebound in U.S. travel and leisure

DIY Investor

4 April 2021

Portfolio Manager Jeremiah Buckley and Assistant Portfolio Manager David Chung discuss the strong recovery potential for travel and leisure industries as COVID restrictions ease.

Key Takeaways

- Travel and leisure industries have been hampered by social restrictions, perhaps more than any other segment of the economy, during the COVID pandemic.

- However, a confluence of factors ‒ broader rollout of vaccines, significant pent-up demand, robust consumer savings and extensive monetary and fiscal stimulus ‒ are beginning to foster green shoots of activity.

- Although it is impossible to forecast the exact timing, looking to the second half of 2021 and beyond, select stocks within these industries may benefit as the U.S. economy reopens and pent-up demand is unlocked.

Travel and leisure have perhaps been the two industries most severely impacted by social restrictions brought on by the COVID pandemic.

However, there are powerful factors coalescing that point to a strong economic rebound in the U.S. in 2021: the broader rollout of vaccines, significant pent-up demand, strong consumer balance sheets and extensive monetary and fiscal stimulus.

These forces are beginning to foster green shoots of activity ‒ particularly in these beleaguered areas ‒ and could lead to a considerable rebound once the economy can fully reopen.

A health solution to the pandemic is driving optimism

Vaccination rollouts have led to a marked drop in the number of COVID cases and hospitalizations, fueling optimism for a full reopening of the economy.

At the time of writing, nearly 100 million vaccine shots had been administered in the U.S. and nearly 20% of the population had received at least one dose.1

Some states have begun to lift social restrictions and mask mandates (e.g., Texas, South Dakota, Montana, Mississippi and Iowa), citing the drop in infections and increased vaccinations.

In other states, restrictions are being eased, such as allowing increased capacity for social gatherings in restaurants, theaters, casinos and sports and entertainment venues, foreshadowing a full reopening of the economy.

However, significant concerns remain around highly contagious variants of the virus and past instances where the easing of restrictions has led to spikes in cases.

Unlocking pent-up demand

Consequently, we are starting to see green shoots of activity in travel ‒ particularly within leisure ‒ and indications of significant pent-up demand that will be released as restrictions ease and markets reopen to tourism.

Many consumers were forced to skip vacations entirely in 2020 and are now anxious to travel in the very near future: 34% of Americans plan to travel out of town this spring and another 35% plan to do so this summer2, while 76% are planning destination wish lists for future travel.3

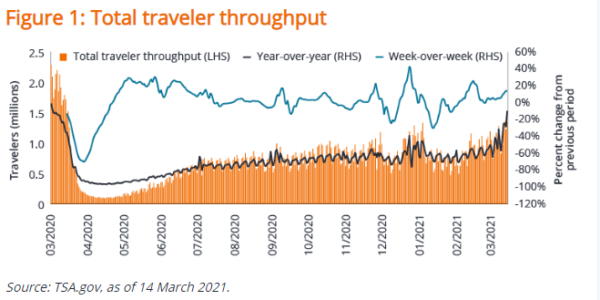

Although still significantly below pre-pandemic levels, total traveler throughput at U.S. airports has increased to the highest levels since the pandemic began as shown in Figure 1.

A major hotel chain expects essentially all rooms within their network to be reopened by mid-2021, and occupancy over the Presidents’ Day holiday in February 2021 was the highest for a long weekend since the beginning of the pandemic.

While leisure travel and bookings within driving distance continue to significantly outpace business and longer-distance travel, there are expectations that business and group demand (trade conferences, for example) will recover in the second half of 2021 and into 2022, as some companies view this travel and these events as essential to their businesses.

That said, the majority of hotel reservations are still being made within a week of travel and international trips remain heavily restricted. This lack of visibility limits trend forecasts going forward but does suggest that companies more exposed to regional travel could benefit initially, and potentially grow market share during this period.

The re-emergence of travel demand also has the potential to positively impact industries outside of obvious beneficiaries like airlines and hotels.

In March, a major U.S. ride-share provider reported its highest week of rides and year-over-year growth in ride-share volume for the first time since the pandemic began.

At the same time, while electronic payment networks have seen cross-border volumes significantly hurt by international travel restrictions, the pandemic has accelerated the adoption of e-payments, and these companies may be poised to benefit from an uptick in travel transactions once restrictions are lifted.

Healthy consumer balance sheets can provide fuel

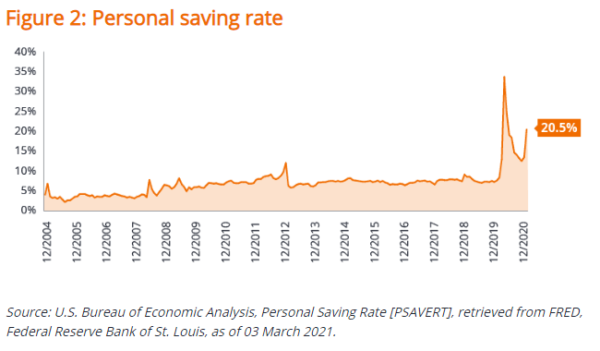

Although millions still remain unemployed and affected by the fallout from the virus, in general, the U.S. consumer appears to be in a healthy position to help drive a recovery, bolstered by surplus savings (Figure 2) and asset growth from both the stock market recovery and strong home values.

Year-over-year, the personal saving rate in the U.S. has nearly tripled to 20.5% as of January 2021 versus 7.6% as of January 2020, driven by a tremendous amount of fiscal stimulus with the likelihood to go even higher with an additional US$1.9 trillion of stimulus recently passed.

Personal saving as of January 2021 amounted to US$3.9 trillion, up from US$2.3 trillion in December, in large part due to the Coronavirus Response and Relief Supplemental Appropriations (CRRSA) Act, which was passed in late December.

Consumers can decide to spend savings on goods and services or use them in other ways, such as paying down debt or making investments.

Ultimately, these decisions will play a significant role in the trajectory of the economic recovery, and early indications show that consumers’ propensity to save during 2020 is beginning to ease.

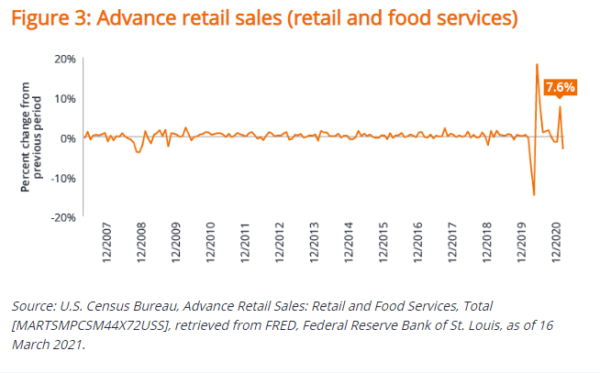

Retail sales are picking up, as depicted in Figure 3 ‒ advance retail sales for January grew 7.6%, with a larger percentage of spending being directed to discretionary categories. While preliminary data for February was weaker in comparison, sales remain elevated versus 2020 and we expect consumer spending to trend higher as the recovery continues

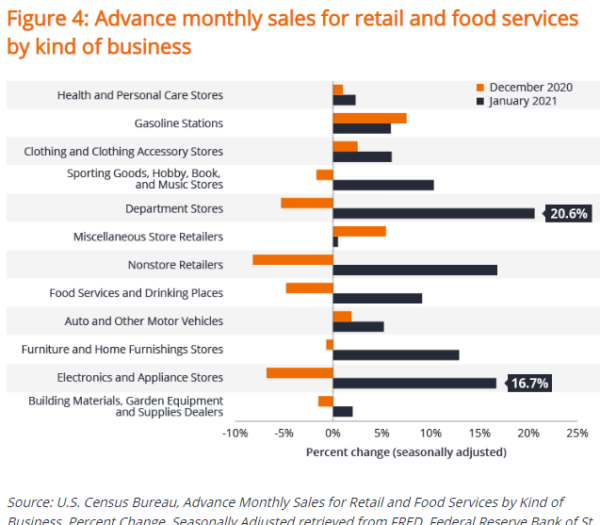

For instance, in January, retail sales at Electronics and Appliance Stores as well as Department Stores increased by 16.7% and 20.6%, respectively (Figure 4). If this trend continues, the amount of cash in savings could spur significant growth, as personal consumption represents over two-thirds of U.S. gross domestic product (GDP).

Growth drivers in the short and long term

Throughout the pandemic, we have seen investment themes related to widespread digitization galvanized. We think that a broad economic recovery can only serve to bolster these long-term trends.

These include the shift to e-commerce, increased adoption of digital payments, a transition to the cloud and Software as a Service for remote work, schooling and entertainment and increased health care innovation across pharmaceuticals, medical devices, patient personalization and diagnostics capabilities.

While we have seen a recent uptick in inflation expectations and interest rates, we also continue to believe that the backdrop for equities in general remains positive, helped by ongoing fiscal stimulus and accommodative monetary policy.

This backdrop combined with an improving health situation, significant pent-up demand and a strong consumer creates growth potential for certain companies in the leisure and travel industries.

That said, it remains extremely important to be selective when analyzing these industries, as some stocks’ valuations are higher than pre-pandemic levels despite materially worse balance sheets.

In some cases, companies have also diluted shareholders by issuing additional equity. Businesses, particularly in the travel and leisure industries, that can benefit from a recovery and have strong balance sheets could be well placed for a rebound as the economy reopens and returns to health.

1 Centers for Disease Control and Prevention, 10 March 2021.

2 Survey conducted online within the United States by The Harris Poll on behalf of Ad Age during 23-25 February 2021, among 2,032 U.S. adults ages 18 and older.

3 American Express Travel: 2021 Global Travel Trends Report.

Click to visit:

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Commentary » investment trust commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.