Jan

2025

Outlook 2025: Fixed income

DIY Investor

5 January 2025

Our fixed income experts examine the outlook for bonds, credit, and emerging market debt in 2025 and give insights into attractive income opportunities enhancing portfolio resilience through diversification – by Julien Houdain, Lisa Hornby and Abdallah Guezour

Global outlook

Julien Houdain, Head of Global Unconstrained Fixed Income & Lisa Hornby, Head of US Fixed Income

As we step into 2025, the calendar will change, but the driving forces behind the markets will stay the same. The evolution of economic fundamentals, and the impact of policy changes on them, will continue to be crucial.

Without a doubt, the changes implemented by the incoming US administration will clearly have a major impact on markets, but it is also important to note that fiscal plans in Europe, UK, and China will play a big part in shaping the overall economic cycle and the strategies of central banks.

These factors will likely create a favorable environment for fixed income, which stands to benefit from both broader economic trends and the high starting point in yields. Fixed income now earns its place in portfolios not only for its attractive income potential but also due to its scope for capital appreciation and its ability to serve as a diversifying asset relative to more cyclical segments of the market.

First, let’s pause and take a look at the US economy going into this year’s Presidential election. Growth was strong, inflation was improving (i.e. falling), and the labour market was close to balanced. The economy was back to equilibrium, and the much-discussed soft landing, a scenario where economic growth slows but does not contract and inflation pressures ease, was being delivered. The key question for 2025 is: can that momentum be maintained?

There’s a high level of uncertainty about policy as we approach 2025. The key issues on the US political agenda, including stricter immigration controls, more relaxed fiscal policy, fewer regulations on businesses, and tariffs on international goods, suggest a growing risk.

These factors may halt any improvement in the core inflation figures and could cause the US Federal Reserve (Fed) to cease easing monetary policy earlier than expected. In other words, we see a no-landing risk rising, a scenario in which inflation remains sticky and interest rates may be required to be kept higher for longer, though it’s not our base case.

The likely impact of Trump’s administration on economic growth is less clear cut. Firstly, as mentioned, growth was already very good. Even though it has the potential to get better, it is worth remembering that we’re starting from a high base already. Measures such as reducing regulation and enhancing fiscal impact can foster growth. These measures include making smarter investments in key areas like infrastructure, education, and healthcare to stimulate economic growth, create jobs, and ensure that public funds yield the best possible benefits for citizens. However, stricter immigration policies resulting in fewer available workers or significant disturbances to global trade due to higher tariffs could harm growth instead.

The pace, scale and sequencing of these different policies will play a critical role in steering the direction of the markets.

Though the potential growth and inflationary impetus of policies of the US government have led us to increase our no-landing risks, valuations in bonds have improved to offer more cushion against these.

We’re likely to start the year with 10-year US Treasury nominal yields above 4%, and real yields (net of inflation) above 2%, an attractive level of income we haven’t seen since the 2008 financial crisis.

CHART 1: Policy rates and 10-year yields are realigning, removing the discentive of owning bonds

Moreover, with policy rates also coming down, the negative carry (where the yield on the bond is below the funding cost of owning that bond position), that has been such a headwind to bond ownership over the past few years has disappeared for all but the shortest maturities.

Furthermore, at lower inflation levels, the diversification benefit of bonds increases, providing a more efficient hedge against weakness in cyclical assets. Bonds also look cheap versus alternative assets, with current yields higher than that of the expected earnings yield on the S&P500.

With these dynamics, bonds can serve a dual purpose in a portfolio: they can provide a source of income and build resilience in a diversified portfolio.

CHART 2: Fixed income yields are attractive versus equities

In other parts of the world, the worsening trade environment will amplify existing weakness in the industrial cycles in both China and Europe. We believe more policy support is needed to offset this, particularly if we see further signs of slowdown within the service sector. The less fiscal policy does, the more monetary support will be needed.

Thus far the policy response has been muted in both regions, but the upcoming German general election could be a change for a significant reassessment of the role of fiscal policy in Europe. It remains to be seen which path will be chosen.

At the same time, the UK has seen its fair share of change when it comes to government policy, most notably with Labour Party’s much anticipated Budget. The unexpected positive fiscal impulse complicates matters for the Bank of England, pushing back the date when we might expect to see inflation return sustainably to target. That said, we believe market valuations largely reflect this impact on inflation with rate cut bets being scaled back significantly recently. This repricing makes gilts attractive, despite the macro landscape remaining volatile.

This disparity in fiscal paths creates relative value opportunities in bonds, currencies and asset allocation. Being flexible and active in how we manage these investments will be key in seizing the excess returns these opportunities afford.

Cautious on credit, but finding value in securitized assets

A starting point of reasonable valuations, strong growth and central bank easing has made a happy cocktail in 2024 for cyclical assets, such as corporate bonds. Returns have been good, especially in higher-yielding areas.

In 2024, we’ve seen credit spreads—essentially the difference in yield between safe investments and those with higher risk—narrowing. Many segments of the market, including US investment grade and high yield corporates, now trade at narrower spreads than at any time since the pandemic. This trend suggests that investors are becoming more confident and willing to invest in higher-risk assets. This rally in spreads has been driven by a combination of robust economic growth, strong fixed income demand and expectations for the continuation of a supportive macroeconomic backdrop.

We expect credit fundamentals to remain robust in 2025. This, combined with elevated all-in yields and steeper yield curves (yields curve steepens when the difference between long-term and short-term interest rates is widening) should continue to attract inflows into credit.

Valuations will likely be supported, though room for further compression is more limited. In other words, while credit spreads may remain expensive, there is limited scope for them to become more expensive. We are therefore more cautious on these assets in multi-sector portfolios and have been focused on shorter-duration corporate bonds when they provide good income with limited spread duration risk (that is, limited sensitivity to changes in credit spreads).

Across the various industry sectors, we prefer banks as their valuations, in our view, have been more compelling than industrials, capital positions remain strong and steeper yield curves should improve bank net interest margins.

Better opportunities exist in securitized assets such as agency mortgage-backed securities. Agency mortgage-backed securities are issued by government-sponsored enterprises and are backed by a pool of mortgages. Like investment grade corporate bonds these high-quality assets still provide a good income stream, but with historically attractive valuations. Demand for this sector is also likely to increase given a less stringent regulatory environment in the US, allowing US banks to purchase these securities in their asset portfolios.

In addition, as the Fed reduces interest rates, we would expect some of the record US$7 trillion in US money market account balances to find its way into this pocket of the fixed income universe. We believe these types of assets have greater potential for capital appreciation and pose less idiosyncratic credit risk. As such, they remain our most favoured choice within asset allocation.

CHART 3: Agency mortgage-backed securities valuations are more attractive than investment grade credit

Lastly, we favour embedding a degree of liquidity. With valuations in most credit sectors at the tighter end of history and policy uncertainty quite high, it is very likely that periods of volatility will provide a good opportunity to deploy capital at less expensive levels. We are embedding that liquidity in various ways, such as through short-dated, high-quality asset backed securities, short-dated corporates, and US Treasury securities.

Emerging Market Debt

Abdallah Guezour, Head of Emerging Market Debt and Commodities

In 2024, emerging market debt (EMD) displayed relative resilience despite facing pressures from rising developed market government bond yields, ongoing geopolitical instabilities, uncertainties surrounding the US elections, and concerns about China’s growth.

A significant divergence in performance emerged between hard currency (debt denominated in a currency widely seen as stable, like the U.S. dollar) and local debt (debt denominated in the issuer’s own local currency). Hard currency debt, both sovereign and corporate, delivered reasonably attractive total returns. This was thanks to the high income generated by high yield issuers. These are issuers that generally have a lower credit rating, implying a higher risk of default, compared to investment-grade bonds.

In contrast, local debt, which outperformed in 2023, went through a significant correction due to weak currencies and rising government bond yields, particularly in Brazil and Mexico, where fiscal policy concerns have impacted investor confidence. However, with international investors underinvested in local debt markets, these fears may be somewhat exaggerated and already reflected in the lower valuations of local government bonds.

Optimism amid uncertainty

As we look towards 2025, despite ongoing global uncertainties and specific challenges in some countries, the trend where emerging market (EM) sovereign and corporate bond spreads become tighter seems set to hold. This means that the difference between the yields (or interest rates) on these bonds and those of safer investments, like developed market bonds, is decreasing, indicating growing investor confidence in EMD.

This optimism is largely due to encouraging signs in EM growth and the solid financial health of many EM issuers. Additionally, the rise in foreign exchange reserves in emerging markets, highlighted in chart 4, underscores the positive impact of the macro-economic adjustments made in recent years.

CHART 4: Annual growth of foreign exchange reserves (% y/y)

Even though these improvements have already been reflected in the current historically tight levels of EM investment grade spreads, there are still attractive pockets of value to be found in the high yield sector. Countries such as Argentina, Egypt, Nigeria, Ivory Coast, Senegal, Sri Lanka and Pakistan are examples of sovereigns that still offer appealing sovereign spreads while continuing their good progress on macro-economic adjustments following recent crises.

Evaluating strengths, challenges, and opportunities in EM corporates

EM corporates are also entering 2025 from a strong position, having received more credit rating upgrades than downgrades for the first time in over a decade. This sector will likely be buoyed by expectations of a resilient US economy in 2025, accommodative international and domestic capital markets, and still-healthy corporate balance sheets, as credit metrics are broadly stronger than pre-COVID levels. As such, default rates are predicted to continue improving, dropping to a healthy 2.7% in 2025, lower than the current level of 3.6% and the long-term average of 4.4%.

Although macro conditions are expected to remain supportive in 2025, the incoming Trump administration in the US promises an uncertain investment and operating climate for EM corporates. Sector selection will be important. EM corporate sectors facing scrutiny from the new Trump administration include autos, electric vehicle (EV) battery producers, chipmakers, and Chinese technology companies.

On the flip side, depending on if and how tariffs are ultimately implemented, investment in nearshoring — that is, relocating business processes or services to a nearby country – could continue to benefit corporates in countries like Mexico and India. Ukrainian corporates could also benefit handsomely if a ceasefire with Russia is achieved.

EM local debt – preparing for currency risks and global trade developments

Lastly, following the 2024 re-pricing in EM local debt, this sector is starting to offer even more appealing re-entry opportunities. EM local rates look very attractive from a valuation standpoint as real yields (the annual return on an investment, minus the effects of inflation) remain at historically high levels in several EM countries.

We expect EM inflation to remain well controlled, particularly due to the deflationary pressures emanating from China, and the expected decrease in global energy and agricultural prices that should result from excess supply in these commodity markets.

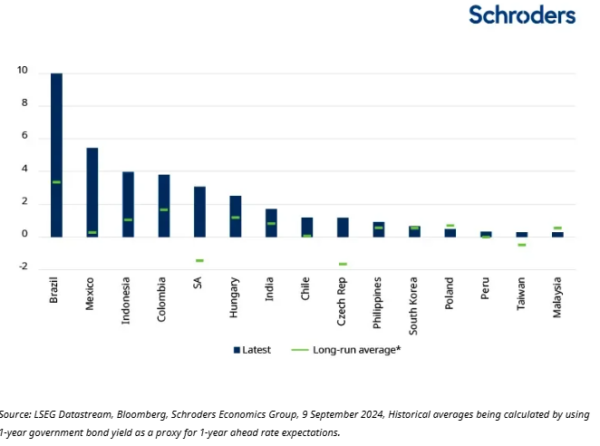

Recent fiscal concerns in several emerging markets (EMs) have already been reflected in what investors expect for policy interest rates and in the way yield curves are shaped. Figure 5 illustrates that the anticipated inflation-adjusted interest rates, known as ex-ante real rates, in key EMs are currently much higher than what has been typical in the past. This suggests that investors are pricing in the potential impact of these fiscal challenges.

There’s a renewed focus on fiscal stability in countries like Brazil, where recent market challenges are encouraging more disciplined policies. The ten-year local government bond yields in Brazil (12.8%), Mexico (10%), Colombia (10.7%), South Africa (10.4%), Indonesia (6.9%), and India (6.9%) are well-positioned to provide potentially high returns in 2025, making them attractive choices for income generation and portfolio diversification.

However, it’s important to consider active hedging of currency risks in these local bond markets, especially given the current strength of the US dollar and the potential for a renewed global trade war following the inauguration of the new Trump administration in early 2025.

CHART 5: EM ex-ante real rates – 1 year ahead market implied policy rate – 1 year ahead rolling consensus inflation forecast

![]()

Past Performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of investments to fall as well as rise.Investment involves risk.

Any reference to regions/ countries/ sectors/ stocks/ securities is for illustrative purposes only and not a recommendation to buy or sell any financial instruments or adopt a specific investment strategy.

Issued in the UK by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.