May

2020

Is it time to be Back in Brazil?

DIY Investor

9 May 2020

Whilst not my trust pick for 2020, back in October I had highlighted that the Brazilian market could be of potential interest, especially as the currency seemed to have found a level at which it seemed supported relative to the USD.

However at the same time – thankfully for me, as a get-out clause – I did warn, based on the pattern that was emerging, that “if the real falls a bit further from here and makes a new low against the US dollar, it will fall a lot further”.

Sadly, the latter has come to pass, as we can see in the graph below.

I would reiterate that, with the clarity of hindsight, this now resembled what market technicians would call a ‘cup-and-handle’ formation; when the USDBRL exchange rate broke the resistance level of c. 4.17 sustainably, we saw an acceleration to the upside.

There were, of course, qualitative reasons for this, particularly related to continued interest rate cuts in Brazil, and the concern over the coronavirus pandemic precipitating a USD squeeze.

I would say these concerns are more important, but most technicians would argue the signal was there that something was going to happen and that the signal was more important than the reason.

USDBRL

So FX has been decidedly unhelpful; yes, sterling has not exactly been strong against the USD, but has seen nothing like this sell-off.

And we’ve had this FX headwind into a period when Brazilian markets, in conjunction with other markets across the globe, have performed brutally.

In the chart below we can see the long-term returns from a Brazilian market index in GBP terms.

This uses a log scale to ensure recent volatility is better reflected, and is not visually amplified as a result of significant nominal growth over this time.

We can see clearly that – whilst not unprecedented – the recent sell-off is pretty drastic, even for what has been a volatile market. We can also see that the market has gone essentially nowhere since 2010.

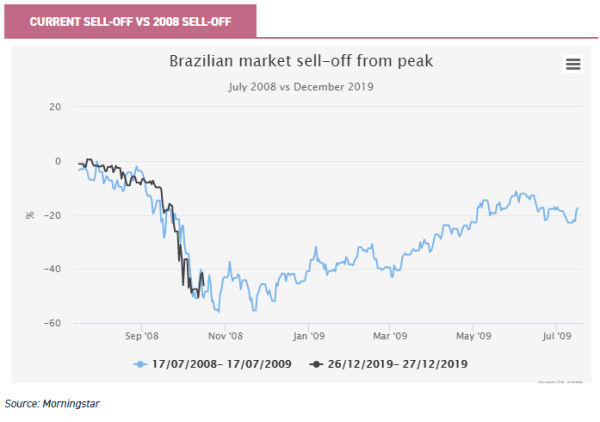

So, the sell-off has been dramatic. We are (at the time of writing) approximately 46% below the peak reached on 26/12/2019 in GBP terms, and worse in USD (which is more relevant for international and domestic Brazilian investors).

But, as noted above, this is not entirely without precedent. There are some historic instances of similar sharp sell-offs. If we look at the drawdown from the three month peak (encompassing the historic peak above at the time of writing), we have seen 78 individual instances where there has been a drawdown of greater than 50% (which was briefly surpassed earlier in March).

These occurred in two clusters: 1990 and 2008. Daily data is not available for the Brazilian market in 1990, but the similarity between the current sell-off and that which occurred in 2008 is striking. Both time periods are taken from their three-month peak in the chart below.

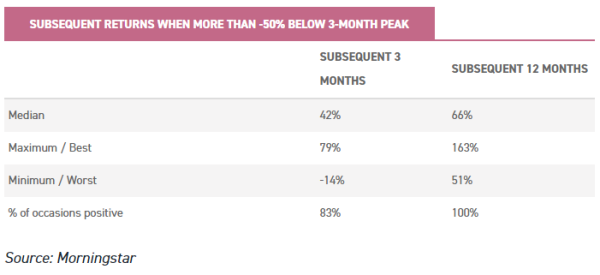

When we look at subsequent returns in both these instances, they were on average very strong. We can see the range of subsequent returns in the table below, which shows subsequent returns from all 78 daily instances where the market had sold off by more than 50% from the three-month peak.

However, some qualitative considerations are of course essential. Investor sentiment may have reacted similarly to the past, but that doesn’t mean the follow up will be the same.

Retail investor participation in the market had surged in Brazil; traditionally retail investors were largely in government bonds, which had offered very sizeable interest payments, but the sharp fall in nominal (non-inflation adjusted) yields had led to an increase in retail buyers in the equity markets. Whether these investors will be readily willing to return to the stock market remains to be seen.

Similarly the USD funding question remains a key concern across the globe: recognising that there were liquidity issues across the globe, the US Fed has introduced swap lines with major central banks across the world, including in Brazil.

This move has helped ease short-term upward pressure on the USD, but in essence has brought forward supply and deferred demand.

There is little doubt that if a global squeeze in USD liquidity – coupled with the economic sudden-stop we are currently seeing – started to trigger a credit event across the world, then the Brazilian market would suffer in line with all global markets.

More positive, however, is a surfeit of anecdotal evidence that throughout much of 2019 Brazilian corporates were refinancing USD debt in Brazilian reals, adding to downward pressure on the BRL; the depreciation of the BRL means that external debt burdens relative to output have stayed broadly stable/risen slightly, but this is a better outcome than the sharp rise that would otherwise have occurred.

The stock market valuation has de-rated, but earnings forecasts don’t appear to have significantly accounted for the spread of COVID-19, with market forecasts only moderately lower (and thus valuations may not yet reflect realistic earnings expectations) – though average profit margins remain low relative to their history.

However, Brazil underwent the worst recession in its history in the early 2010s; companies that survived have proven their robustness, and, whilst Brazil does not exist in a state of autarky, the economy is largely focused on domestic activity with relatively low trade volumes relative to total economic activity.

The share prices of trusts such as JPMorgan Brazil (JPB), Blackrock Latin America (BRLA), and Aberdeen Latin American Income (ALAI) have, unsurprisingly, reflected the wider market turmoil, whilst these trusts have experienced their Net Asset Values (NAV) fall by c. -42%, -45% and -38% respectively from their peaks.

With NAVs falling sharply, we haven’t seen a particularly increased discount opportunity in these trusts, but should the market rebound we should likewise see NAVs bounce back, particularly if these vehicles provide geared exposure to a rising market.

Against this backdrop, Blackrock manager Ed Kuczma is positive on the prospects for the Brazilian market, highlighting that current market volatility is creating increasingly attractive opportunities in Latin American markets, in companies which offer accessto structural growth opportunities.

Blackrock’s longer-term thesis for Brazilian stocks remains intact; though they have had to adjust growth expectations downwards in the face of cooling economic activity in Q1 2020, the benefit that structural reforms could offer gives the potential for outperformance of EM peers

Click to visit:

Past performance is not a reliable indicator of future results. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. In particular, this website is exclusively for non-US Persons. Persons who access this information are required to inform themselves and to comply with any such restrictions.

The information contained in this website is not intended to constitute, and should not be construed as, investment advice. No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not a recommendation, offer or solicitation to buy or sell or take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm’s internal rules. A copy of the firm’s Conflict of Interest policy is available on request.

Commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.