Apr

2024

Investing Basics: Investing in Trade Finance

admin

7 April 2024

“World can run without money and currencies but not without business and trade.” Amit Kalantri

Trade finance should be the most well known of asset classes; this article describes what it is, and how you might go about investing in it – by Philip Gilbert

Essentially, everything we consume, wear, and use forms part of global trade, much of which is subject in some way to financing. Trade finance is one of the oldest forms of banking, and still today forms a large and stable part of global banks lending.

Families, and family firms such as Flemings, Barings, Rothschild, Hambros, Medici’s, Rathbones, Harry Tate (Tate & Lyle), Jardine, Matheson & Co. all founded their fortunes on trade and the financing of it.

Trade and the financing of it are an old as civilisation itself. The first records date back to the 19th century BC, where the evidence to the existence of an Assyrian merchant colony at Kanesh in Cappadocia (now part of Anatolia), other highlights include:

- The establishment of the Silk Road to finance trade between East and West

- The Hanseatic League secures trading privileges and market rights in England for goods from the League’s trading cities in 1157.

- The Italian bank in Lombardy are founded, and cities such as Venice and Florence become important centres, with families such as Medici to the fore

- Money was created to be a medium of exchange that represented the value of goods

- The British Empire and its famous merchant banks and finance houses, and institution such as the British East India Company (which received its Royal Charter in 1600) were all founded on world trade

- The Dutch East India Company is formed in 1602.

- The first English outpost in the East Indies is established in Sumatra in 1685.

- The Cobden-Chevalier Treaty, is finalised in 1860 between the United Kingdom and France, is the first international free trade agreement; it leads to successive agreements between other countries in Europe.

What is trade finance?

Trade finance is a loan that funds the sale or purchase of goods, often across borders. The structure of that loan might be a letter of credit, factoring and direct lending, and, in recent years, supply chain finance – but the practice is as old as banking itself.

Unlike corporate debt, which might be used to fund speculative buyouts, or “general corporate purposes,” trade finance is tied to a specific transaction, for example, the shipment of soya beans from Brazil to the US. Therefore:

- trade finance loans can be collateralized with the underlying commodity itself

- Self-liquidating. Once the sale is complete, the loan is paid off.

There are a number of safeguards that are normally put into place to protect the lender.

- The goods are fully insured, this is paid for by the importer and exporter, not the lender

- The goods are monitored by, or on behalf of, the lender during the term of the loan

- back-up off buyers are in-place should the original buyer not complete for any reason

Trade finance loans are often short term, decreasing the duration risk for investors. Depending on the sector, the average finance period runs between 90 to 120 days.

The impact of the Basel III global banking regulations has reduced the ability of banks to meet the funding required to match the predicted growth in international trade. According to estimates from Standard Chartered Bank, the new proposals will lead to an increase in trade finance pricing of between 15% and 37%.

‘I am more concerned with the return of my money that the return on my money’

This in turn, according to the bank, could lead to a reduction in trade finance volumes of 6%, which would also mean a reduction in global trade by $270bn per annum, and a 0.5% reduction in global gross domestic product. Source: The Wall Street Journal

Why Invest in Trade Financing?

- Trade finance loans are historically considered safer investments:

- Between 2005 and 2009, only 1,089 trade finance transactions defaulted out of 5.2m transactions from nine leading international lenders, for a default rate of about 0.02%, Source: International Chamber of Commerce and the Asian Development Bank.

- This is comparable to the long-term average default rate for companies rated AA by S&P, Source: UK-based Equity Development.

- Trade finance is resilient to crisis,:

- During the crisis of 2007-08 only 445 international trade defaults were reported out of 2.8 million transactions conducted over this period.

Source: International Chamber of Commerce

- Essentially world trade continued to function financed by the trade finance procedures defined over hundreds of years.

- Even countries in default need to ensure that trade finance obligations are completed in order to allow supplies of food and other basic necessities to continue.

- Trade financing is secured: funds advanced to producers are typically guaranteed by the goods themselves. Furthermore, they are insured to overcome weather issues, loss as sea etc.

- Duration; trade finance loans rarely exceed 120 days, therefore the loan is self-liquidating.

What are the risks?

The financing of trade has historically formed a core part of a bank’s own lending activities. Global banks are active providers of revolving trade backed financing. Set out below is a table produced by Bank for International Settlements highlighting the trade finance assets held by a number of banks:

The reason? It is inherently low risk.

The loans are short term. The security of loan is over collateralised against a real asset with real value (goods). There is no market price movement risk as the goods are pre-sold. The credit risk is almost always to the bigger company in the chain (money goes to a farmer but is owed from the mill, for example).

- Loss of goods? Theft? Fraud? Default of the purchaser? These are the key considerations in any trade deal. Insurance is normal on all goods shipped (even e-bay suggests you do this).

- The difficult part is the credit checking of the purchaser and this is where an experienced operator is essential. Like a bank who collects all that annoying information when you want a mortgage, there are systems and people in the world who are specialists in credit checking. The right skills are key to reducing risk.

- How can an investor be sure? Like any other investment, you can ask for advice, read around the subject, and look for a credit rating assessed by an approved credit rating agency.

How do I Invest in Trade Finance?

As a result of the Basel III regulations, a number of global banks including Santander, Citibank, and BNP Paribas have issued bonds secured by trade loans. This type of transaction is referred to as securitisation, and the security is referred to as collateral. Essentially, the interest on the trade finance loans services the bonds coupons, at maturity investors capital is returned as the loans are self-liquidating.

Whilst this sounds complicated a parallel can be drawn with a retail bond issued by Bruntwood Investments, which was secured on a portfolio of commercial properties. A bond based on trade finance would be secured (collateralised) on a portfolio of trade financing agreements covered by way a 100% first lien on the underlying commodities.

As with Bruntwood, the issue could be over-collateralised, e.g. Bruntwood issued £50m worth of bonds which we secured over £70m worth of property, protecting investors against potential falls in asset prices. However, as trade finance loans are of short duration, typically

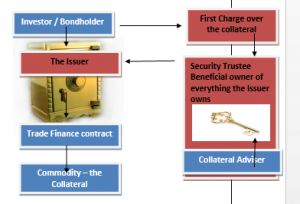

How Secure is the Security (Collateral)?

The answer is simple it ‘very secure’. The beneficial owner of the first lien on the goods is the Trustee on behalf of Bondholders. All assets of the Issuer will be held within the Security Trust. Bondholders will have a direct first legal/security charge over the assets of the Issuer, via the Security Trust.

Essentially, the assets, either cash waiting to be lent or re-lent, or the first charges over the assets are locked in the Security Trust which acts like a safe; the only person with the key to the safe is the security trustee who is the beneficial owner of behalf of the bondholders. The Security Trustee is usually a global institutional such as US Bank Trustees, Citigroup, etc.

Conclusion

As with any form of investing a bond based on trade finance is not suitable for everyone. Like all bonds it will produce a regular fixed income flow, however, unlike many bonds it is secured on the underlying collateral, i.e. 100% first lien on the goods.

Some of the key concerns for bondholders might be:

- The Coupon: coupons can vary but 5.5%+ is feasible

- Loan-to-value: Investors can be immunised from first 25% of any loss

- Duration: as the underlying loans are often

- Default: historic defaults are circa 1% p.a. or lower

- Liquidity: issues can be listed as retail bonds on the LSE which provides ongoing liquidity

- Accessibility: issues are designed for retail investors

First published on October 2018

Alternative investments Commentary » Alternative investments Latest » Commentary » Financial Education » Fixed income Commentary » Fixed income Latest » Latest

Leave a Reply

You must be logged in to post a comment.