Oct

2020

Investing in Modern Media

DIY Investor

12 October 2020

In 1939, as many Americans attending the World’s Fair in New York stared in wonder at the recently invented TV, the NY Times haughtily dismissed the new technology. It could clearly never compete seriously with radio because “people must sit and keep their eyes glued on a screen; the average American family hasn’t time for it.”

Each time a new medium comes along, folk believe it will kill the earlier form – printing presses putting monks and scribes out of business, cinema killing books, television killing radio, social media killing all.

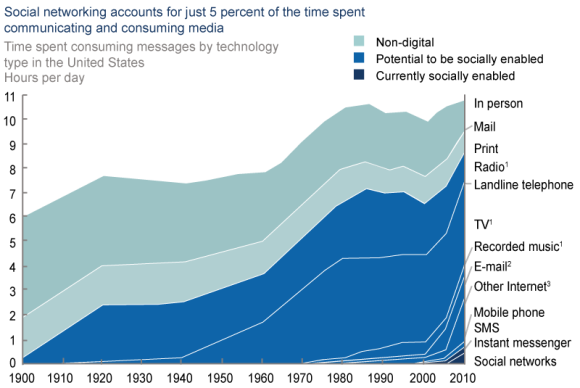

What is interesting – as this chart from McKinsey shows – is just how much time Americans – and the rest of us – have actually managed to find for each generation of new technology.

1 Radio, TV, and recorded music are slightly discounted to account for the time spent using these concurrently with other media. 2 Does not include email sent internally within companies, which is not counted as internet traffic. 3 Includes all social technologies that cannot be explicitly separated in available data.

Source: Bureau of Labour Statistics; WAN-IFRA; Statistical Abstracts; National Bureau of Economic Research; US Census Bureau; Radicati Group; Yankee Group; Nielsen; ITU; eMarketer; and others; McKinsey Global Institute analysis. Graphic via www.mckinsey.com/industries/high-tech/our-insights/the-social-economy.

A key driver of this growth is the way new technologies have made content available ubiquitously – whatever we are doing and wherever we are in the world. Where once we were constrained to reading a newspaper (ironed) over breakfast, now commuters stream the world into their EarPods.

So what does this mean from an investment perspective? Our Media theme has been successful over the years, particularly benefiting from AT&T’s bid for Time Warner and from content-makers selling to a growing global audience. But the world is changing, and with it our strategy changes too.

Stock markets don’t like industries which see higher volumes but lower margins, and that is the ultimate outcome of many of the new technologies. There are two key models for funding media – advertising and subscription – and both have their challenges.

The advertising model: Where is the audience?

The advertising-funded media of the past include part of the newspaper industry, free-to-air television, US radio, billboards and now social media. What most advertisers want is reach –their product in front of as many of their targeted consumers as possible.

Traditional TV was very good at this, but as advertising migrates from free-to-air channels to digital channels, its reach shrinks and so it is left with a smaller programming budget. This raises concerns for the likes of ITV. However, even if Downton Abbey is too expensive to make, there is a steady audience for Pointless and Countdown – shows that are very cheap and whose audiences comprise a fair chunk of the target for mass market consumer products. So old media will still retain a sizeable share of revenue – but it is under threat.

The largest TV viewing audience in the US is for the Superbowl. In 2017, 111 million people watched the Patriots beat the Falcons. This was slightly down on the previous year, which was slightly down on the year before. A 30-second advert cost $5 million (Business Insider 02/17), $45 CPM (cost per thousand viewers).

Facebook’s North American daily average users number 239 million (Statista 12/17) and recent advertising rates are around $11 CPM (Economist 12/17). And then there is the rest of Facebook’s world to reach. That’s why Facebook keeps taking advertising share.

Lastly, social media enables more targeted marketing, allows collaboration and operates in real time. These features are very powerful in enhancing information flow in the education, technology and perhaps medical sectors. It is less clear that they enhance media capabilities in the consumer goods or energy industries. Perhaps their largest impact could come in government, where the ability to interact with the electorate between elections has been enhanced by these new technologies.

Influence brings responsibility …

This huge ability to influence has political consequences. The last few months have seen Facebook’s management rapidly change from doubting that some had used their site to influence the US presidential election. The questioning of social media companies by Congress was weak and showed members were ill-informed (as are UK and European politicians.) But Silicon Valley seems to recognise the need to get its own house in order. Any medium wants to be seen as a comfortable place to spend time. Allowing trolls too much freedom, as Twitter has, makes a large part of the audience leave.

Facebook tends to describe itself as a market place, but the landlord of a market place would do well to keep the loos clean. The cost of doing this may bring down the margins of these exceptional businesses somewhat: they can easily afford this, and they could pay some tax besides. If they were regulated like traditional publishers, they would find their costs escalating very quickly. Obligations such as showing balance in political reporting would be very awkward – but probably not impossible to implement.

The subscription model – who do you want to be?

A network like ITV needs you to watch hours of television as advertisers pay per viewer. A subscription channel just wants you to pay the subscription, regardless of whether you watch anything. Often it will focus on a range of strong-affinity, small-audience programmes, rather than take-it-or-leave-it, mass-market programmes.

HBO gives a model for the subscription channel. Nobody who pays for it plans to watch all or much of its content. The hook that brought the subscriptions was often rather dark, non-mainstream drama – The Sopranos, Six Feet Under, Game of Thrones – the antithesis of family viewing.

And then we come to Netflix. As far as we can tell, the current business model is to spend $7 billion on programmes and to sell them for $6 billion of subscriptions. At a recent meeting with our team, Netflix seemed to have no plan to break even, though it has raised its subscription price since then. Although Netflix is gaining subscribers very rapidly, to value the company we would have to assess how many subscribers will stay when the company charges more for its product than the cost of making it. Doing that assessment is beyond objectivity. So we look on Netflix as a very effective company which disrupts other business models, but not as a company we choose to select for our fund. Many companies have relied on Wall Street to fund their dreams for ever – and many of these companies are no longer with us.

Finally, the PayTV bundle model is also fraught. When people pay for an individual subscription they look for the shows they feel strongly about. When people look at their PayTV bundle, they wonder whether they can save money on all the channels they don’t want. The guts of SkyQ at £65 a month (broadband extra) have been movies and sport. Movies now compete with Netflix at £7.50. Sports have seen poor viewing figures from the peak in 2016 when Leicester won the Premier League and the Chicago Cubs won the World Series – both stories with unbeatable romance. For now, it may be a relief that Sky did not show the Ashes tour, but some may not feel it’s worth the money.

Finding hits and merchandising them …

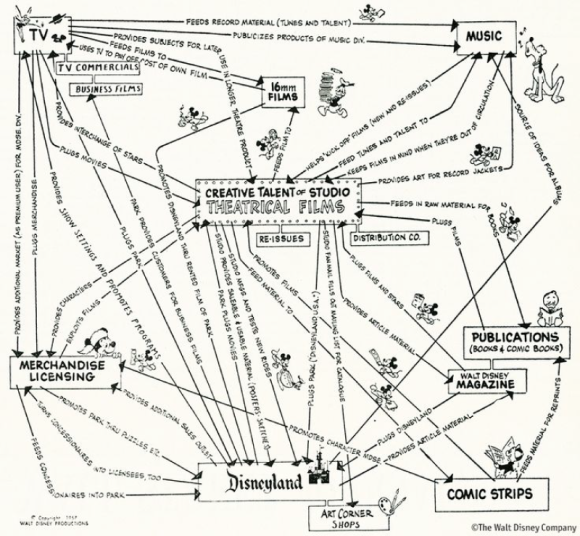

Behind the luvvy façade, the media industry has always had hard-nosed business-people looking for a predictable return on investment. One model beyond advertising and subscription that has helped has been to create a hit story and then merchandise it. Here is a Disney’s business plan from the 1950s:

Source: 1957 Walt Disney Productions, via http://www.telegraph.co.uk/business/2017/09/01/money-behind-star-wars-new-hope-global-mega-franchise/

In the 1920s, Mr Disney made films, some of which were hits and others which were not. When the Great Depression came, Kay Kamen approached him to sell merchandise, and this stabilised the business. In 1933 they sold two million Mickey Mouse watches. This financed Snow White in 1937 and that merchandise sold more than they received as ticket receipts for the film. Star Wars toy sales in the year to July 2017 were $1.4bn, compared with box office of $1.5bn. The films became marketing for merchandise and parks.

But the industry seems to be struggling to create new characters. The research shows that the public likes a novel twist on the familiar (cowboys in space with Japanese styling), but can quickly turn against being sold rehashed material. The economics of the film industry show a Pareto distribution – 80% of sales from 20% of films. As even this model has declined – Americans bought 30 movie tickets a year in the 1940s, compared to four now – they have retreated to repeating formulas. Superhero films lead the ratings, but the public is not so easily duped into a watching a remake of Murder on the Orient Express. All but three of the 30 biggest duds in movie-making history have been released since 2005.

New characters also may have a shorter life with the audience, costing a lot to establish and coping with few repeats. New shows such as The Good Doctor and This is Us have topped the US ratings this year and Designated Survivor and Bull disappeared; Will and Grace trundles on and Young Sheldon has succeeded as a spin-off from Big Bang Theory.

For the investor, content creators are getting less bang for their risked buck. Sports rights, whose inflation has kept many WAGs in handbags for years, may not act as the core of a PayTV package. Again, perhaps celebrity sportspeople are not the draw they were – Tyson Fury vs Muhammed Ali? They may be more quickly forgotten. Perhaps this is why the mighty Time Warner is happy to sell out to AT&T and Murdoch to sell his video assets to Disney.

Broadband, the shovel store by the gold mine …

Many content-creators – new and old – are struggling to generate strong, sustainable profits. Most of them need help from broadband providers to reach their increasingly fragmented audiences and keep them connected wherever they are. For the last decade, fixed bandwidth has been in excess supply as newly laid fibre was made more efficient (frequency division multiplexing). Mobile bandwidth also expanded as new spectrum was auctioned and new generations of mobile technology used that more efficiently.

The 5G technology, for which there is no currently agreed standard but which is planned for two years’ time, will again increase capacity, but often using very high frequencies which struggle over distance.

Valuations in transmission businesses are currently very modest. An added appeal is that owners of fixed broadband networks also may face less resistance to price rises – certainly BT seems to be pushing them through. In the US, the new FCC’s chairman has decided to end ‘Net Neutrality’ and ditch a regulation called Title II which allows the FCC to intervene. There will doubtless be legal challenges, but it may be hard to force the FCC to regulate something it doesn’t want to regulate. These changes may allow broadband providers to charge, explicitly or implicitly, heavy bandwidth users for the capacity they use.

We have also returned to investing in a few mobile companies in emerging markets, where price wars seem to be moderating, allowing some price increases as mobile internet use grows. In many emerging markets, there is no other way to access the internet.

We still like media but as the market changes, so do our investments. Having made money in Time Warner and Disney, we have now sold out of them completely. A new holding, reflecting the point about broadband above, is TIM Brazil which, among other things, provides mobile internet to millions of Brazilians.

To ensure you understand whether this fund is suitable for you, please read the Key Investor Information Document and Costs and Charges Information document, which are available, along with the fund’s Prospectus, from artemisfunds.com.

The value of any investment, and any income from it, can rise and fall with movements in stockmarkets, currencies and interest rates. These can move irrationally and can be affected unpredictably by diverse factors, including political and economic events. This could mean that you won’t get back the amount you originally invested. A fund’s past performance should not be considered a guide to future returns.

Risks specific to the Artemis Global Select Fund

The fund may have investments concentrated in a limited number of companies, industries or sectors. This can be more risky than holding a wider range of investments.

The fund may invest in emerging markets, which can involve greater risk than investing in developed markets. In particular, more volatility (sharper rises and falls in unit/share prices) can be expected.

Risks specific to Mid Wynd International Investment Trust

Please ensure that you understand whether this fund is suitable for you. We recommend that you get independent financial advice before making any investment decisions. This information does not constitute an offer, invitation or solicitation to deal in the securities of this fund.

The fund may invest in emerging markets, which can involve greater risk than investing in developed markets. In particular, more volatility (sharper rises and falls in unit/share prices) can be expected.

The fund may invest in the shares of small and medium-sized companies. Shares in smaller companies carry more risk than larger, more established companies because they are often more volatile and, under some circumstances, harder to sell. In addition, information for reliably determining the value of smaller companies – and the risks that owning them entails – can be harder to come by.

The fund may borrow money to make further investments, an investment approach known as ‘gearing’. This can enhance investment returns in rising markets but will reduce returns when markets fall. Financial advisers and retail investors: The company currently conducts its affairs so that the shares in issue can be recommended by financial advisers to ordinary retail investors in accordance with the Financial Conduct Authority’s (“FCA’s”) rules in relation to non-mainstream investment products and intends to do so for the foreseeable future. The shares are excluded from the FCA’s restrictions which apply to non-mainstream investment products because they are shares in an investment trust.

Any research and analysis in this communication has been obtained by Artemis for its own use. Although this communication is based on sources of information that Artemis believes to be reliable, no guarantee is given as to its accuracy or completeness.

Third parties (including FTSE and Morningstar) whose data may be included in this document do not accept any liability for errors or omissions. For information, visit artemisfunds.com/third-party-data.

Issued by Artemis Fund Managers Limited and Artemis Investment Management LLP, which are authorised and regulated by the Financial Conduct Authority.

First published in April 2019

Commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary » Mutual funds Latest

Leave a Reply

You must be logged in to post a comment.