Oct

2024

Investing Basics: Investment Trust Sectors

DIY Investor

19 October 2024

Investment trusts were once dubbed the ‘best kept secret in the City’; not any more it seems, as investors have embraced the fact that some trusts have consistently increased their dividends over decades, and have done so in the face of enormous headwinds – just one of which was the COVID-19 pandemic. By Jemima Reeves

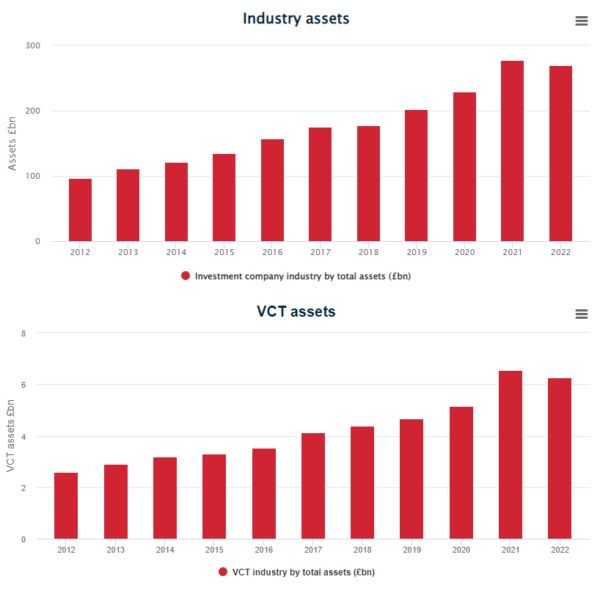

There is currently £270 billion invested in investment trusts, a figure that has doubled in less than ten years.

Once an investor decides that investment trusts might prove a valuable addition to their portfolio, the challenge is then to select one or more specific trust; with over 400 trusts currently trading on the UK stock market, there’s no lack of choice.

Fortunately, help is at hand; much of the ‘heavy lifting’ has already been done for you. The Association of Investment Companies (AIC), the trade body founded in 1932 to further the interests of the investment trust industry, regularly publishes detailed information regarding all the investment trusts listed on the UK stock market within its website – https://www.theaic.co.uk.

In order to make life easier, the AIC has segmented the industry into sectors: this classification framework provides a way of grouping companies with common characteristics in order to narrow the choices down to ones that are most likely to suit a particular need, thereby speeding up the process of search, comparison and selection.

You can find information on the specific sectors here: https://www.theaic.co.uk/aic/statistics/aic-sectors

This section of the AIC website sets out the sectors, defines them, and lists the individual investment trusts that are categorised within each sector.

Trusts reclassified

In May of last year, the AIC undertook a wide-ranging revamp of its classification framework and made a number of key changes:

- some sectors were new (about half of these came from breaking down the property and debt sectors into greater detail)

- some were renamed (although most of these were fairly cosmetic like ‘Sector Specialist: Infrastructure’ becoming just ‘Infrastructure’)

- some disappeared altogether

- a number of investment trusts were reclassified within different sectors.

In order to be categorised within a sector, 80% or more of the trust’s assets must be invested in line with the sector definition.

According to Ian Sayers, the Chief Executive of the AIC: “We undertook this review to ensure that investment company sectors accurately reflect the shape of the industry today. Recent years have seen significant growth in investment companies investing in alternative assets, such as property, debt and infrastructure and the emergence of new asset classes such as leasing and royalties. Our new sectors allow investors to find and compare companies with similar characteristics easily. I’m confident the new sectors will play a useful role in helping inform investors’ decisions.”

Why is sector classification important?

The AIC sector classification system is used throughout the industry by investors, asset managers, the media, advisers, investment platforms and data vendors.

It provides meaningful and relevant categories for numerous types of analysis, including performance rankings and data tables, peer group comparisons, and awards.

The AIC’s sectors are not an indicator of the relative risks or potential rewards of any investment trust, but are used by investors to help them identify potential investment areas, sectors or regions of interest.

Typically, investors will embark upon an investment decision journey by determining which sectors exhibit the characteristics which align most closely with their needs.

For example, if you’re a retiree, you may well want to consider sectors that specialise in delivering a high, and ideally growing, income. A younger individual with no specific or immediate needs to fulfil might be seeking a good broadly-focused investment trust that invests globally and which aims to deliver both income and capital growth. Similarly, someone who already has a reasonably well-balanced portfolio might be looking to explore something more specialist.

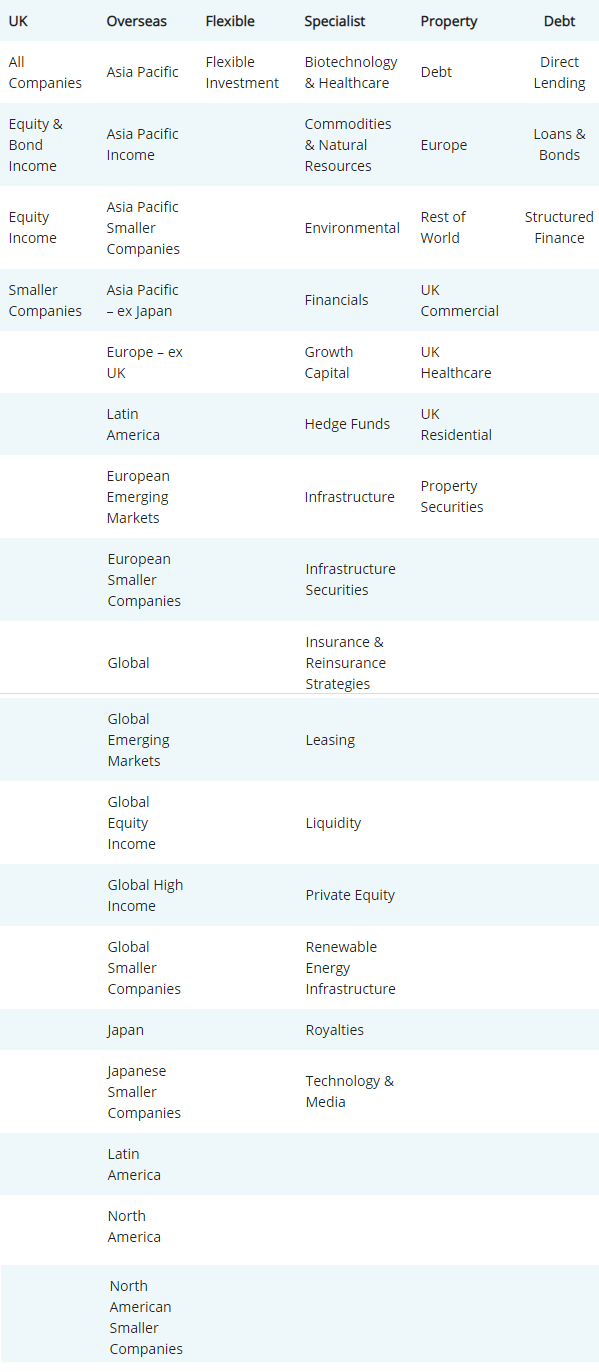

The AIC operates six core investment trust sectors (a seventh relates to venture capital trusts), and these six are then further segmented according to country/region, asset type or specialism – as you can see from the table below – giving 48 investment trust sectors in all.

Bear in mind that, whilst these classifications are based on a combination of regional or industry focus and the trust’s investment objective, they aren’t exact, in that no two investment companies are ever the same.

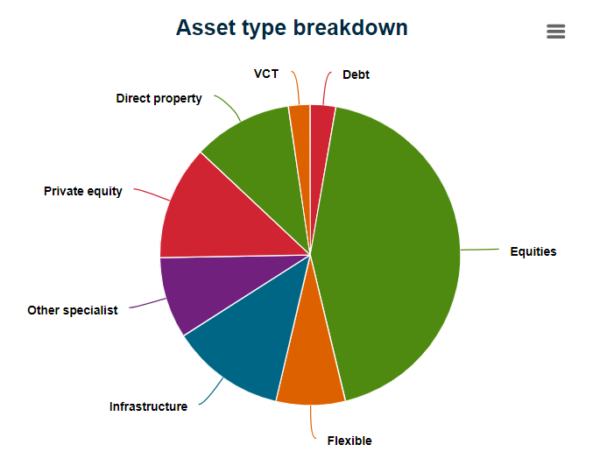

It’s also interesting to see the breakdown of asset types across the investment trust industry. As the chart below reveals, of the total assets under management of £270 billion as at the 31st August 2022, over 43% was invested in equities. Beyond that, the asset mix is relatively broad with no other asset type representing more than 10% of the industry total.1

1Source: AIC, 31/08/22

Making your final selection

By using the AIC’s sector information you should now have a good feel for the type of trust which best suits your needs, and therefore the relevant sector(s) to consider. The next stage is to identify the best performers within those sectors. You can do this by, again, reviewing the wealth of past performance data within the AIC’s website and/or by visiting the websites of the trusts themselves (whilst remembering that past performance isn’t an indicator of future performance) and undertaking as much research as you can: study the factsheet, listen to any investment commentaries from the fund manager, analyse the trust’s major holdings and download the latest annual and half-year reports.

Notes

Please refer to our glossary for more detailed definitions of our data points.

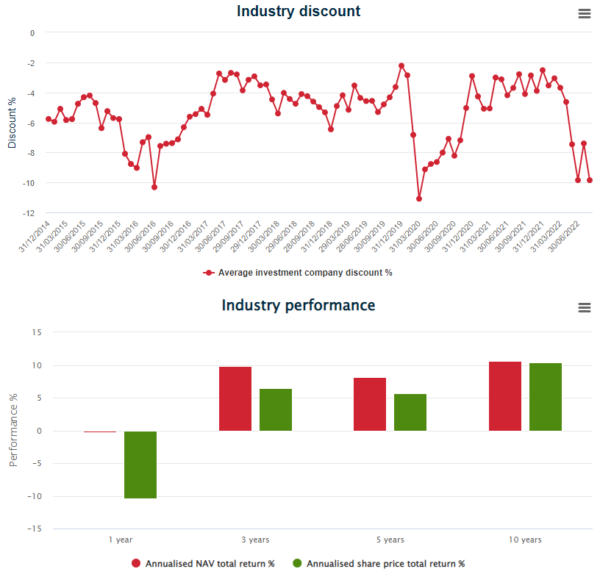

- Source: AIC/Morningstar. Data will be updated for the previous month-end on the seventh working day of each month. Discount, performance and yield figures exclude VCTs.

- Discounts are weighted by market capitalisation of company and are based on cum-income, fair-value net asset values (known as cum fair NAVs).

- Share price performance figures are weighted by market capitalisation. NAV performance is based on, and weighted by, Cum Fair net assets.

- Average yields are weighted and include dividends paid from capital profits but exclude any special dividends.

- Fundraising information does not include issuance of shares from treasury.

Disclaimer

This data has been prepared by the AIC using Morningstar data and is for information purposes only. It is not an invitation or inducement to engage in investment activity nor does it purport to contain information on which to base investment decisions. Whilst the AIC and Morningstar have taken all reasonable steps to verify the statistics on our website, neither the AIC nor Morningstar accept responsibility for any errors or omissions in this publication or for any loss of any nature incurred by any person using this publication, howsoever caused. Past performance is not a guide to future performance and the performance of individual investment companies can diverge significantly from any average figures. Investors are advised to seek independent financial advice before making any investment decisions.

Commentary » Financial Education » Investment trusts Commentary » Investment trusts Latest » Latest » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.