Jun

2021

Inflation Protection: What’s the best recipe?

DIY Investor

6 June 2021

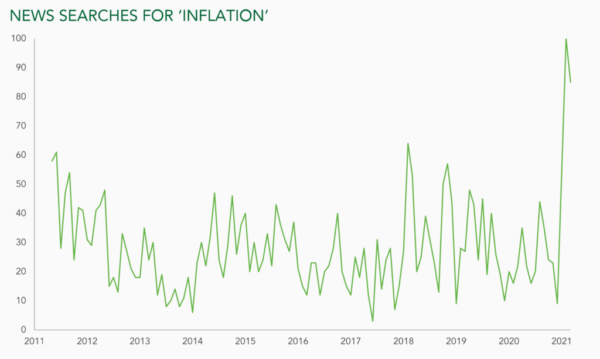

Inflation is in the news again. Many prices are rising even before we can physically get out and spend, and governments are pouring vast amounts into the economy – writes Steve Russell

Whichever side of the inflation debate you are on, it makes sense to assess the impact inflation could have on portfolios. Most of today’s investors have never seen meaningful inflation in the whole of their professional careers. So, as we emerge from lockdowns and pent-up demand meets ongoing supply constraints, we consider how different asset classes might fare if inflation does return.

Bonds – higher inflation will be the death knell for the bull market in conventional bonds. Between 1946 and 1981, 30-year US Treasuries lost over 80% of their value and British Consols lost 97% of their purchasing power (according to Reuters). Government bonds became known as ‘certificates of confiscation’. Before we even consider equities, this spells the end of the 60:40 portfolio.

Take some index-linked bonds, mix with value/commodity equities, add a decent slug of gold and, if liked, at most a pinch of infrastructure

Cash – inflation is the erosion of the purchasing power of money. If interest rates are kept below the level of inflation, as the US Federal Reserve has promised, huge amounts of cash and money market funds could be in search of a new, inflation-proof home.

Equities – many investors who have never experienced inflation are pinning their hopes on stocks to ride out any storm. But periods of high inflation have been disastrous for stock markets. As inflation rose between 1966 and 1974, the US cyclically adjusted price/earnings ratio (CAPE) fell from 24x to just 8x (Financial Times figures). Even if interest rates are held to the floor, rising inflation means the discount rate on future earnings also rises. This would be a calamity for highly rated growth stocks and profitless businesses.

Commodities – getting warmer now, as long as inflation is accompanied by strong economic growth. This could happen as we recover from the pandemic, so this is the best place to hide within equity markets.

Infrastructure – the ‘inflation protection’ of choice for many. Essentially disguised bonds or equities with inflation-linked revenues. At risk from a derating of equities or bonds, with added illiquidity and execution risk. Most infrastructure projects rely on governments to honour the inflation promise – and governments have a habit of changing the terms of trade – remember solar energy subsidies?

Gold – a centuries-old inflation hedge. Deserves a place in a diversified portfolio, despite possible mounting competition from bitcoin.

Index-linked bonds (UK)/Treasury Inflation-Protected Securities (US) – the clue is in the name. Hiding in plain sight, but missing from too many lists of inflation protections. They pay income that rises with inflation and return your capital with compensation for inflation. If inflation returns, and especially if interest rates are held below the rate of inflation, investors could find themselves panicking into this asset.

Our recipe for protecting against inflation: take some index-linked bonds, mix with value/commodity equities, add a decent slug of gold and, if liked, at most a pinch of infrastructure. Avoid conventional bonds and high-priced growth stocks as these stop your mixture rising. Beware cash – it can cause a bitter aftertaste.

This article was originally published by Ruffer and is here republished with permission.

Published by our friends at:

Commentary » Equities » Equities Commentary » Fixed income Commentary » Fixed income Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.