Nov

2025

How to Protect Against Inflation

DIY Investor

23 November 2025

Transitory or not, Inflation is back.

Transitory or not, Inflation is back.

It will affect your portfolio and may impact your life.

If your portfolio is already set up to reach your goals and hedge against most risks, returns should offset any inflation in the long run.

But there is a small chance that Central Banks won’t get the job done to slow down inflation. If you think that’s the case, extra protection may be worth considering.

Here are the best ways to protect against unexpected inflation.

Ways of Protecting Your Portfolio Against Inflation

To reduce the impact of high unexpected inflation on your portfolio returns you may consider Inflation-linked Bond ETFs, investing in physical Real Estate, or Equities with business models having the ability to pass on costs.

Choosing a Government Bond ETF with low duration can also mitigate impact.

What about Bitcoin and Gold?

Certain inflation hedges are obvious. House prices slowly adjust to maintain similar or higher value.

Other diversifiers react to sudden unexpected spikes in inflation.

In Nicholas Taleb’s words “I have learned through history that there is no such thing as inflation anymore. There is hyperinflation or nothing”

This is why having a minor exposure to very reactive assets like Gold or Bitcoin can be useful.

Read on to understand how to diversify your hedges.

‘Having a little inflation is like being a little pregnant’

Why Bankers Don’t Care (for now!)

The key reason why bankers delay rate hikes to slow down inflation is that the accumulated public and private debt is massive and would impact its repayment and thus economic growth.

The other reason is that, believe it or not, central bankers like inflation. As Russell Napier framed it “a central banker is someone who will permit inflation in anything except wages“.

In fact, a 2% inflation target is the most desired outcome. A temporal overshoot to 3-4% is probably acceptable as long as it brings them closer to the 2% goal.

Up until COVID-19 this 2% was hard to achieve because deflation is a powerful force. Consider this:

- China and Emerging Countries – manufacturers can manufacture anywhere in the world where labor is particularly cheap thus reducing prices

- Artificial Intelligence and Robotics – ongoing innovations are all designed to produce better goods and services at lower and lower prices

- Millennials – tend to have fewer kids and are minimalists. Older populations like Japan or Italy (yes, Italians are on average as old as the Japanese) are also less prone to spending

Why you Should Care

What type of tax is Inflation?

Inflation is a hidden tax.

As Milton Friedman once said, it is a tax without legislation.

Inflation penalizes those who lend money and favors those that borrow.

Your Bond ETFs are taxed. Since as a bondholder, you lend money.

Your Cash is taxed. As inflation rises your cash becomes less valuable.

Equities tend to underperform too. Although in the long run, they will outperform Inflation.

How does Inflation affect Stock Market?

One of the things that may not be intuitive is that when you buy a stock or a bond, current inflation expectations are built into the price that you pay.

The discount rate on stocks and bonds includes inflation expectations.

By expecting high inflation you have no edge over other market participants.

Why is this important?

You may read in financial news about recently published realized inflation (e.g. 5%) but it may be a rate that was already baked into the calculation of the long term average expected inflation.

Only inflation that is currently not expected by the market will move Equity and Bond prices.

Will Inflation Rise?

The market expects inflation to rise this year.

In fact, by looking at Bond and Equity prices you can extract the current expected inflation rate.

For example, you can find out what the market expects (i) through data from the central bank or (ii) by comparing inflation bond and nominal bond yields:

- In the US the rate is provided by the FED. Here you can check the annual average inflation for the next 5 years which is currently 2.5%.

- In the UK, the 10-year average implied Inflation is provided by the Bank of England. The expected annual inflation over the 10-year time horizon is currently 3.75%.

- In Germany, the 10-year average Inflation can be calculated quite easily. Take today’s Bund yield and subtract the real yield from today’s Federal Inflation- linked bond. Currently, the market expects a quite moderate 1.7% increase per year.

- In other European countries you may get an estimation from the central bank or by looking at bonds. Read how to get this estimation in the technical addendum below.

For example, you would need annual inflation to be higher than 3.75% in the UK for Equity and Bond markets to react.

Inflation-beating Assets

The perfect hedge against inflation doesn’t exist.

But a combination may do the trick.

The CFA Institute defines a perfect hedge as an asset fulfilling three criteria:

- In needs be very reactive to inflation (provide return)

- Price reaction must be consistent over time (reacting every time inflation materializes)

- Have the lowest cost (hedges have an opportunity cost because most assets underperform Equities in the long run and this will drag the performance of your portfolio)

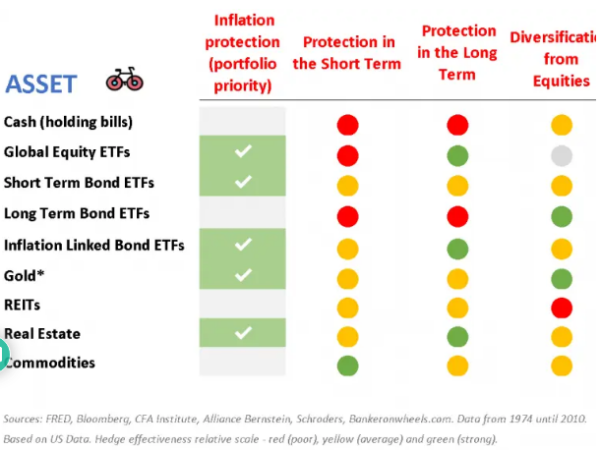

Asset Comparison

Relative protection in the short and long term and portfolio diversification benefit

How do I read the above table?

Let’s look at how different assets protect your portfolio from inflation:

- Portfolio Priority is a suggested prioritization in overweighting an asset for (extra) protection against unexpected inflation within your portfolio.

- Short Term Protection reflects if assets are being reactive. For example, Gold is very reactive to hyperinflation but not mild inflation.

- Long Term Protection is linked to long-term outperformance. For example, Gold is generally inconsistent in the long run.

- Diversification is also key when constructing a portfolio. For example, Long Term Bonds will underperform in an inflationary environment but will protect you in other scenarios (e.g. during a 1929-style deflation or during major economic downturns). A good compromise between short and long-term Bond ETFs to account for any scenario could be medium-term Bond ETFs. The below analysis only focuses on the unexpected inflation protection aspect.

Hedges for Extra Protection

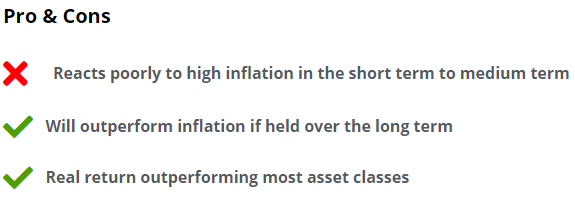

Global Equities

How to use them in a portfolio

- It is prudent to have a broadly diversified portfolio as a solid base since sectorial inflation impact is not straightforward to estimate.

- Global Equities will outperform in the long run and you may remain totally passive.

- Growth Stocks tend to suffer more compared to Value Stocks as inflation and rates rise given their long-dated cash flows (higher duration impact).

- But while it may be tempting to consider Value stocks as a hedge, there is currently limited evidence implying a relationship according to research from AQR.

- Trend-following strategies tend to outperform, according to research from Man Group. I’m not convinced they do after considering implementation costs and time spent.

Why are stocks affected by inflation?

All assets are driven by two factors – growth and inflation.

For Bonds where the coupon is fixed inflation impact seems intuitive to understand.

Similarly, not all companies can keep margins and pass on the increased costs to the consumers. But all of them suffer from higher demanded yield by investors, thus impacting equity prices.

What stocks benefit from inflation?

If you want to take directional bets, Energy stocks have historically outperformed since commodities tend to be strongly correlated to inflation. However, Energy stocks are more significantly exposed to equity market movements than to commodities. This means they provide limited diversification to the rest of your global equity portfolio. Materials have also sensitivity to unexpected inflation.

If you do decide to hedge actively, consider energy companies that are also green-friendly.

Tech, healthcare, consumer goods, or utility stocks have generally underperformed.

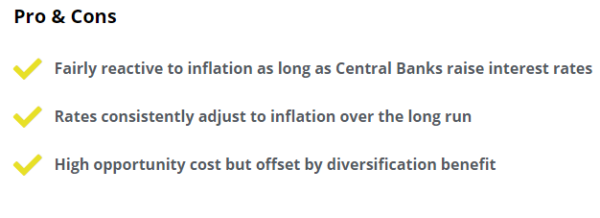

Short Term Bonds and Savings Accounts

How to use them in a portfolio

- Keeping an allocation in Short Term Government Bond ETFs or Aggregate Bond ETFs is a surprisingly effective strategy. As long as Central Banks react to inflation, which historically happens in a majority of cases.

- Look for Bond funds that have a short duration (e.g. 2 years) since it won’t be much affected by rising interest rates. If you want to intuitively understand how duration (and inflation) affect Bond ETF returns, have a look at Bankeronwheels.com Bond ETF Calculator.

- Not only should rates adjust once the central banks start raising rates but also it provides rebalancing opportunities to buy cheaper equities that may suffer from inflation.

- Your Bank’s Saving Account can also be a decent option as long as the guaranteed returns track market rates.

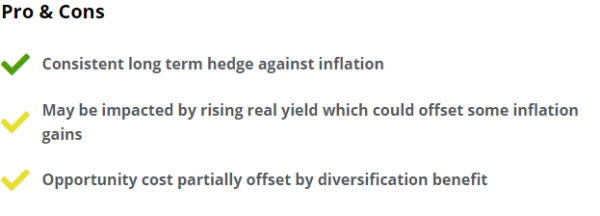

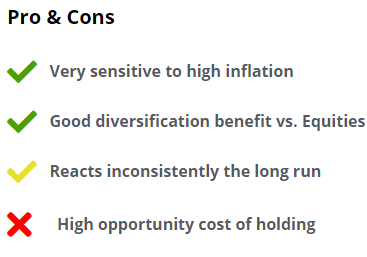

Inflation-Linked Bonds

How to use them in a portfolio

- I think that adding Inflation-Linked Bond ETFs as the main Inflation hedge is sensible due to (i) sensitivity to inflation and (ii) long-term consistency.

- However, Nominal Bond ETFs usually provide better diversification than Inflation-Protected Bond ETFs. That’s why a combination of both Bond ETF types in a portfolio is the ideal mix.

- If available, when choosing an Inflation Bond look for a duration that aligned with your investment horizon to match the inflation hedge (or short duration for a Bond ETFs). If you do that, you’re guaranteed to maintain your purchasing power, less the (currently negative) real yield on the bond at the end of the investment period. The low/negative real yield is the price to pay to hedge and diversify your portfolio.

Gold

How to use it in a portfolio

- Gold protects predominately when real interest rates fall and that’s why it’s a very good diversifier for Equities.

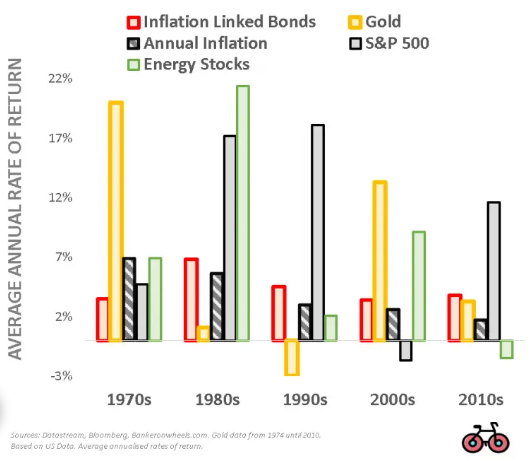

- It has a side benefit of being very sensitive to very high inflation (look in the graph below at how it overshoots in the 1970s, providing great inflation protection).

- However, given the rate sensitivity and price volatility, it is not a consistent hedge over time, especially in a low inflation environment. In such cases, it may take decade(s) to maintain purchasing power.

- Your allocation should consider that it is a drag on performance vs. Equities in the long run and the fact that it’s a volatile asset class. Learn more about why Gold is controversial but also why a small allocation in your porfolio has merits.

Bitcoin & Wine

While theory suggests a minor inclusion in the portfolio for diversification, crypto has so far limited data to argue it will effectively hedge against inflation.

But MAN Group research suggests any collectibles are resilient strategies against inflation – wine, stamps, art, and maybe one-day NFTs.

Consistency of Inflation-Linked Bonds Protection

Diversification of hedges is the most prudent strategy, according to Alliance Bernstein’s research.

But the most consistent hedge, in the long run, are Inflation-Linked Bonds.

Assets to Avoid

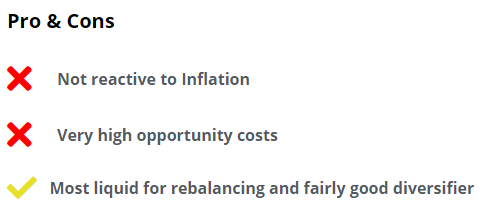

Cash

Why using it in a portfolio is not optimal

- A small allocation for liquidity purposes can be justified

- But cash is generally better kept in Short Term Bond ETFs or Saving Accounts that don’t lose purchasing power

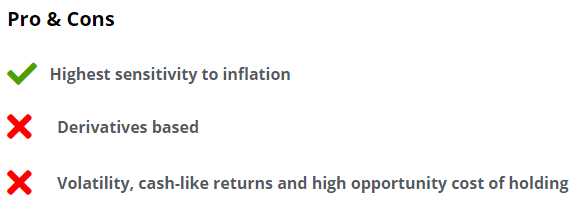

Commodities

Why using it in a portfolio is not optimal

- While commodities have historically been a great hedge, I’m not an advocate of including commodities into a portfolio. Great in theory, not so much in real life since (i) investors usually don’t understand what these funds hold (derivatives) and (ii) ETFs holding future contracts may not be able to replicate correctly the price of the commodity (contango).

- Importantly, in the long run, commodities do not generate returns above 1% and are very volatile.

- The other question we may ask is ‘aren’t we looking through the rear mirror?’ While energy and material still drive price increases future inflation may not come from oil/gas or certain materials as it used to. In the new age, e.g. semiconductors could become a material driver. For example, Taiwan was swapping Chips for Vaccines. Decarbonization may also play a role, according to JP Morgan.

- I would tend to overweight (Green-friendly) Energy Stocks rather than investing through commodity ETFs if you consider commodity-related directional bets.

REITS

Why using it in a portfolio is not optimal

- Higher inflation tends to lead to higher long-dated government bond yields and property yields as investors

demand a higher income to offset the increase in inflation. This negative effect is immediate. - However, the upside of investing in Real Estate takes time to materialize. The UK, US, and Japan have experienced a closer relationship between property returns and inflation over a ten-year period than over a one-year period.

- Certain REIT sectors react better to inflation like residential assets where short-term leases readjust quicker.

- A much better alternative is to buy physical real estate, where you are the borrower, and both asset prices and the mortgage play in your favor.

Technical Addendum

Expected Inflation in Your Country

How do I calculate the future Inflation rate?

Step 1 – Look up Bond yields

You need to find two bonds (one nominal and one inflation linked) with broadly the same maturity.

Usually, the best candidates are 5 or 10-year Bonds.

The implied future inflation rate can be calculated by subtracting two yields:

(i) a Nominal Yield or the yield that you earn from Nominal Bonds before accounting for inflation and

(ii) a Real Yield from an Inflation Bond which is the yield that you earn from Bonds after accounting for inflation

Financial websites may have these yields, for example in the UK:

- You can take today’s 10-year Gilt Nominal Yield. This yield before accounting for inflation is 0.8%.

- You can then use today’s 10-year Linker (Inflation Linked Bond) Real Yield. This yield after accounting inflation is -2.95%.

Step 2 – Subtract the two yields

Currently, the annual inflation expectation over 10 years is 3.75% (this is assuming you find the products given the combination of Covid-19 & Brexit).

Calculating Expected Inflation from Bond Yields

For this calculation inflation-linked bonds must be actively traded, since you need to know their real yield, as opposed to the nominal one.

Unfortunately, this is not always the case, since some countries don’t have an active Inflation-linked bond market.

The current market estimations may also not be entirely accurate.

For example, one study found that breakeven (a.k.a. expected) inflation tends to underestimate short term inflation and overestimate long term price increases.

Good Luck & keep’em* rolling!

(* Wheels & Dividends)

REFERENCES

- Vincent L. Childers, CFA Institute, ‘Inflation Hedging Strategies‘ (2012)

- Jon Ruff, Vincent Childers, Alliance Bernstein, ‘The Real Value of Gold’ (2011)

- Nicolas Rabener, ‘Myth-Busting: Equities Are an Inflation Hedge‘ (2021)

- Paul Bosse, Vanguard Research, ‘Commodities and short-term TIPS: how each combats unexpected inflation’ (June 2019)

- Teun Draaisma, Henry Neville and Otto Van Hemert, Man Institute, ‘How to defend against Inflation‘ (June 2021)

- Henry Neville, Teun Draaisma, Ben Funnell, Man Group, ‘The Best Strategies for Inflationary Times‘ (March 2021)

- Thomas Maloney, Tobias J. Moskowitz, AQR, ‘Value and Interest Rates: Are Rates to Blame for Value’s Torments?‘ (March 2021)

- Sue Wang, Vanguard Quantitative Equity Group, ‘The potency of commodities as an inflation hedge‘ (August 2021)

- Kerry Craig Ian Hui Gareth Lam, JP Morgan, ‘Are commodities still a good inflation hedge amid decarbonization?‘ (June 2021)

Commentary » Equities » Equities Commentary » Financial Education » Fixed income Commentary » Latest » Mutual funds Commentary » Take control of your finances commentary » Uncategorized

Leave a Reply

You must be logged in to post a comment.