Apr

2024

How the DIY investor can neutralise the market….Safely

DIY Investor

4 April 2024

Dr Fred Piard, author of ‘The Lazy Fundamental Analyst’, introduces his market neutral portfolio strategy and how it can work for the DIY investor

Market neutral investing uses sophisticated techniques like statistical arbitrage, delta hedging and stock picking to eliminate market risk. A possible advantage is staying in the market and not trying to time the next crash.

Market neutral investing is supposed to offer better capital protection and lower volatility but it is not a perfect solution or for everyone. Aggressive investors and market timers may be disappointed because it often underperforms the benchmark in bullish trends. Here’s how it can work.

Using an index on the short side makes a market neutral strategy safer

An equity market neutral portfolio usually holds balanced amounts of long and short positions in a stock universe. It can be a worldwide universe, a national index (for example the S&P 500), a sector or an industry (for example healthcare, biotechnology).

I am personally reluctant to sell short individual stocks.

If a market neutral approach is being used by a risk-averse investor, it is better to avoid risks that are not related to the market, like being trapped in a short squeeze. This risk exists in all market segments, even large companies.

‘If a market neutral approach is being used by a risk-averse investor, it is better to avoid risks that are not related to the market, like being trapped in a short squeeze. This risk exists in all market segments, even large companies’

In 2008 Volkswagen AG became briefly the highest capitalisation in the world. Its share price was multiplied by five in two days. Short sellers covered their positions with large losses, in panic or forced by margin calls.

Even absorbed in a diversified portfolio, such a shock hurts. I prefer to sell a benchmark index on the short side of a market neutral portfolio, so as to avoid this kind of event.

The long side of a market neutral portfolio aims to beat the market in all (or most) phases of the expansion-contraction cycle. Sector trends are linked to these phases, at least in theory. The reality is often more complicated.

Cycles on different time frames may be mixed and macro factors can freeze some sectors (like the oil price did for energy stocks in the second half of 2014). As a consequence, it may be difficult to apply the cycle theory and focus on the right sectors at the right time.

Sector diversification is a simple solution to keep drawdowns acceptable in depth and duration.

Example: the Russell 2000 ‘Lazy’ portfolio

The following simulation is based on a portfolio mixing all the Russell 2000 strategies of my book ‘The Lazy Fundamental Analyst’. There are nine strategies, one for each GICS sector except Telecommunication. Each strategy selects 20 companies using two fundamental factors.

‘Sector diversification makes the portfolio safer in irregular market cycles’

The result is an equal-weighted portfolio of 180 stocks. Of course, past performance, real or simulated, is not a guarantee of future returns. But with so many holdings, performance can hardly be suspected of being curve-fitted or random.

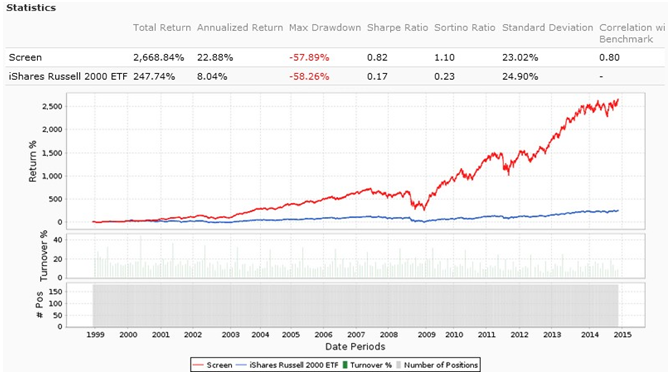

The chart shows a simulation of my 180-stock Russell 2000 ‘Lazy’ portfolio from 2 January 1999 to 5 January 2015 (16 years), rebalanced every four weeks.

Data and chart: Portfolio123

The following table gives statistics of the excess return over IWM (iShares Russell 2000 ETF) by four-week periods. It corresponds to a market neutral portfolio with the 180 stocks on the long side and IWM on the short side, with a leveraging factor of 2, without the margin and carry cost.

| Average 4week return | Average Annual return | Max Drawdown Depth | Max Drawdown Duration | Avg gain/ Avg loss | 4week gain probability | Kelly criterion |

| 1.04% | 14.4% | -23.7%* | 19 months | 1.54 | 68% | 0.48 |

* on rebalancing date, it may be deeper in real time.

On the same period the Russell 2000 ETF (with dividends reinvested) returned about 8% annualized with a drawdown of 42 months going below -58%.

There are solutions other than IWM for shorting the Russell 2000 index: futures, options, CFDs, leveraged ETFs, etc. Each of these has advantages, disadvantages and a cost.

Optimizing the strategy

Holding 180 stocks is a lot for an individual investor. The number can be reduced by a due diligence process or a quantitative method.

In my real portfolio and newsletter, I have excluded the most sensitive sectors to macroeconomic and geopolitical concerns, kept the focus on larger companies, and optimized the quantitative models to keep only 24 stocks.

Optimising quantitative models to a lower number of holdings incurs a risk of curve fitting. However, with 24 holdings balanced in cyclical and defensive stocks, the risk is quite low. The biggest danger of optimising is not over-rating the possible return, but under-rating the real risk. If the return can never be predicted, a diversified market neutral portfolio limits the risk by design.

The Lazy Fundamental Analyst’ is published by Harriman House.

Commentary » Exchange traded products Commentary » Exchange traded products Latest » Latest » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.