Oct

2023

How do different equity styles perform during an economic slowdown?

DIY Investor

27 October 2023

We examine which equity styles have performed best during slowdowns or recessions and explain why value stocks may continue to outperform – by Tina Fong

Lockdowns in China and the Russia-Ukraine war have meant that stagflation remains at the top of investors’ minds. Higher inflation has also forced central banks to react and start to rein in years of loose monetary policy. As interest rates rise across the key developed economies, the market has become increasingly worried about recession risks.

From an equity style perspective, how should investors position their portfolios in a slowdown or recessionary world?

Like stagflation, the slowdown phase is when economic activity is slowing, inflation is rising, and central banks are tightening policy. We find that the more defensive equity styles have been the winners. But unlike past slowdowns, the performance of value stocks has been unusually strong this time. Later we explain why this is.

By comparison, during recessions, policymakers are typically cutting interest rates in response to the slump in growth and inflation. As households and companies repair their balance sheets, investors start to anticipate a rebound in economic activity and corporate earnings. This leads to a rotation towards the more cyclical equity styles.

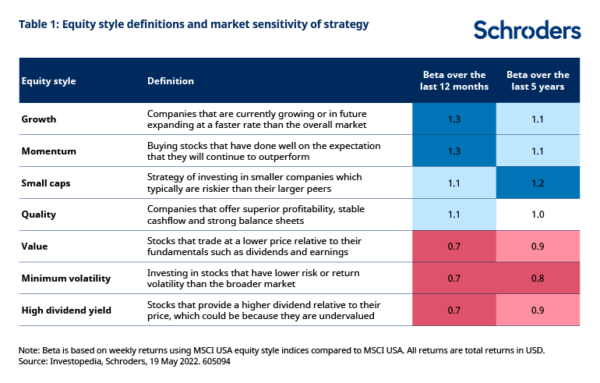

Equity style primer

Table 1 provides an overview of the different equity styles in our analysis. We show the beta to illustrate the sensitivity of the investment strategy towards the performance of the overall market. For instance, the more defensive equity styles have a beta of less than one and they tend to outperform when the market sells off.

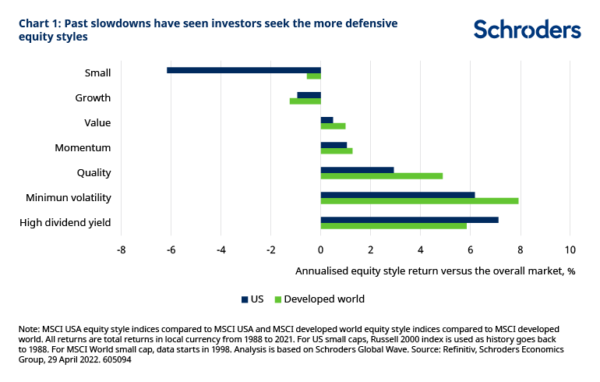

Which equity styles have tended to do well during slowdowns?

Historically, the more defensive equity styles have outperformed their more cyclical peers (chart 1). On average, the style winners have been high dividend yield and minimum volatility strategies. It appears that investors have sought shelter from stocks that are better at weathering the challenges of weaker economic growth and accelerating inflation.

Instead, small caps are the laggards during slowdowns, as these companies have less pricing power than large caps. So they particularly feel the squeeze on profit margins from higher costs.

Meanwhile, value stocks have tended to perform slightly better than their growth counterparts. But the return profiles of these two styles have not been very different during slowdowns.

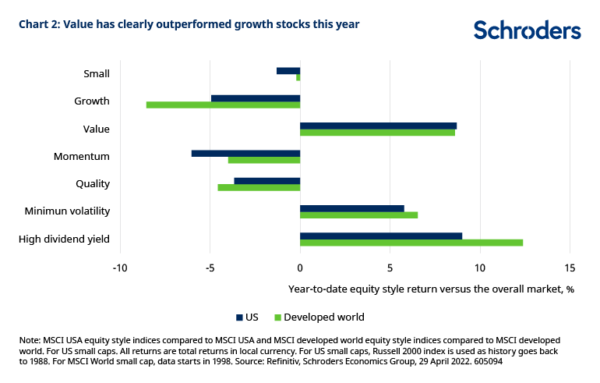

But the performance of value has been different this time

So far this year, both high dividend yield and minimum volatility styles have experienced strong gains which is consistent with previous slowdowns (chart 2). But unlike past slowdown periods, the divergence between the performance of growth versus value stocks has been stark. In fact, the excess returns from investing in value versus growth this year has been the third highest since the mid-1970s.

This has been driven by two key factors. First, the stellar returns of energy stocks have certainly helped as they tend to be classified in the value bucket. Second, in contrast to past slowdowns when bond yields have been falling, Treasury yields have been rising this time. The surge in US government bond yields has hit the growth areas of the market, such as tech, which are more sensitive to rising borrowing costs. This is because these companies generate a large proportion of their earnings in the future, so these future cash flows are being discounted at a higher rate.

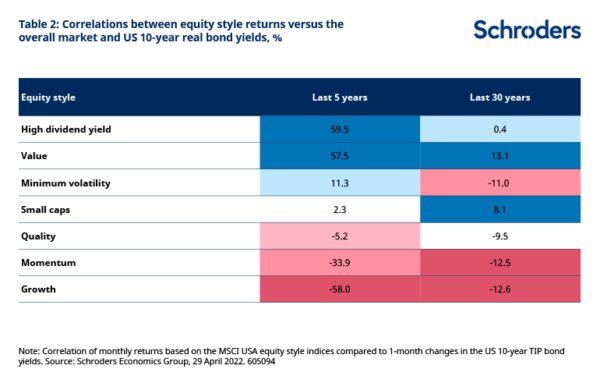

Table 2 shows that the growth style is the most negatively correlated with US real bond yields (measured using 10-year inflation protected Treasury or TIP bonds) over the last five years. Similarly, both momentum and quality stocks have underperformed along with rising bond yields. Over the same period, value has been one of the equity styles most positively correlated with higher yields.

That said, the composition of these equity styles are not constant through time, and so the characteristics and drivers will change. For instance, the negative correlation between growth stocks and real yields have been stronger over the last five years compared to the past 30 years. This is because of the current dominance of technology stocks in the growth bucket, which are more sensitive to higher rates.

Looking ahead, assuming recent history is repeated, if real yields continue to rise, value stocks could continue to outperform relative to growth in this environment.

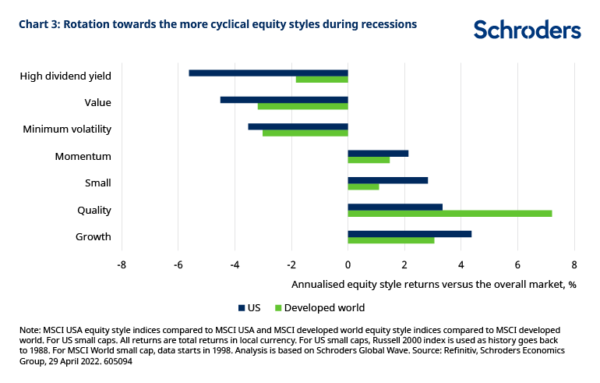

What does recession mean for the equity style investing?

While quality stocks continue to do well during recessions, there is a noticable reversal in style leadership towards the more cyclical equity styles (chart 3). Growth stocks have generally regained their spark during recessions. This is because the value of these companies are boosted by the fall in interest rates and bond yields as central banks respond to the collapse in economic growth.

Meanwhile, small caps have tended to beat their larger peers as investors start to discount the recovery in corporate profitability of these companies. Relative to large caps, they are also more likely to benefit from looser monetary policy.

Overall, lessons from past slowdowns have shown that investors should seek shelter in the more defensive equity styles. While this is likely to be repeated, the difference this time is value stocks could continue to outperform their growth peers if bond yields continue to rise. If at some point the world does go into a recession and bond yields fall, our analysis suggests that growth stocks and the more cyclical styles could start to do well again.

![]()

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

Commentary » Equities » Equities Commentary » Equities Latest » Investment trusts Commentary » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.