Jul

2019

Half year report from IT Investor as markets hit all time highs

DIY Investor

5 July 2019

![]()

Stock markets never fail to surprise. The heavy fall at the end of 2018 seems to be long-forgotten, and global markets have been making all-time highs again.

In pound terms, they rose 16.5% over the first six months of the year (and a further 3% in the first three days of July).

The weak pound has been a big driver of returns for sterling-based investors in recent years, but it didn’t have much of an impact in this case. The pound was down about 0.5% against both the US dollar and the euro.

‘global markets have been making all-time highs again’

Global bonds and gilts have also done pretty well, both up some 5%. Even Bitcoin and gold have bounced back in recent weeks, not that they’re my cup of tea.

Against this backdrop of pretty much everything going up, we have the Neil Woodford fiasco.

I must admit that I’m surprised that the daily pricing of his main fund is showing a drop of just 5% since the end of May compared to the nearly 30% fall in the share price of Woodford Patient Capital Trust.

Who knows how this particular tale of woe will end? I suspect we will only be a tiny bit wiser come the end of 2019.

In the wider world of investment trusts…

The average discount on investment trusts has shrunk a little over the last six months, from 4.3% to 3.6%. That’s not surprising when markets have been on such a tear. Gearing levels have reduced a little, from 9.2% to 8.6%.

We have seen a sector revamp by the AIC, which looks pretty sensible in the main, tidying up a lot of square pegs that found themselves in round holes.

There were five debutants. In size order:

- Schiehallion (Baillie Gifford’s dedicated unicorn investment vehicle)

- US Solar Fund (another renewable trust)

- Aquila European Renewables Income (and another)

- Riverstone Credit Opportunities (lending money to the energy sector)

- Cameron Investors (looking to mop up small funds that have lost their way)

On the name change front, two more F&C funds were rebranded under the BMO moniker, leaving F&C Investment Trust as the last company to carry that particular flag (although its name was changed from Foreign & Colonial to just F&C at the end of 2018).

And crusty old British Empire Securities became the sleek-sounding AVI Global.

Share splits seem to be back in fashion, with HGCapital performing a 10 for 1, and Witan, Edinburgh Worldwide and North American Income doing 5 for 1s.

The Woodford saga has also stirred up the log-running saga over what’s the best investment vehicle, especially when it comes to illiquid assets.

‘we still have an almighty muddle concerning how investment trust costs are calculated’

I suspect we could end up seeing a little more demand for investment trusts as a result of all this, which might not be that helpful for those us looking to snap up a bargain!

Talking of fund managers setting up their own shops, Alexander Darwell of Jupiter European Opportunities has just announced he is doing just that.

There is a good piece by Gavin Lumsden on Citywire on why this doesn’t look to be Woodford Mark 2. The new firm is to be called Devon Equity Management, so at least Darwell is avoiding the hubris of naming the firm after himself.

On the disclosure front, we still have an almighty muddle concerning how investment trust costs are calculated. I am hoping we see some progress on that front by the end of 2019, although I suspect the FCA’s attention is mostly on the Woodford fallout right now.

My portfolio: bye-bye City of London

In April, as I mentioned I might in my first-quarter review, I started a position in Gresham House Energy Storage Fund and added to Princess Private Equity in my ISA.

Last week, I decided it was time to bail out of City of London Investment Trust. I hadn’t held it for that long by my standards (a couple of years). Its heavy weighting towards oil and banking stocks had been making me a little queasy, though, for ethical and financial reasons.

‘No doubt this will mark a turning point for the UK stock market, which will now surge ahead after a long period of underperformance’

These were all positions it held when I first bought, of course, so this was a queasiness entirely of my own making.

City of London does hold a number of decent UK stocks, albeit ones I already have plenty of exposure to elsewhere. It also has that stellar record of consecutive dividend increases (52 so far and 53 in the bag) and commendably low costs of around 0.4%.

It was my sole mainstream UK fund and as I did some basic prep work for an article about it, I was finding little reason to keep holding on.

No doubt this will mark a turning point for the UK stock market, which will now surge ahead after a long period of underperformance.

If that’s the case, then you’re welcome!

Reinvesting the proceeds

I did have a vague plan to reinvest City of London into a few tech and biotech funds, but I feel the need to do a little more research here before taking the plunge.

Instead, I’ve bought some more HICL Infrastructure, Gresham Energy Storage, JPMorgan Global Growth & Income, Murray International, Acorn Income, and Henderson Smaller Companies. In short, I’ve smudged the funds over a number of positions that I was building up.

‘In some cases, there was the added bonus of the discount situation looking relatively attractive’

In some cases, there was the added bonus of the discount situation looking relatively attractive.

For example, HICL is trading around net asset value, which is unusual for an infrastructure fund. Similarly, Murray International has slipped to a rare discount in recent weeks, tempting me into a further nibble.

Acorn and Henderson are both on discounts of around 10%, which isn’t that unusual for UK small-cap investment trusts. However, that was why I bought them but not BlackRock Smaller Companies, where the discount has shrunk significantly despite the departure of Mike Prentis.

The JPMorgan purchase is probably the hardest to defend, given I recently wrote that I was little concerned about the change of manager there and wanted to see how things progressed. But all these top-ups were relatively small in size, so I don’t feel too naughty about that.

Ideally, I would have liked to buy some more Bluefield Solar, but the premium has gotten a little too high for a new purchase right now. I might return for a further nibble should the situation become more favourable.

My performance so far in 2019

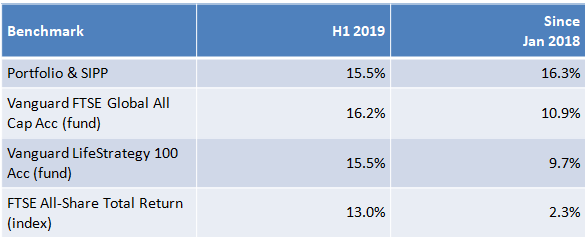

I recently wrote about tweaking some of the benchmarks I use to measure my portfolio. I’ve settled on three that should be easy to get numbers for, are based in pounds, and that include re-invested dividends:

- Vanguard FTSE Global All Cap — a newish global tracker with an ongoing charges ratio of 0.24%.

- LifeStrategy 100 — another global tracker, with charges of 0.22%, that has a higher UK weighting that better reflects the geographic make-up of my portfolio.

- FTSE All-Share — for old times sake. I suppose for consistency this should really be a UK tracker fund.

Here’s how I’ve done these last six months and since I started to unitise my returns at the start of 2018:

I’ve combined my portfolio (ISA and dealing accounts) and SIPP into one figure, to avoid things getting too messy with loads of different numbers.

I’m more than happy with 15.5% despite the fact it’s lagging the global tracker a little and matching LifeStrategy 100. It would be a great annual performance with inflation running at 2% or so, let alone a great six-month number.

‘I’ve maintained the lead I had over global markets since the start of 2018’

I’ve maintained the lead I had over global markets since the start of 2018. Pleasing, but it’s just eighteen months so not especially meaningful.

Given the make-up of my portfolio, I suspect I might do a little better when markets are struggling but broadly keep up when they roar ahead. Let’s see if that continues to be the case.

UK markets lagged behind again. It seems a little churlish to sneer at a 13% six-month return, yet the UK fell harder than global markets did in 2018 and still didn’t bounce back as strongly.

Stars and dogs

A number of funds have done me proud with returns between 20% and 25% over the last half-year.

Fundsmith, HG Capital, BlackRock Smaller Companies, JPMorgan Global Growth & Income, Lindsell Train Global, and Smithson all fall into that camp.

Relative laggards were Murray International, HICL Infrastructure, and Gresham House Energy Storage. These all had positive returns but less than 5%. Murray is the largest of those three for me, but it held its ground during the second half of 2018.

My turnip award goes to Baronsmead Venture Trust. It’s the lone holding in these red these past six months with a 3% loss.

Baronsmead’s net asset value hasn’t recovered in step with global markets this year, partly due to problems at Staffline, one of its (formerly) largest holdings. Staffline accounted for over 5% of net assets at the end of 2018 but its share price has collapsed by over 90% since.

‘There are new VCT rules which restrict the range of companies that can be invested in’

I’ve held this Baronsmead fund for fourteen years now. With the exception of the financial crisis, when everything plummeted, it’s the first time I can remember it struggling like this.

There are new VCT rules which restrict the range of companies that can be invested in, and concerns that there is a lot more VCT moneychasing what’s now a much smaller pool of possible investments. And there’s also been a change of ownership for the firm running the trust. But I don’t think either of these has had time to cause the recent underperformance at Baronsmead.

It’s a position that needs a bit more monitoring than before. You have to hold VCTs for five years to keep your initial tax relief. So that complicates matters a little should I decide to sell.

The one-year mark

It’s a year since I started this blog, and it’s been amazing to see the traffic grow. Special thanks to Monevator, DIY Investor (UK), and DIY Investor for linking to my site and helping to raise its profile.

I’m still finding plenty to write about, but time seems to be in short supply. I expect the summer holidays will curtail my output, as they did in 2018.

My general aim is to keep doing roughly one article a week for at least another year before taking stock a little. I managed 62 articles over the first year, with at least 4 every month except for August.

What next?

I now have 18 holdings in all, comprising 14 investment trusts, 2 funds, 1 ETF, and 1 share. That’s a manageable number for me, and probably there’s room for a couple more holdings without spreading myself too thinly.

I’ve been pondering what to do with City of London for a little while, so it feels good to bite the bullet on that one. Could Baronsmead become the next problem child in my portfolio? There always seems to be one!

I’d still like to add to my holdings in renewables, plus some technology and biotech/healthcare, but I expect this to happen relatively slowly. The high premiums on renewable trusts are holding me back a little right now, as is the fact this sector has seen a rash of new issues and large fundraisings in recent months.

Let’s see what the second half of 2019 throws our way.

Note that I may own some of the investments mentioned in this article. You can see my current holdings on my portfolio page. Nothing in this article should be regarded as a buy or sell recommendation as this site is not authorised to give financial advice and I’m just a person writing a blog. Always do your own research!

To subscribe visit:

![]()

Leave a Reply

You must be logged in to post a comment.