Oct

2020

Global perspectives – Cyclicals recovery building a head of steam

DIY Investor

8 October 2020

![]()

The headlines may be full of rising coronavirus infection rates but the stock market and world economy appear to be moving in a different direction.

Global bond yields are threatening to break out to the upside of the trading ranges prevailing during the summer, while economic surprise indices remain firmly in positive territory.

Crucially for short-term market direction, earnings estimates across the globe are now rising on a weighted basis.

The re-introduction of social restrictions during the winter remains a concern as across Europe governments are dealing with an accelerating number of coronavirus infections.

Nevertheless, a vaccine for 2021 is within sight. We remain neutral on equities overall but believe global markets are likely to continue to trend higher as COVID-19 shrinks back to being a healthcare question rather than an economic problem over the coming 12m.

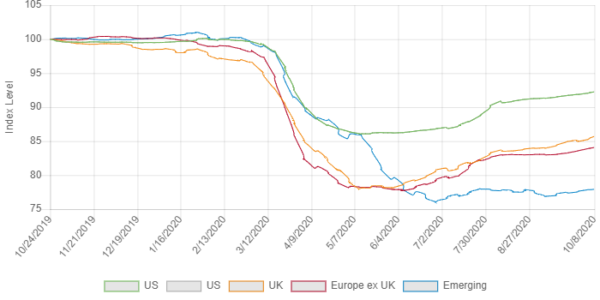

Exhibit 1: Global earnings estimates remain on improving trend

Source: Refinitiv, Edison calculations, weighted data.

Rising infection rates spooked investors during September but national economies have not been shut down as a result.

Thankfully, it is now possible to shut down the riskiest activities or implement regional lockdowns to control infections rather than restricting much larger swathes of economic activity.

Investors have not been slow to recognise this and analysts’ earnings forecasts for 2020 are now on a recovery trajectory following the very large downgrades recorded during Q1 and Q2.

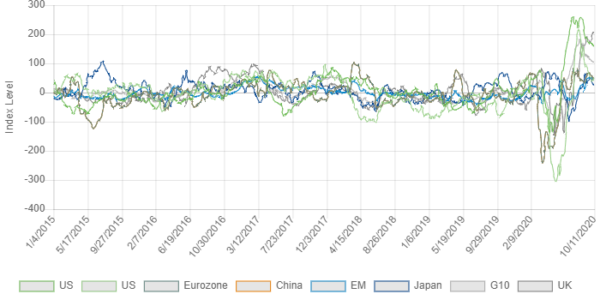

This improving outlook for the corporate sector has additional and legitimate confirmation, in our view, from global economic surprise indices.

These indices indicate the extent to which recent economic data has been ahead or behind of consensus forecasts. Surprise indices have stayed positive into the autumn despite initial fears that the recovery observed post-lockdown would prove to be short-lived.

Exhibit 2: Economic surprise indices still firmly positive

Source: Refinitiv

Furthermore, despite the recent increases in coronavirus infections, global government bond investors also appear to be discounting an improvement in economic activity as yields tentatively nudge the highs of the very low trading range established post-pandemic.

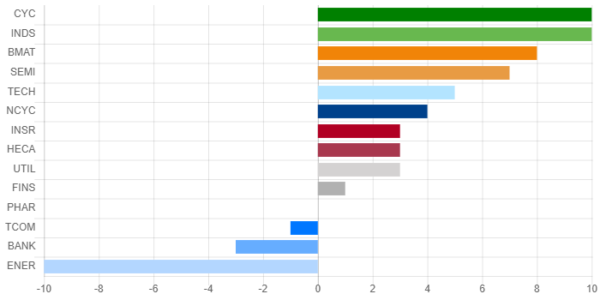

Finally, on a global basis, cyclical and industrial stocks have over the last 3 months been the strongest performers, rather than the global technology sector.

Exhibit 3: Global cyclicals and industrials now 3-month market leaders

Source: Refinitiv, price returns shown in USD.

At this point in the pandemic we are of the view that the trend is the investor’s friend. Investors must now look forward to 2021 and beyond which may include a period of continuing social restrictions but from around Q221 the prospect of an increasing availability of vaccines.

Vaccine approvals are in our view likely following the data submissions currently being filed with regulators, around the start of 2021.

From an economic perspective, given pre-existing infection rates, vaccines will offer a substantial boost to herd immunity even if they are not ubiquitously administered.

We continue to believe European equities are now of increasing interest because of the lag in performance compared to the US and the extended period of very loose monetary policy which lies ahead.

Brexit negotiations remain a risk but as with the withdrawal agreement some of the feared disruptive outcomes are in reality of lower probability than implied by their coverage in the media.

As investors look ahead, we believe it is also time to consider carefully the mainstreaming of the environmental sector. Low interest rates magnify and bring into sharp relief long-dated risks and opportunities.

By 2035, a significant proportion of the world’s auto markets will have banned the sale of internal combustion vehicles, reducing demand for transportation fuels. In terms of risks, we note the fossil fuel energy sector is struggling to perform even as other cyclical sectors rebound with hopes of recovery, Exhibit 3.

With a significant proportion of government coronavirus stimulus packages centred around the greening of national economies, it is in our view time for mainstream investors to actively engage with environmental trends rather than regard them as merely a portfolio risk to be avoided.

The environmental sector is forecast to grow rapidly over the next 15 years as the global economy de-carbonises and moves towards increased sustainability on a variety of climate change, environmental pollution and biodiversity metrics.

Recently, the ECB has suggested adjusting asset purchasing policy to steer economic activity towards green objectives, which only a few years earlier would have been a very controversial step regarded as outside its remit.

We believe investors now starved of yield from government bonds may consider rotating towards lower-risk green investments to generate a replacement income, even if few securities can match the defensive character of government bonds in a crisis.

Click to visit:

![]()

Commentary » Equities » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.