Jul

2021

Global equities: Volatility rises at the upper reaches of valuation

DIY Investor

24 July 2021

Despite the arrival of ‘freedom day’ in the UK and the strength of other developed market economic recoveries, global equity market progress has been relatively muted in recent months.

Despite the arrival of ‘freedom day’ in the UK and the strength of other developed market economic recoveries, global equity market progress has been relatively muted in recent months.

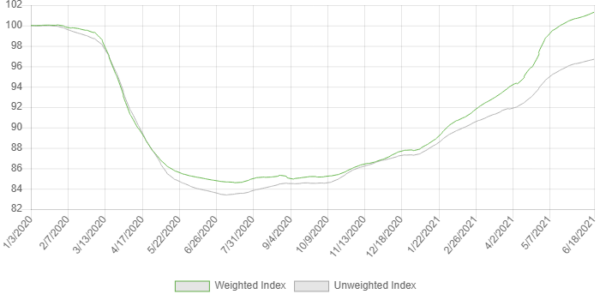

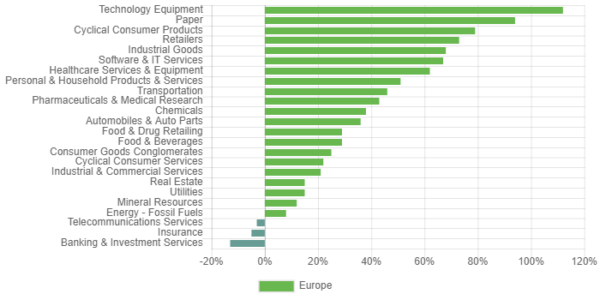

More recently, in the last week equities have slid from highs and bond yields have fallen. Yet global sectors are still trading at historically high valuations. Investors seem to have become shy of chasing equities higher, absent actual delivery of promised profits growth for 2021 and beyond.

For the UK, ‘freedom day’ is increasingly looking like business as COVID-usual in terms of restrictions on physical mobility, with reports of 500,000 English residents per week placed under NHS contact tracing self-isolation.

We believe investors are aware of their limited investment choices at present. Low bond yields, low corporate credit spreads and the anticipation of an extended period of accommodative monetary policy into 2022 are in our view the primary driver of relatively high equity valuations – and it is not necessarily irrational.

Should profits forecasts match expectations, markets could trade sideways as earnings catch up over time. Low interest rates and rapid profits growth have been the basis for our neutral view on equities during 2021.

On the other hand the scope for a correction in equity prices is clearly present given that global equities are trading close to a 15y-record forward price/book multiple. On balance, risks to the outlook are increasing. Investors are having to digest higher than expected inflation, slowing economic growth (even if consensus forecasts are still rising modestly) and the rapidly spreading delta covid variant.

Click to visit:

![]()

Leave a Reply

You must be logged in to post a comment.