Oct

2021

Getting ahead of COP26 and what it means for investors

DIY Investor

31 October 2021

This November sees the UK play host to COP26 – the 26th Conference of Parties – where global leaders from almost 200 nations will come together and discuss climate objectives and, more importantly, revisit the commitments made as part of the 2015 Paris Agreement.

This November sees the UK play host to COP26 – the 26th Conference of Parties – where global leaders from almost 200 nations will come together and discuss climate objectives and, more importantly, revisit the commitments made as part of the 2015 Paris Agreement.

The parties are likely to agree that efforts will need to be meaningfully increased to ensure that achieving net zero by 2050 is within reach. In the coming years, investors can expect a raft of policy changes, with governments increasingly targeting public spending on infrastructure. Corporates are likely to face higher costs as a result of broader adoption of carbon pricing systems, but may find that capital markets reward them for focusing future investment spending on climate-related projects. Companies that can get ahead of the impending change and work with governments to achieve their goals may benefit from first-mover advantage. We discuss the technology and policy developments required to reach net zero in more detail in our paper, “Achieving net zero: The path to a carbon neutral world.”

More ambition required on the path to net zero

The main aims of the Paris Agreement were to keep global temperatures from warming above 1.5 degrees Celsius and effectively reach net zero greenhouse gas emissions by 2050. Countries were asked to submit their own emission reduction targets in the form of NDCs (Nationally Determined Contributions) and review them every five years. Importantly, COP26 is the first meeting of global leaders since the end of the first fiveyear period. We now know that the proposals set out in 2015 are not sufficient to meet the target of restricting global warming to 1.5 degrees.

Just over 110 parties – accounting for around half of global emissions – have submitted new NDCs, but the United Nations (UN) has judged that these proposals still fall well short of the degree of change required to meet the 1.5 degree target. The UN estimates that current national plans will lead global emissions in 2030 to be around 16% above 2010 levels. In order to be consistent with the 1.5 degree target, 2030 emissions need to be below 2010 levels by 45%. With progress wide of the mark, the current proposals and potential improvements are expected to form a significant part of discussions at COP26.

The US, UK and European Union are all among those to have submitted new plans to reach net zero by 2050. The US has pledged to cut net carbon emissions in half by 2030 (relative to emissions in 2005), while the EU plans to reduce its emissions by 55% by 2030, relative to 1990. The UK has one of the most ambitious plans, aiming to cut emissions by 68% by 2030 (relative to emissions in 1990), but is responsible for less than 1% of total global greenhouse gas emissions. In fact, these three developed nations make up just 25% of global carbon emissions, which only makes clearer the need for global coordination.

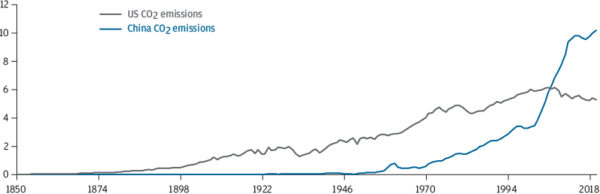

Herein lies the challenge at this conference. A significant number of countries have still not submitted an update of their emission reduction targets. COP26 can only be deemed a success if all countries – including those with the highest emissions – decide to increase ambitions when they update their targets for the next decade. China has not updated its NDC but has stated its intention to reach peak carbon emissions by 2030 and net zero by 2060 – a pledge that does not go far enough for a country that is responsible for the largest amount of global carbon emissions. Undoubtedly, China will argue that the onus should be placed on developed countries, which initiated the industrial revolution, have a longer history of emissions and have the financial means to cut down on them (Exhibit 1). With China’s attendance at COP26 still in doubt, the potential for climate disputes to catalyse geopolitical tensions is increasingly clear.

Exhibit 1: US and China CO2 emissions over time

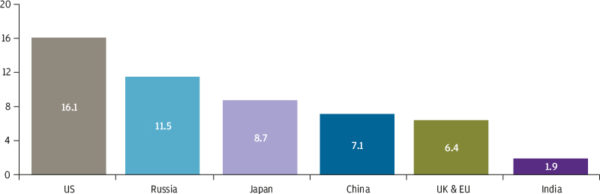

The metrics used to measure emissions make a huge difference: on a per capita basis, the US has a greater level of emissions than China (Exhibit 2). It is also worth noting that around 14% of China’s carbon emissions are attributable to goods that are exported and consumed abroad, which underlines the major role that recipients of China’s exports have to play in helping China to reduce its emissions. Another key expectation from COP26 will be for developed countries to make good on their promise to deliver at least USD 100 billion in finance per year to support developing countries in their climate goals. OECD data suggests that around USD 80 billion was mobilised in 2018. Commitments to increase this support will perhaps encourage some of the important developing nations to step up their carbon-reduction initiatives.

Exhibit 2: Global CO2 emissions per capita

Considerations for investors

Investors should be prepared for climate-related headlines in the coming weeks, as COP26 acts as a catalyst for governments and corporates to make new, more ambitious commitments. We expect this to impact financial markets in multiple ways.

Green bond issuance set to grow

Green infrastructure spending will be a major focus for governments that are under pressure to demonstrate their climate credentials to an increasingly green electorate. There are already several examples. The Biden administration’s USD 2.3 trillion American Jobs Plan includes multiple spending measures aimed at clean energy technology and the transition to electric vehicles. It is a similar story across the Atlantic, with the UK government’s Ten Point Plan for a Green Industrial Revolution aiming to generate 250,000 green jobs. In Europe, at least 30% of spending in the EU’s EUR 750 billion recovery fund must have climate-related benefits. Yet with more than USD 13 trillion of global investment in electricity systems alone estimated to be required by 2050 if net zero targets are to be reached, the scale of the challenge is clear.

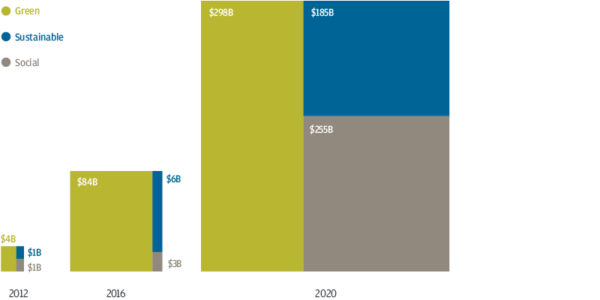

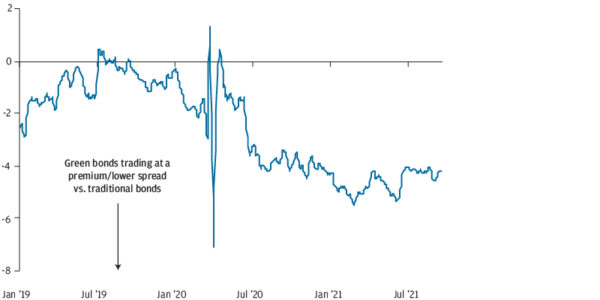

A rise in green bond issuance will be the key means by which governments will fund new climate-focused spending. The European Investment Bank became the first issuer of green bonds – for which proceeds are earmarked for environmentally friendly outcomes – back in 2007, and both governments and corporates have flocked to the sustainable bond market since, with green, social and sustainable bond issuance growing from just USD 6 billion in 2012 to over USD 700 billion last year. The popularity of the market is unsurprising given that strong demand for this debt often leads to lower borrowing costs for the issuer – a dynamic known as the green premium, or “greenium” (Exhibit 3). Despite this benefit, the US government remains a notable absentee from the green bond market. While officials have so far been reluctant to discuss this idea publicly, the emergence of a “Green Treasury” appears increasingly inevitable.

Exhibit 3a: Global sustainable, social and green bond issuance

Private capital encouraged to be part of the solution

An acceleration in government spending is one piece of the puzzle, but we also expect to see further measures aimed at incentivising private capital to be part of the solution. Strengthened regulation that pressures large investors to tilt portfolios towards climate-friendly strategies is one way to achieve this outcome. Another route is for governments to co-invest alongside the private sector in public-private partnership models. This type of structure can often be used to ensure that initiatives that would be too risky for the private sector to invest in alone can still access the financing they require.

Corporate announcements to demonstrate the leaders and laggards

In the face of increasing investor scrutiny, the corporate sector is unlikely to wait for regulation to force its hand on tackling climate change. The number of companies signing up to science-based target commitments had already surpassed last year’s record by June of this year, and November’s summit will intensify pressure on corporations that are not yet on board. Those that are able to align with government goals will benefit from government spending and be rewarded with access to easier finance through capital markets. Central banks are likely to incorporate green bonds or tilt their corporate asset purchases towards companies that are making investments consistent with net zero, meaning these companies will likely benefit from relatively lower borrowing costs. Additionally, investors may find comfort in owning the bonds of these firms, particularly in more stressful market environments, in the knowledge that the central bank is likely to be a willing buyer.

In industries such as energy, logistics, airlines and farming that are typically carbon intensive, there are also reasons to be optimistic. Those that adopt policies that help reach net zero will likely gain market share and be viewed as part of the solution, rather than the problem. Whatever the industry under consideration, investors may find opportunities by identifying companies that are better prepared for the transition.

Carbon pricing likely to impact corporate profits

Reaching agreement on a global carbon pricing system will be one of the most challenging issues of the summit. We cover how such a system could work in our paper, “The implications of carbon pricing initiatives for investors.” While some regions, such as Europe, have already made substantial progress, firms will remain incentivised to outsource production to other regions with lower carbon costs until a global solution is reached. Without a global solution, regions that decide to go it alone also risk imposing a competitive disadvantage on the profit margins of their domestic corporations. The risk of disagreements on carbon pricing spilling over into broader international relations is clear, with Europe perhaps needing to introduce a carbon border tax if other countries decide not to adopt a carbon pricing system. Without substantial progress, the path to net zero looks worryingly steep.

Conclusion

Investors should be braced for a wave of new climate ambitions stemming from November’s COP26 summit. With the conference serving to shine a spotlight on the enormous challenge presented by the need to reach net zero by 2050, both the public and private sectors will be keen to stress the extent of their ambitions, with potentially market-moving implications. For investors, there are risks and opportunities across sectors. Companies that prove they can be a part of the solution will likely benefit from a lower cost of financing in the years to come, as both governments and the private sector look to tilt their spending towards green initiatives. For businesses that are poorly prepared for the climate transition – regardless of sector – life will only get tougher.

The Market Insights program provides comprehensive data and commentary on global markets without reference to products. Designed as a tool to help clients understand the markets and support investment decision-making, the program explores the implications of current economic data and changing market conditions.

For the purposes of MiFID II, the JPM Market Insights and Portfolio Insights programs are marketing communications and are not in scope for any MiFID II / MiFIR requirements specifically related to investment research. Furthermore, the J.P. Morgan Asset Management Market Insights and Portfolio Insights programs, as non-independent research, have not been prepared in accordance with legal requirements designed to promote the independence of investment research, nor are they subject to any prohibition on dealing ahead of the dissemination of investment research. This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not a reliable indicator of current and future results. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities: In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be.; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). For all other markets in APAC, to intended recipients only. For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance. Copyright 2021 JPMorgan Chase & Co. All rights reserved.

Commentary » Investment trusts Commentary » Mutual funds Commentary » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.