Mar

2023

Focus on Funds: Fundsmith Equity vs. Lindsell Train Global

DIY Investor

18 March 2023

![]()

One of my dirty little secrets is that I don’t exclusively hold investment trusts. My SIPP includes two open-ended funds that are extremely popular with many investors: Fundsmith Equity and Lindsell Train Global.

In many aspects, these funds are very similar. However, I thought it would be useful to pitch them against each other to double check my rationale for holding both.

Why I hold these funds

Neither fund has an exact investment trust equivalent, but I like the investing style they employ. Their managers are widely regarded to be among the best that the UK fund management industry has to offer — although such accolades often prove to be a curse.

I first came across Terry Smith when he wrote “Accounting For Growth” in the early 1990s, exposing the tricks companies used to flatter their figures. He went on run Collins Stewart, which later became Tullett Prebon, before he set up Fundsmith in 2010.

Fundsmith runs two investment trusts, Fundsmith Emerging Equities and Smithson, the latter of which I also hold, but Fundsmith Equity is its oldest and largest fund.

Michael Lindsell and Nick Train worked together at GT Global, a fund management operation owned by the royal family of Liechtenstein, in the 1990s. GT merged with Invesco in 1998 and the two of them set up their own fund management operation, Lindsell Train Limited, shortly afterwards.

Lindsell Train Investment Trust was launched in January 2001 and it invests in many of the same companies that Lindsell Train Global does. However, nearly half its asset value is attributed to a 24% stake in Lindsell Train Limited (its staff own 3% and the two co-founders the remaining 73%).

Somewhat ironically, the value of this asset, and hence of the investment trust, has soared due to the success of Lindsell Train’s open-ended funds.

Despite its great performance over the last 18 years, Lindsell Train Investment Trust only has assets of £180m and demand for its limited number of shares have seen its premium soar to nearly 100%.

Nick Train also runs another investment trust, Finsbury Growth Trust. It’s done very well, too, but it is UK-focused.

Bull market funds?

Fundsmith Equity was set up in November 2010 and Lindsell Train Global in March 2011.

Despite being a long-term admirer, I’ve only held Lindsell Train for three years and Fundsmith Equity for a year and a bit.

Both funds could be considered children of the current bull market, which obviously raises concerns over how they might fare when things get choppier. But their managers have been around the block a few times.

Lindsell Train Investment Trust was up 1,078% in net asset terms from launch to 31 March 2019, compared to 172% for the MSCI World Index. In share price terms, it has risen 1,806% and it’s up a further 20% since then (at the time of writing, anyway) making its total share price return nearly 2,200%!

Smith’s previous track record is a little less public. He started as an analyst and then ran financial services businesses but he was the adviser to Tullett’s pension fund for seven years prior to Fundsmith’s launch. During that time, it produced annualised returns of 14% compared to the 6% annual rise in MSCI World, although I’m not sure if he followed the same approach as that used by Fundsmith Equity.

The two funds’ track records

From March 2011 to March 2019, Lindsell Train Global returned 288% versus 143% for MSCI World. On an annualised basis, that works out at 18.5% and 11.7%.

Starting a little earlier, Fundsmith Equity is up 325% compared to 151% for MSCI World, making it the slightly better performer at 18.8% annualised versus MSCI World’s 11.6%.

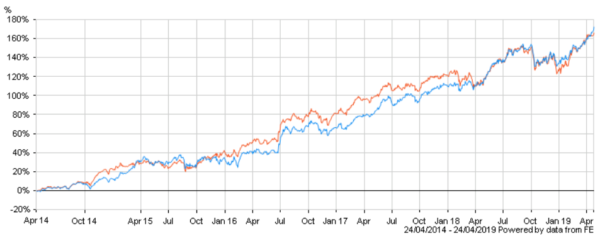

Over the last five years, there is also very little difference. Fundsmith, the orange line, opened up a little lead a few years ago, but Lindsell Train has reeled it back in and recently snuck ahead (172% versus 166%).

By way of comparison, Scottish Mortgage, the poster child for the investment trust industry, is up 178% in share price terms and 163% in net asset terms.

Number of holdings

Both funds have a concentrated approach when it comes to their portfolios. Fundsmith aims for 20-30 holdings while Lindsell Train Global targets 20-35.

At the moment, Fundsmith seems to have 27 holdings and Lindsell Train Global 26, although it’s difficult to get fully up to date information.

Lindsell Train Global publishes its full list of holdings every six months in its interim and final reports.

Fundsmith Equity lists out its full holdings in its long-form annual report but this appears to only be available to direct holders on request. Nevertheless, a few folks have stitched together a full list from its regular missives.

Top 10 holdings

The top 10 holdings for each fund are published monthly. Here they are as of 31 March 2019:

Intuit and Paypal appear in the top 10s for both funds, while Unilever, PepsiCo and Diageo also appear to be common holdings.

The 5 common holdings account for some 30% of Lindsell Train Global and almost 20% of Fundsmith Equity, partly explaining why their recent performance records are so similar. I must admit I wasn’t aware the overlap between these two was as great as that.

Lindsell Train Global publishes percentage figures for its top 10 holdings, with Unilever, Heineken, and Diageo currently around the 7.5%-8% mark and the remainder around 5% apiece.

Fundsmith Equity doesn’t put percentages on its monthly factsheet but Hargreaves Lansdown uses data from Funds Library (the latest of which is dated from September 2018) suggesting its top 10 positions typically range from 4% to 6%.

Fundsmith Equity’s other holdings

As posted by langley59 at Lemonfool and in no particular order:

- Automatic Data Processing

- Intercontinental Hotels

- Reckitt Benckiser

- PepsiCo

- IDEXX

- Unilever

- 3M

- Visa

- L’Oreal

- Kone

- Becton Dickinson

- Sage

- Intertek

- Johnson & Johnson

- Diageo

- Coloplast

- McCormick & Co

Lindsell Train Global’s other holdings

Taken from its 31 December 2018 report (the order is Japan, UK, Europe, US):

- Astellas Pharma

- Canon

- Ito En

- Japan Exchange Group

- Kao Corp

- Meiko Network Japan

- RELX

- Celtic

- Hargreaves Lansdown

- Pearson

- Juventus

- Brown-Forman

- eBay

- International Speedway

- Walt Disney

- World Wrestling Entertainment

Meiko Network and Celtic are very small positions (just 0.25% combined). International Speedway (currently being bid for) and Canon are also less than 1%.

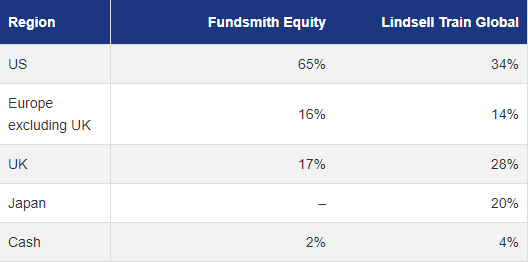

Geographic split

If you’re wary of the high valuation of the US stock market, then Fundsmith Equity’s 65% US weighting may give you the heebie-jeebies.

Both funds back a number of UK companies, though, and Lindsell Train also has an unusually high weighing in Japan (presumably because Michael Lindsell worked there for a number of years when he was at GT).

You’d need to look elsewhere for emerging market exposure it would seem.

Lindsell Train Global says it primarily invests in developed markets and Fundsmith Equity doesn’t seem to rule out emerging markets, so it looks like they are both keeping their options open, should the right opportunity arise.

Sector split

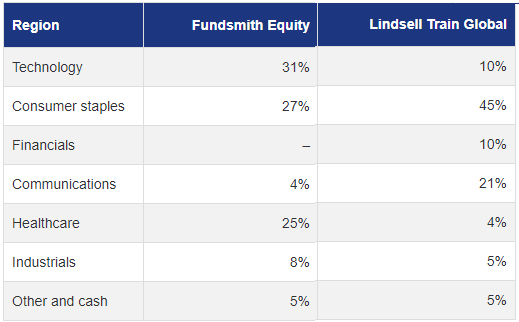

Although industry sectors can often be vague to the point of useless, you can see some significant divergence here as well.

Fundsmith Equity is much more technology focused, with the likes of Facebook, Sage, and Amadeus. It’s big on healthcare, too, so I think it’s fair to say it is the more forward-looking of the two portfolios.

Both funds like big consumer brands in food, drink and cosmetics, but Lindsell Train Global has much more of them.

Lindsell Train Global also favours big sporting brands, owning shares in two football clubs, World Wrestling Entertainment, and the owner of NASCAR/IndyCar. Lindsell Train also holds shares in Manchester United in its UK fund.

The 10% financials weighting in Lindsell Train Global seems to consist of Hargreaves Lansdown and the LSE (i.e. no banks or insurance firms), while communications includes RELX, Pearson and, I would assume, Disney and the WWE (i.e. no BT, Vodafone etc).

Neither fund manager takes much of an ethical stance, to my knowledge anyway, but their portfolios seem relatively ESG-friendly(although Philip Morris, a tobacco stock in Fundsmith’s top 10, might put some people off). I suspect that’s more because both managers prefer capital-light businesses.

Style and size

One difference I would highlight is that Fundsmith’s investment style seems to be more quantitative and methodical. Numerical analysis is at the fore in much of its literature and it specifies a wider group of companies that are in its ‘investable universe’.

Lindsell Train’s approach appears a little more qualitative, seeming to focus a little more on brands and competitive moats.

Size-wise, Fundsmith Equity is by far the larger of the two. It runs £18.6bn dwarfing the £6.8bn in Lindsell Train Global. If you add in their other funds, Fundsmith runs about £20bn and Lindsell Train around £15bn.

Certainly, there is a danger that Fundsmith Equity, in particular, could become so big that it becomes harder and harder for it to take meaningful positions in the companies it likes the best. That point seems to be a little way off yet, and the fact that neither fund tends to trade that much may help delay matters.

Nevertheless, as they continue to attract new investors, these funds will need to buy more and more of the companies they already hold, if they want to maintain their existing position sizes.

Ages and bench strength

Terry Smith is 66 in May. Nick Train turned 60 this month while Michael Lindsell is 60 next February.

None of this trio seems ready to down tools quite yet, but I guess Train and Lindsell may be around a little longer. Having two folks at the helm at Lindsell Train may reassure some people. Of the two, Nick Train is definitely the public face of the firm, with Lindsell keeping a much lower profile.

Smith is certainly never shy to voice an opinion, such as his recent bashing of Hargreaves Lansdown for the way it chooses funds for its Wealth 50 list. Lindsell Train Global is on that list and it has also been buying shares of Hargreaves Lansdown recently.

Although I’ve never seen Smith or Train mention each other in interviews, I would imagine they respect each other’s long-term/low-turnover approach to investing, despite their differing opinions of Hargreaves Lansdown!

Both firms derive their names from their founders, and it’s clear they have been crucial to their success so far. What happens when they depart is a concern.

Smith’s deputy on the investment side would seem to be Julian Robbins while Lindsell Train has recruited the more youthful James Bullock. This is a key area to watch over the next several years for me.

Skin in the game

A fair bit of guesswork is required here, but Smith looks to be well ahead.

Smith invested £25m when Fundsmith launched. Assuming he has left that alone, it’s worth just over £100m.

Train and Lindsell had around £1m and £4m respectively in Lindsell Train Global, according to the December 2018 annual report.

Charges

Things get a little murky here as open-ended funds have different classes which different charges depending on how you buy them.

The ongoing charges figure for my holding in Fundsmith Equity is 0.95% while Lindsell Train Equity is 0.51%.

It’s probably worth highlighting that Scottish Mortgage (just over £8bn of assets) is cheaper than both at 0.37%. Chalk one up for the investment trust industry!

Neck and neck

Picking between these two feels like being asked to select your favourite child.

I doubt either of these funds can continue to beat the market by such a wide margin as they have done in recent years. Seven percentage points a year is a big gap for funds of this size to maintain. But I’d still expect them to outperform global markets for a while yet.

There’s a lot of overlap between these funds due to their five common holdings. Elsewhere, though, there are big enough differences to make investing in both a sensible option. To my mind, their combined portfolios seem a little more balanced.

Find an excellent overview of Environmental, Social and Governance Investing here >

Note that I may own some of the investments mentioned in this article. You can see my current holdings on my portfolio page. Nothing in this article should be regarded as a buy or sell recommendation as this site is not authorised to give financial advice and I’m just a person writing a blog. Always do your own research!

Click to visit IT Investor, where you can subscribe to be notified when new posts are added:

![]()

Leave a Reply

You must be logged in to post a comment.