Feb

2022

Five Charts Showing the Attraction of Asian Equity Income

DIY Investor

21 February 2022

![]()

Asian shares offer a compelling proposition when it comes to investing for income.

By Richard Sennit, Fund Manager, Schroder AsiaPacific Fund and Schroder Oriental Income Fund

Interest rates may be on the rise but investors searching for higher income will still want to consider the merits of dividend-paying shares. Income investors often look to UK shares. However, Asian equities also hold significant attractions for income investors, and can help provide diversification.

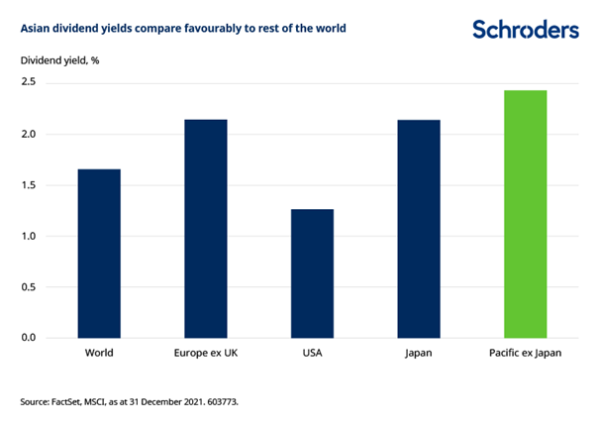

The chart below shows how dividend yields in the Pacific ex Japan region are above those on offer in other non UK markets, and comfortably ahead of regions like the US. The dividend yield is the dividend per share, divided by the price per share.

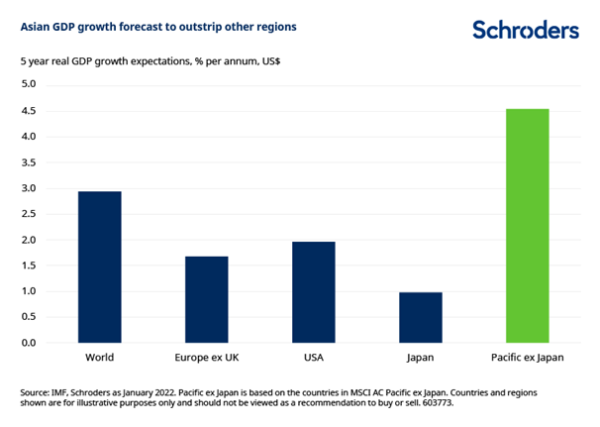

Added to their higher yields, Asian companies are operating in a region that is forecast to enjoy higher economic growth than other parts of the world over the next five years, as the next chart shows.

You may argue that overall GDP growth has little to do with investment returns. But as an income investor I’m looking for companies which are able to grow their income and dividends over time. Given the choice, I’d rather be doing that in an environment of higher economic growth than lower growth.

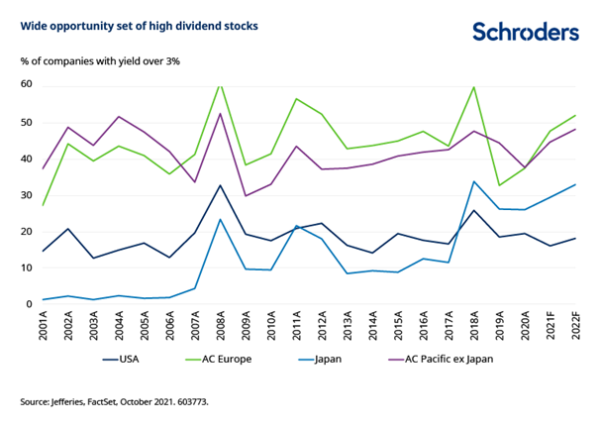

Then we come onto the opportunity set for income investors in Asia. The chart below shows the percentage of companies in different regions with a dividend yield above 3%.

As we can see, around 50% of companies in Pacific ex Japan and in Europe fulfil that criteria. By contrast, the percentages in the US and Japan are much smaller (around 33% and 18% respectively).

This is a fairly blunt measure but nevertheless demonstrates that income investors in Asia have a broad universe of companies to pick from.

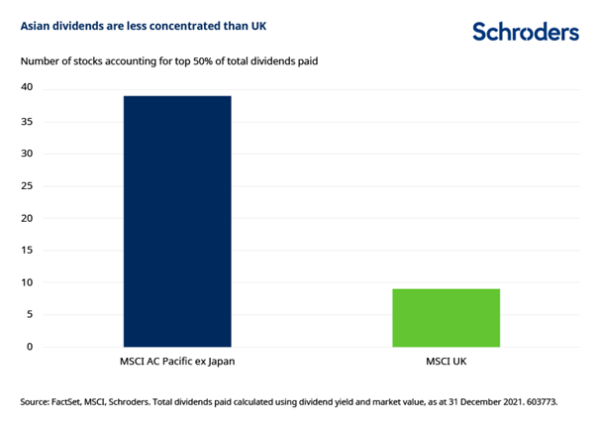

Next, dividends in Asia come from a relatively large number of companies, whereas in the UK they are much more highly concentrated in just a handful of stocks.

The chart below shows how fewer than 10 stocks make up 50% of the income from the MSCI UK index. By contrast, the corresponding figure for Asia is close to 50 stocks.

Again, this highlights the wider opportunity set that Asia offers for investors to choose from. This greater number of income payers making up 50% of the income also potentially makes Asia a more resilient source of income as it means investors are less reliant on any single company than they are in the UK.

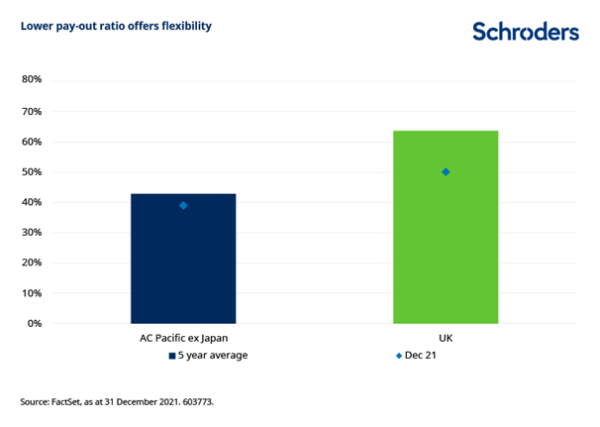

The final chart illustrates another key consideration for income investors: the resilience of company dividends. The chart below compares the dividend pay-out ratio of companies in the Asia ex Japan index compared to that of the UK index.

The pay-out ratio is the proportion of earnings paid as dividends, and as we can see this is lower in Asia than in the UK.

What this means is that if the economy slows and earnings become more volatile, Asian companies on average have a buffer.

We’ve seen over time in Asia that when earnings come under pressure, companies that have a lower pay-out ratio don’t necessarily have to cut their dividends. Instead, this buffer gives them the flexibility to allow pay-out ratios to rise until earnings have recovered.

A lower starting pay-out ratio also offers potential scope for future dividend growth.

Taken together, we think these charts show that Asian shares are an attractive proposition for income investors, offering both higher dividend yields than many other markets in combination with a wide set of opportunities.

To hear more from Schroders Investment Trusts, sign up to the newsletter.

More information on Schroder AsiaPacific Fund here >

More information on Schroder AsiaPacific Fund here >

Read the 25th anniversary booklet here >

More information on Schroder Oriental Income Fund here >

![]()

Click to watch the most recent AGM presentations

https://schroders.wistia.com/medias/cfctug2c6b?wvideo=cfctug2c6b

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Commentary » Equities » Equities Commentary » Equities Latest » Investment trusts Commentary » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.