Dec

2021

Fidelity European Trust PLC: Sam Morse shares his thoughts on the trust’s 30th anniversary

DIY Investor

8 December 2021

Sam Morse

Portfolio Manager, Fidelity European Trust PLC

To mark the 30th anniversary of the launch of the Fidelity European Trust PLC What Investment’s Editor-in-chief Lawrence Gosling spoke to the current lead portfolio manager Sam Morse.

Lawrence Gosling (LG): You’ve been managing the trust for the past 11 years and earlier in your career you were an analyst researching ideas for the portfolio. How has the investment landscape changed for European equities in the past three decades?

Sam Morse (SM): The big change for Europe in the past 30 years is the same for all investment markets, and certainly the UK, and that is globalisation.

In 1991, you were largely investing in companies that were exposed to domestic Europe and did all their business there.

Amazingly, I think less than 50% of the earnings and profits of European companies these days come from Europe.

The big multinational European companies, some of which have been regularly in the fund and have been very successful compounders, are businesses that are very much global in their nature, and probably to do less business in Europe than the index as a whole.

Investing in Europe really is about investing in companies not in the economy, which is a good thing because the European economy has been somewhat sluggish during this period.

LG: The trust has only had four portfolio managers in its 30-year history. There are not many football clubs who can point to that level of consistency.

SM: It started with Anthony Bolton, followed by Tim McCarron, Sudipto Banerji and then myself as lead manager since January 2011. I have two senior colleagues, Cristina Dondiuc, an investment director who leads our client servicing activities, and Marcel Stötzel, who is the co-portfolio manager.

We have all employed different stockpicking techniques, but with the same objective of finding good companies in Europe.

‘We have an incredible in-house research department with about 40 analysts covering Europe’

The other key element that has been consistent is the level of support we get from the Fidelity team of analysts. We have an incredible in-house research department with about 40 analysts covering Europe.

That wasn’t the case in 1991, although I’m proud to say I was one of the analysts who was looking at Europe at that time and I hope I made a small contribution in those early years.

I did a quick calculation based on average tenure and I reckon approaching 250 different analysts have contributed to this fund over that 30-year period I think that’s one of the key differentiators from other European investment trusts and what has led to the very attractive return.

LG: How would you describe your approach?

SM: My particular focus is on dividend growth and trying to identify attractively valued companies that will grow over time.

The one thing all the trust’s managers have had in common is a focus on stockpicking, rather than worrying about the macro or what will happen going forward in the European economy.

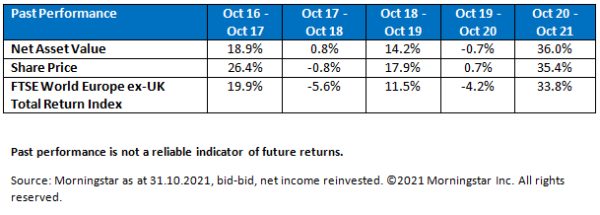

This is what has helped the Trust return 13.9% p.a. over that 30 year period (NAV return net of fees).

LG: How key are dividends?

SM: What is very important are the reinvested dividends. Hopefully, all the shareholders remember to reinvest dividends if they don’t need the regular income. This has meant a return of almost 50 times your money over the past 30 years.

I looked at this five years ago to coincide with the 25th anniversary of the trust. The reinvestment of dividends meant a return of almost 25 times your money at that point.

Since then we have doubled investors’ returns. That really shows both the power of stockpicking and of compounding. One of the great advantages of investment trusts that sometimes gets overlooked is their ability to gear. Certainly, the gearing level has varied over 30-year periods, depending on our confidence in the stocks.

‘This has meant a return of almost 50 times your money over the past 30 years’

The combination of that compounding stockpicking and gearing has meant that if you’re invested in the fund, net of fees you’ve made almost more than three times the amount of money than if you’d invested in the index over the same period.

This is quite staggering and ticks the box for active management, which, as active managers, we’re always very pleased about.

LG: How has Europe performed compared with some of the other major investment markets?

SM: It is perhaps a bit counterintuitive to look at the indices for the major stock markets.

Europe has pretty much matched the world stock market return despite the fact that many people tend to read gloomy headlines about how it’s rather sclerotic, but actually European companies have done pretty well.

I think what really drives the performance of an index is the performance of the companies and their real dividend growth.

Fidelity’s Peter Lynch had a lovely saying: ‘Nobody can predict interest rates, the future direction of the economy or the stock market. Dismiss all such forecasts and concentrate on what’s actually happening to the companies in which you’ve invested.’

I think this is very much a testament to our focus on stockpicking. The general view is that Europe hasn’t done as well as the world in the past 10 years or so, and that’s largely because of the big US tech names.

LG: When the trust first launched, innovation in the tech sector in Europe was one of its drivers. Is this still an attractive area or should investors look to the US?

SM: Technology has become an important part of the benchmark in Europe. It’s now a much larger component. Our weighting in tech is around 15% and we’re probably about 3% overweight compared with the index.

The tech companies in the US have done phenomenally, but that may change in the next 10 years.

We have one or two companies in the portfolio we think look of value relative to their US peers, German software firm SAP would be a case in point.

LG: Are you seeing pricing power that would allow companies to generate more cash, which they could pay back to investors in dividends?

SM: I think the pricing power is often very much a function of the company’s business and the strength of the franchise.

With most businesses I invest in, pricing power is something I really focus on. Although when inflation and interest rates rise, I tend to lose out on the valuation side because a lot of these ‘steady eddy’ businesses get hit on a valuation basis. On the flip side, their earnings are much more robust than many others.

Traditionally some companies haven’t had pricing power but now they do because of supply chain issues and the pandemic.

The autos sector has some pricing power currently, for example, but you know it’s going to end. I’m very much a long-term investor so what I’m looking for are companies that can grow their dividends on a three- to five-year view.

My question is about the sustainability of dividends.

LG: If someone is not currently invested in European equities why should they consider them now – and why this investment trust?

SM: I don’t have a huge amount of confidence in predicting what’s going to happen in terms of stock market directions or interest rates, etc. The pandemic has demonstrated that it’s foolish to believe we can predict what will happen.

I would rather build a robust portfolio of companies that have a good long-term track record in terms of earnings, sales, dividend growth and cashflow growth, where I feel strongly they will be able to continue that track record.

We’re not trying to shoot the lights out. Each and every year we’re just trying to add a little bit of extra performance relative to the benchmark.

The beauty of this approach is we don’t have too many sleepless nights worrying that the portfolio will go off the rails. We invest in decent companies with good track records that we are confident can help us outperform a little bit each year.

With the power of compounding that little bit of outperformance can deliver a very attractive return ahead of the benchmark over time.

Find out more about Fidelity European Trust PLC here >

Important information

The value of investments and the income from them can go down as well as up, so you may get back less than you invest. Investors should note that the views expressed may no longer be current and may have already been acted upon. Reference to specific securities should not be construed as a recommendation to buy or sell these securities and is included for the purposes of illustration only. Overseas investments will be affected by movements in currency exchange rates. This trust uses financial derivative instruments for investment purposes, which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The shares in the investment trust are listed on the London Stock Exchange and their price is affected by supply and demand. The investment trust can gain additional exposure to the market, known as gearing, potentially increasing volatility. This information is not a personal recommendation for any particular investment. If you are unsure about the suitability of an investment you should speak to an authorised financial adviser.

The latest annual reports and factsheets can be obtained from our website at www.fidelity.co.uk/its or by calling 0800 41 41 10. The full prospectus may also be obtained from Fidelity. The Alternative Investment Fund Manager (AIFM) of Fidelity Investment Trusts is FIL Investment Services (UK) Limited. Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited.

Commentary » Investment trusts Commentary » Investment trusts Latest » Isas commentary » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.