Feb

2021

Explain it to a Golden Retriever – World ETFs Review

DIY Investor

17 February 2021

Explain it to a Golden Retriever – World ETFs Review: Guest post from Bankeronwheels.com

Explain it to a Golden Retriever – World ETFs Review: Guest post from Bankeronwheels.com

In 2019, I cycled over 5,000 km across Japan and didn’t wanted to leave (a few typhoons forced me to). One of the reasons is the Japanese architecture, especially the peaceful countryside and Japanese gardens

Japanese people love minimalism and simplicity

In a lot of fields, as Steve Jobs said, Simple is Hard – making a product like the iPhone certainly was

Yet, in Investments Simple is Easy

I spent part of my career analyzing Structure Finance products. Yes, the ones that blew up in 2008 (I actually went into this field only in 2009 – to ‘clean up’ the mess)

You don’t need much knowledge to put your cash to work

In fact, to get exposure to World Equities you only need a single ETF

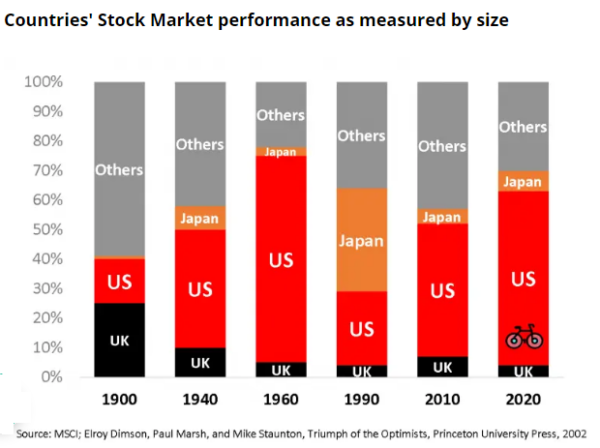

And this exposure evolves with the markets as certain countries grow or decline in World ETF Benchmarks

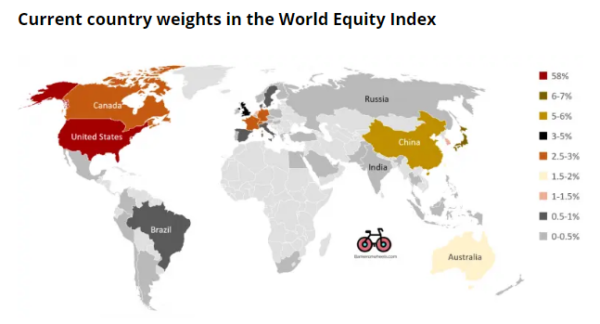

Currently, c. 60% of all World Stocks as measured by market capitalization are US Equities but it wasn’t always that way and…

It may not always remain so. While there are certainly reasons for the current allocations, imagine if China or/and India accelerated opening up (and transparency) of their Capital Markets (China’s current weight is only c. 5% in the Global Stocks whereas its GDP is 65% of the US GDP). The mix of Emerging Market sectors is getting interesting as well

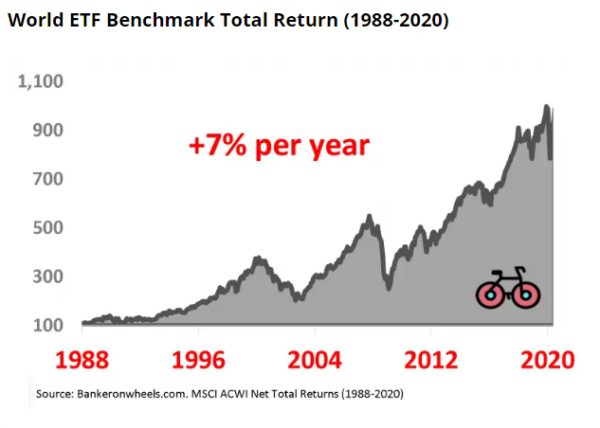

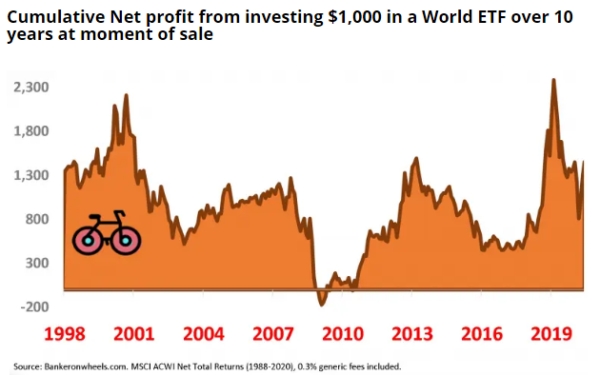

WORLD ETF BENCHMARK PERFORMANCE

If you assume your investment horizon is 10 years…

… by investing $1,000 and keeping it for the entire 10 year period it would have on average returned c. 7% per year (after 0.3% fees) and your portfolio would have doubled (on average) during those first 10 years

Click to read the entire article:

Commentary » Exchange traded products Commentary » Exchange traded products Latest » Latest » Mutual funds Commentary » Uncategorized

Leave a Reply

You must be logged in to post a comment.