Mar

2024

Don’t stop believing

DIY Investor

22 March 2024

Why the UK small-cap sector is ready to shake off its shackles after a tough few years…by Jo Groves

Legendary investor Warren Buffett shared these pearls of wisdom for investors: “Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.” It would be fair to say that UK equity funds have been languishing in the unpopular category for some time, having suffered a consecutive 32 months of net outflows as investors gravitated to the glitz of the magnificent seven.

However, the variation in investor appetite extends beyond a simple UK-US divide, with an additional divergence in the fortunes of small and large-cap stocks over the past few years. Fears of ‘higher for longer’ interest rates have weighed on small-cap valuations across the board, with a torpid domestic economy further adding to the woes of UK equities.

However, with macroeconomic issues beginning to ease, contrarian investors may see current valuations as a highly attractive opportunity to position their portfolio for a potential recovery in UK small-caps.

A track record of outperformance

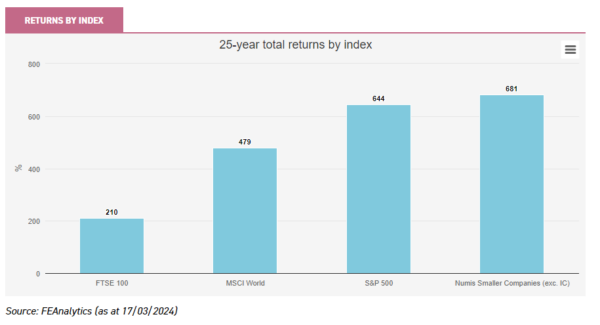

Despite the current downturn, small-caps have outperformed their larger-cap counterparts over the long term. The stellar returns from the US mega-caps may have dominated the financial press of late but the chart below shows that investors would have made higher returns from the (UK-based) Numis Smaller Companies Index over the last 25 years than the S&P 500

There are several reasons behind this outperformance: UK small-caps can offer superior earnings growth, the sector boasts a broad investable universe and limited analyst coverage can lead to pricing inefficiencies. Many UK small-caps also derive a significant proportion of revenue from overseas, making them less dependent on the domestic economy, coupled with robust balance sheets to weather an economic downturn.

In addition, UK small-caps have historically performed particularly well after a period of under-performance, and the current downturn has been longer and deeper than the stock market crashes of the Global Financial Crisis and bursting of the dot.com bubble. A recent note by my colleague showed that, since 1955, every time the Numis Smaller Companies Index had a negative (calendar) year, it has been followed by positive returns for the following three years, with an average return of 84%.

As a consequence, investors will be focusing on the catalysts needed to precipitate the long-awaited recovery in the sector. One such catalyst could be a narrowing of the disconnect between investor sentiment and company fundamentals. Roland Arnold, portfolio manager of BlackRock Smaller Companies (BRSC), remarked in a recent note: “Many smaller companies have enhanced their competitive position, strengthened their balance sheets and continued to generate volume growth in sales, but this has not been reflected in share prices.”

Another tailwind could be the green shoots of an improving macroeconomic environment for the year ahead. The risk of recession has been baked into UK equities for some time and it was notable that the major UK indices rose on recent news of the UK entering a recession. Looking ahead, the OECD currently forecasts that the UK will have the fourth-highest GDP growth amongst the G7 economies in 2024, above the average for the Eurozone, France and Germany.

Attractive valuations

Small-caps valuations tend to be hit harder than large-caps during periods of rising interest rates and elevated volatility. The steep base rate hikes in the UK have taken their toll on the valuations of higher-growth companies, with investors seeking sanctuary in lower-risk assets.

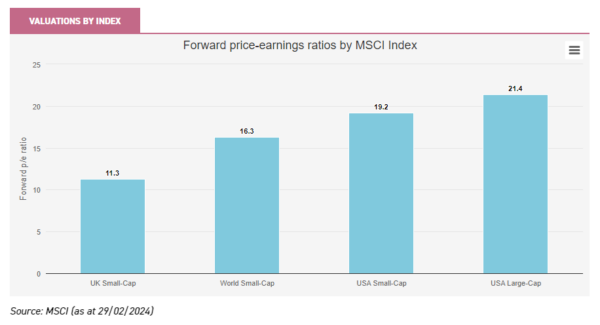

This has proved a double whammy for the UK small-cap sector, which is currently trading at a steep discount to both large-caps and its global peers. As shown in the chart below, the MSCI UK Small-Cap Index is trading at a discount of 70% and 44% to the MSCI USA and World Small-Cap indices respectively.

While investors may have been eschewing the attractive valuations on offer in the listed market, UK public and private companies have been firmly on the menu for strategic buyers over the last five years. There were more than 3,600 M&A transactions in 2023, according to PwC, with strong interest from overseas buyers helped by the strength of the US dollar against the pound.. One such example in the listed market is the £410 million acquisition of UK-based investment bank Numis, a BRSC portfolio company, by Deutsche Bank in 2023.

Private equity firms are also sitting on a record $3 trillion of dry powder and bids for portfolio companies by financial buyers have boosted returns for BRSC. The trust’s latest target was Ten Entertainment, a UK bowling alley operator, with US private equity firm Trive Capital paying £287 million for the company, a 33% premium (to the closing share price prior to the announcement). On a similar note, UK private equity firm Inflexion paid £434 million to acquire a 40% stake in BRSC portfolio company GlobalData to fund organic growth and further acquisitions.

Dividend hero status

The dividend stream offered by many of the FTSE 100 large-caps is widely appreciated, but this quality is often overlooked for smaller-cap companies. The MSCI UK Small-Cap Index offers a yield of 3.6%, comfortably above the 2.1% average yield for its global equivalent and not far below the 4.2% yield for the UK large-cap index (as at 29/02/2024).

BRSC is a newly-minted ‘dividend hero’, an accolade given by the AIC to investment trusts that have consistently increased their dividends for 20 consecutive years. Roland seeks companies with strong cashflow generation, rather than the highest-yielding options, but the current yield of c. 3% (as at 15/03/2024) can diversify returns beyond capital growth alone and the dividend is typically fully-covered.

Investing in UK smaller companies can be higher-risk than their larger-cap peers, however, an improving economic outlook and hoped-for interest rate cuts could prompt a re-rating of the sector. If this is the case, BRSC’s focus on market-leading companies with strong balance sheets should position it to benefit from a recovery in the UK small-cap sector.

View the latest BRSC research note here >

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by BlackRock Smaller Companies. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Alternative investments Commentary » Brokers Commentary » Investment trusts Commentary » Investment trusts Latest » Latest

Leave a Reply

You must be logged in to post a comment.