Aug

2024

Distinguishing noise from trends in sustainable investment

DIY Investor

11 August 2024

Andy Howard, Global Head of Sustainable Investment, discusses the shifting sentiment around sustainable investing

Headlines surrounding sustainability and sustainable investment have clearly shifted. During 2021-22, coverage was almost universally positive, sustainable investment fund performance had been strong across the market and inflows into sustainable products outpaced a wobbling market for fund investments.

Since then, coverage has turned. Typical sustainable investment fund performances have wavered, inflows into those funds have softened, political rhetoric has become more critical and media headlines have become more negative.

In practice, neither the highs nor the lows are representative of the trends, or the fundamental importance of sustainability to the investment industry. The underlying trend is more important than the fluctuations around it.

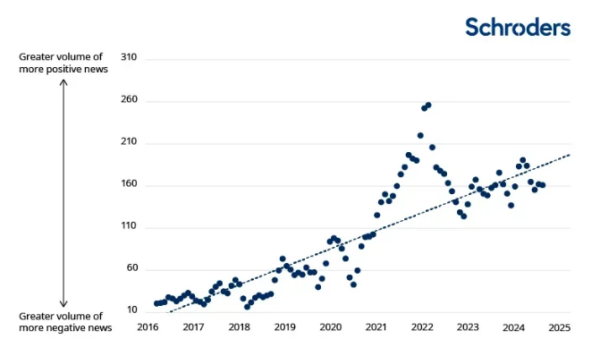

The chart below plots sentiment toward sustainable investment over recent years. We have used a news aggregation service to extract all stories featuring “sustainable investment” since 2016 and a sentiment classification service to determine the positive or negative tone of those stories. By multiplying the volume of stories by the average sentiment in each month, we can gauge fluctuations in media views of the field.

Two things stand out. Firstly, that during 2021-22, sentiment was far stronger than is the case today, reflected in our anecdotal experiences and the “hotness” of hiring into sustainable investment roles at that time. Second, and more importantly, the trend is firmly upward over the period we have been able to examine.

Strength of sentiment toward sustainable investment, indexed

Source: Schroders calculations. We extract news stories from a wide range of sources based on the “sustainable investment” search term and use a sentiment classifier to determine the strength of sentiment toward that topic in each story. We then multiple the number of stories in each month by the average sentiment in that month to calculate the above index. Chart is rebased so that the average “strength of sentiment” is 100 over the period shown.

Sustainable investment will again become a “hot topic”. The areas of focus, the investments that benefit and the acronyms used may look different but we believe the focus will return. The forces that shape our conviction in the importance of sustainability to the investment industry and our clients are only intensifying. Climate change, nature loss, social unrest are growing challenges over which the investment industry’s awareness – and ability to analyse – are rising with increased corporate recognition[1] and disclosure[2].

At Schroders, we take a long term view, focusing on trends that will shape the years ahead rather than shorter term noise. Future demands will look different to those we have seen in the past – less focus on commitments and aspirations and more on practical implementation and delivery – but the importance of sustainability to effective investment decisions and our clients’ interests is unchanging.

[1] For example, the WEF Global Risks Report plots a growing corporate focus on sustainability related risks

[2] Global regulators have introduced growing disclosure requirements, for example see KPMG’s analysis

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.