Sep

2023

Deglobalisation: did Mexico just eat China’s lunch?

DIY Investor

23 September 2023

As trends identified in the “3D Reset” continue to build in the global economy, Mexico has overtaken China to become the number one exporter of goods to the US. We look at what this means for the Asian superpower – by David Rees

In spite of depleted excess savings and much higher interest rates, US consumption has continued to tick along at decent rates of growth. And a period of real wage growth suggests the US consumer will keep the show on the road for a while longer.

As a result, we recently upgraded our forecast for the US economy, and the prospect for resilient consumption lends support to our view that restocking will support an upturn in the global goods cycle in the months ahead.

Too early to call regime shift in global supply chains

That should be good news for export-orientated emerging markets. And as we previously argued, a boost to manufactured exports is one potential bright spot in China’s beleaguered economy. However, it’s not guaranteed.

One push back to the view is that while US consumption has been robust, it has failed to spill over to China in the way it has in the past. Indeed, despite some recent improvement, US imports from China continued to contract by almost 25% year-on-year (y/y) in July.

However, while US imports from China have collapsed, demand for goods from neighbouring Mexico has continued to grow year over year.

We have been arguing for some time that the growing wedge between the US and China, exacerbated by disruptions during the pandemic, meant that there was likely to be a shift in global supply chains.

Indeed, deglobalisation is one of the pillars of what we’re calling the “3D Reset”, and the trend of nearshoring – as countries like the US bring supply chains closer to home, forms a key part of this.

That resilience in US demand for Mexican goods has seen Mexico overtake China for the first time since the early-2000s to become the number one exporter of goods to the US.

As of July, Mexico had a roughly 15% share of exports to the US, whereas China’s share had fallen to 14.6% from a peak of almost 22% in March 2018. Note that we use a 12-month rolling average of nominal US$ dollar exports in order to strip out seasonal effects.

Read more: Globalisation reset: which economies and markets stand to benefit?, or listenhere

And that, while not as dynamic as it is in Asia, Mexican manufacturing and markets ought to benefit from any reshoring of production back towards the US (see links immediately above to written article and podcast covering our latest research on these trends).

But while it is tempting to conclude that we are already witnessing this regime shift in global supply chains, at least three factors suggest that China will still benefit from any upturn in the goods cycle in the months ahead.

Ukraine war, Covid and tariffs have distorted the picture

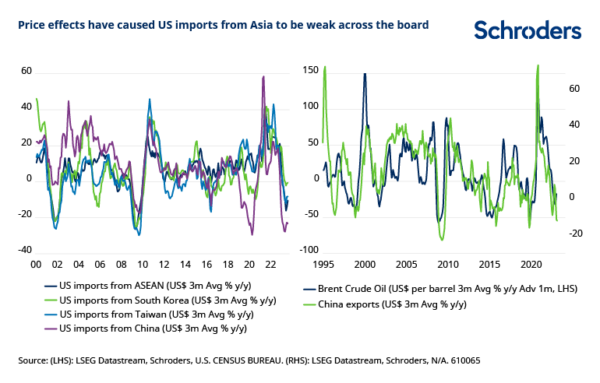

First, while China has underperformed, it is worth noting that US nominal imports from Asia have been weak across the board over the past year. This in large part reflects price effects as the large swings in energy prices since Russia’s invasion of Ukraine wash out of the incoming economic data.

Just as falling energy components have contributed to the decline in global inflation in recent months, this has also dragged down nominal exports as fluctuations in producer prices and transport costs have been passed onto consumers. Indeed, it is notable that, despite being a net import of oil, China’s nominal export growth has historically moved in lockstep with changes in energy prices.

Looking through these price effects, it is worth noting that Asian exports have been growing in volume terms. By contrast, government-mandated price controls through state-owned energy companies meant that swings in energy costs were less violent in Mexico and that they are now having less of a dampening effect on nominal trade.

Second, changes in the composition of US consumption have made it less import-intensive. Whereas in the initial phase of the pandemic and subsequent lockdowns concentrated demand into the goods sector, the reopening of the US economy released pent-up demand for services that rely far less on imported goods.

But while Mexican exporters also faced the same issues, they have benefitted from strong motor vehicle exports as dealers scramble to clear backlogs of orders from the post-pandemic era. Auto exports from Asia have also been faring well, notably China’s emergence as a key manufacturer of electric vehicles. But very little of those products are bound for the US market.

Third, and perhaps most importantly, it appears that Chinese firms are rerouting exports via third parties in order to circumvent tariffs and sanctions imposed by the US government in recent years.

It is always difficult to identify a single smoking gun when it comes to proving re-routing of trade. But a couple of things point that direction.

One is that while China’s share of bilateral trade with the US has fallen, its share of the global export market has not. Indeed, China’s share of global exports shot up during the pandemic and has remained elevated ever since.

There has been some diversification in Chinese trade, for example it has taken a far larger share of trade with Russia since its invasion of Ukraine. But the sheer difference in the size of consumption spending means that more exports to Russia cannot feasibly explain the fact that China has retained global market share even as exports to the US have sagged.

Chinese goods must still be finding their way to the US.

For a description of 3D Reset terms see:

The 3D Reset: the economic terms you’ll need to know

Another indication is that China’s exports to other countries in Asia and Mexico itself have increased markedly in recent years, just as US imports from those countries have also grown strongly. This is consistent with a re-routing of trade via third parties in order to rebadge shipments and avoid trade sanctions.

Indeed, it is notable that China’s trade balance with Mexico itself has risen by about 1% of GDP during the recent period of weak bilateral trade with the US.

However, while Mexico stands to benefit from the new regime in global trade, reshoring will be a slow moving process that takes years rather than months. In the meantime, if we are right in expecting an upturn in the global goods cycle, that ought to be a positive catalyst for China’s economy and some of its markets – particularly the renminbi which has weakened sharply this year and is driven in large part by the export cycle.

While the authorities are currently busy trying to lean against depreciation pressures, announcing incremental measures aimed at supporting the currency around 7.20-7.30/$, we expect it to strengthen as exports pick up.

![]()

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.