Dec

2023

Consumer watch – Falling into the Fall

DIY Investor

6 December 2023

A weaker quarter for the consumer sectors

The UK, Continental European and North American consumer sectors took a backward step in Q323 and underperformed their regional indices to a greater or lesser extent. This brought to an end a relatively favourable run of performance for the UK and Continental Europe consumer sectors that began at the end of 2022.

The weakness was broad-based among the sectors, suggesting that bigger-picture concerns began to weigh on the companies again. Rising bond yields through Q323, notably for the US and Continental Europe, were a challenging headwind for equity valuations.

Overall profit upgrades, but breadth of upgrades mixed

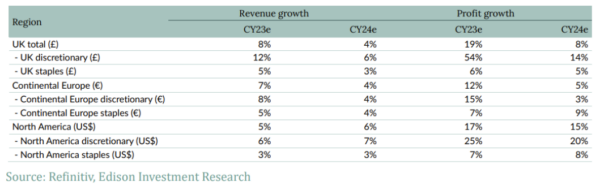

There was yet another general uptrend in aggregate CY23 profit estimates during the period, but it was more of a mixed picture at the company level. Prior to Q323, there had been a pretty clear trend of an increasing number of earnings upgrades versus downgrades for the individual companies, albeit there were still plenty of negative surprises.

However, this went into reverse in Q323 and the pattern was consistent across the three geographic blocks, with more downgrades than upgrades for the companies. So, while strong overall growth in profit is expected for the year (helped by easier comparatives due to COVID restrictions and lower inflation on some costs versus the peak), ongoing low economic growth, higher interest rates and still above-average inflation have understandably taken their toll.

Roughly one-third of the companies for which there are estimates are expected to generate lower absolute profits than achieved in CY22. The downturn was pretty well-flagged, so it is clear that there is only so much cost cutting that some companies have been able to do to offset volume declines and inflationary pressures.

As we near the end of the year, we take our first look at CY24, and it is pretty clear that optimism abounds based on consensus estimates: the majority of companies (ie more than 90% for which there are estimates) are expected to report higher profits than forecast for 2023. We suspect this may be food for the bulls and bears.

Exhibit 1: Consensus growth expectations

Plenty of valuation opportunities

Our valuation screens, which compare current (end-September 2023) multiples to the companies’ long-term (2006–22 to take into consideration the last cycle) averages, suggest that there continues to be a good deal of value in the sectors.

We appreciate that times have changed from a cost of capital perspective, but the size of the discounts to historical multiples appears high for many companies. There remains more apparent value in the UK (Exhibit 21) and Continental Europe (Exhibit 31) than in North America (Exhibit 40), or perhaps there is just less scepticism about the outlook for the latter over the two other regions.

Access the full report here >

![]()

Leave a Reply

You must be logged in to post a comment.