Jul

2021

Consumer revenge – the next stage of the recovery in Europe

DIY Investor

4 July 2021

Is pent-up consumer demand the key to unlocking value in Europe? In this article, John Bennett, Director of European Equities, considers some of the meaningful trends he believes could drive positive momentum in the region

Is pent-up consumer demand the key to unlocking value in Europe? In this article, John Bennett, Director of European Equities, considers some of the meaningful trends he believes could drive positive momentum in the region

Key Takeaways

- As we progress towards a post-pandemic world, the next stage of the recovery is likely to be led by consumers, armed with record-high savings.

- Political instability (including Brexit) and COVID-19 have left European equities out of favour. As these headwinds pass, the valuation gap between Europe and the US appears extreme.

- We expect the unprecedented synchronised fiscal and monetary response to COVID-19 to lead to an inflationary environment which warrants consideration of a greater allocation to Europe.

While Europe has faced renewed COVID-related restrictions over the past few months, we are now seeing significant progress in the vaccination campaign. Having witnessed a profound ‘V-shape’ recovery in the industrial economy, it is our view that the next ‘V-shape’ will be led by consumers. The risk of potential virus mutations demands vigilance, but we believe the direction of travel – back to some semblance of social and economic normality – is clear. It is merely the speed of travel that remains uncertain.

The reopening play

As we progress towards this post-pandemic world, many consumers have accumulated record-high savings due to limited consumption opportunities during lockdown and supportive furlough measures. The term ‘revenge spending’ has been coined to express the fervour of the unleashed consumer. The US, UK and Israel – with the most advanced vaccination programmes – offer glimpses of the consumer revival: clothing, cosmetics, holidays, homeware, eating and drinking all feature on wish lists. We anticipate this will be replicated in Europe as the vaccine programme catches up.

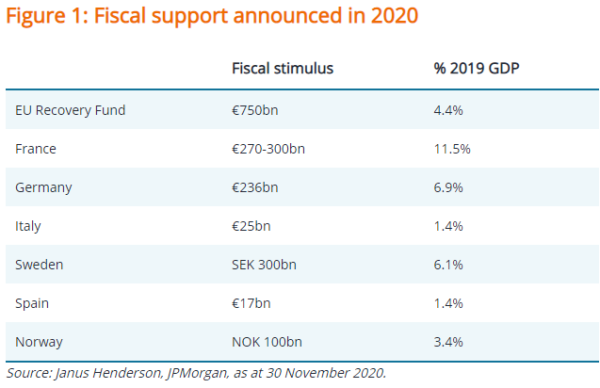

We expect consumer finances to remain supportive: US payrolls have surprised positively and are on track to return to pre-pandemic levels by the end of 2021 if job creation continues at the same pace. Economic growth in the UK is expected to reach over 6% in 2021, with additional government spending aimed at supporting employment. In the European Union (EU), aside from the measures undertaken by individual countries, financial assistance of up to €100bn has been made available to help preserve jobs under the SURE1 instrument, in the form of loans to member states. European Central Bank policy has been correspondingly accommodative, with the relaxation of the Stability and Growth Pact to help governments support their economies through the pandemic, as well as a raft of country-specific and other regional measures implemented in 2020 (Figure 1):

Political instability, including Brexit, and the impact of COVID-19 have limited the appeal of European equities to investors. As these headwinds pass, the valuation gap between Europe and the US begins to look unjustified (Figure 2). On a fundamental level we are encouraged by many of the recent corporate earnings releases in Europe comfortably ‘beating’ analysts’ expectations.

Source: Janus Henderson Investors, Refinitiv Datastream, from 1 February 1983 to 1 May 2021. Past performance is not a guide to future performance. Shiller P/E Ratio = a price-to-earnings ratio adjusted to take into account the cyclicality of markets.

Risk and reward

The beneficiaries of ‘stay at home’ trends, such as video conferencing and food delivery, technology and Software as a Service (SaaS), have until recently been afforded ever-higher multiples of future earnings by the market, with share prices reflecting heightened expectations. COVID-19 further fuelled the decade-long outperformance of the ‘growth’ factor in stock markets, which has tended to favour the more technology-heavy US market over Europe. Conversely, due to the often-binary nature of the market, many high-quality businesses have been penalised, with earnings multiples (share prices) implying run-off or disruption. Amidst its abundance of ‘old economy’ sectors, such as steel, agriculture and manufacturing, trading on optically cheap valuations, the European market has been blessed with some global champions.

The automotive industry offers up a perfect illustration of this dichotomy: Tesla, a US-listed electric vehicle ‘disruptor’, is seemingly priced for global domination. In Europe, longstanding premium auto brands like Mercedes-Benz and BMW are priced as hapless victims of the looming transition to electric vehicles. At such extreme valuation disparities, a small change in market perception can have significant share price implications.

Is inflation finally making a comeback? If so, Europe stands to benefit

US equities have led Europe for the past decade, aided by the US market’s greater abundance of ‘growth’ stocks which benefit from low interest rates. We believe the unprecedented synchronised fiscal and monetary response to COVID-19 offers the best prospect for a return of inflation since the global financial crisis. If inflation proves to be more than the US Federal Reserve’s ‘transitory’ base case, a change in market regime is likely; one which, in our view, broadly favours a rebalancing towards ‘value’ at the expense of ‘growth’ and by extension, towards Europe and away from the US.

1 Source: SURE (‘Support to mitigate Unemployment Risks in an Emergency’)

Click to visit:

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Commentary » Equities » Equities Commentary » Equities Latest » investment trust commentary » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.