Feb

2024

Bring some ying-yang into your portfolio in 2024

DIY Investor

7 February 2024

Inherent contradictions within portfolios can give them stability in a polarised world…by William Heathcoat Amory

Investors must always confront a wall of worry. Long-term investors reassure themselves that the stock market’s ability to surmount these issues is one of life’s constants, with the adage that it is time in the market, not timing markets, that truly protects and generates wealth. On the other hand, it is always hard to ignore that nagging doubt, and convince yourself to take what feels like an uncomfortable leap into the stock market despite what might seem to be clear warning signals.

In this context, the outlook today seems more than unusually uncertain. Tensions in the Middle East continue to ratchet up, giving an excuse for bad actors such as Putin and the Iranian regime to stir up hostilities elsewhere. If that wasn’t enough, politics globally has become even more polarised, and an unusual number of elections occurring in 2024 will mean the potential for significant shocks and/or shifts in economic policy and sentiment. Within the election cycle, for the first time the risk of AI-generated fakery lies as a malign presence, potentially leading to even less predictable electoral outcomes. China seems to be slowing rapidly, threatening to drag the global economy into recession, with a rumbling crisis in its property sector and declining population raising the stakes for its unelected ruling elite. Is it impossible that they look towards an invasion of Taiwan to distract their citizens from the economic mess?

Run for cover

Time to head back under the metaphorical duvet, and continue to hold those short-dated government bonds?

I don’t think so. As my father is fond of saying, “’Twas ever thus”. And how could it otherwise be? In the 1970s a British scientist working for NASA came up with a hypothesis for detecting the potential for life on other planets that would be both cheap and effective. James Lovelock theorised that planets that have atmospheres that are in chemical equilibrium and therefore chemically stable will be lifeless, but those such as Earth that have highly reactive chemicals, such as oxygen and methane in stable concentrations, will exhibit life. In what became known as the Gaia hypothesis, Lovelock proposed that Earth had evolved into a self-regulating system, in which life itself perpetuates the conditions for life.

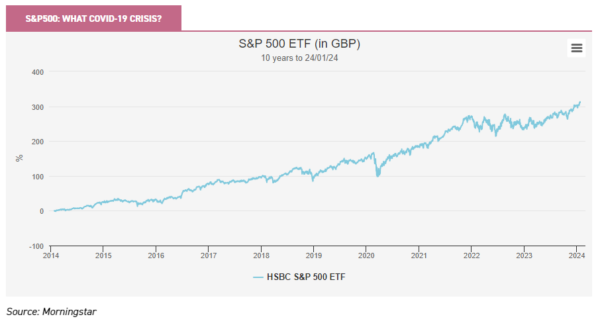

The central tenet of the Gaia hypothesis is that in having a dynamic system with feedback loops, the Earth can be seen as self-regulating, and whilst elements in the system are unstable, overall the system is very stable. He theorised that on Earth, if a natural cycle starts to go out of kilter, then other cycles tend to kick in and bring the system back into line, a process which continuously optimises conditions for life. In this way, Gaia may illustrate one of the fundamental truths about stock markets, which are also collectively a dynamic system with feedback loops. In order for markets to function, optimism must always be balanced by fear. At times, one may dominate the other, but only for very short periods before feedback loops start to kick in. One only has to remember the abject fear we all experienced during Q1 of 2020. A new pandemic appeared, politicians had no idea what to do, and with economic activity supposedly grinding to a halt, stock markets cratered. Yet an element of optimism soon crept back into markets, likely a function of prices having fallen, and a new equilibrium was soon reached. The market stopped falling, and then crept back upwards, and it wasn’t long before the S&P 500 had risen back above its previous heights. In fact, taking a step back, the COVID-19 crash seems nothing much more than a blip.

In order to demonstrate the Gaia hypothesis, Lovelock constructed a thought experiment, known as Daisyworld. Two species of daisy exist, one dark, which does well in less warm conditions, and one white, which does better in warmer conditions. As one competes the other out, it changes the reflective properties of Daisyworld’s surface, and thereby the overall temperature. So when dark daisies start to dominate the surface, the Daisyworld heats up and more white daisies thrive. This in itself increases the amount of the sun’s energy reflected back to space, and Daisyworld cools slightly, meaning dark daisies do better once again. The coexistence of these daisies and their reflective properties mean a constantly evolving equilibrium is maintained, which aligns with the optimum temperature for daisy growth. In the experiment, if the luminosity of the sun is varied, the overall temperature of Daisyworld is significantly more stable than it would be with only one species of daisy. This is a basic example of feedback loops creating stability for a system that would otherwise be less stable.

A precondition for stability in Daisyworld is therefore constant instability. Whilst Lovelock found popularity in the West, similar ideas – written about much earlier – can be found in Russia in the late 19th and early 20th centuries. For example, Vladimir Vernadsky was one of the first scientists to recognise that oxygen, nitrogen and carbon dioxide result from biological process (i.e. life). He pointed out that living organisms in the biosphere (which was a relatively new term at the time) would shape conditions on Earth, and as a result he is considered as a pioneer in environmental sciences. In the east, the Chinese philosophy encapsulated by yin and yang can be summarised as a constant duality, in which complementary forces (rather than opposing forces) interact to form a dynamic system. Everything can be seen to have duality: shadow cannot exist without light, male without female, winter without summer.

The parallels from Gaia, from early Russian scientists, and the ancient Chinese philosophy of yin and yang can all be seen in stock markets. Despite the constant threat of instability, markets actually tend to be fairly stable, except over the very short term. Buyers and sellers find equilibrium, which results in share prices moving constantly, but effectively in a relatively stable system. Yet at all times, and as a precondition of this stability, market commentators and participants continuously recognise and fear destabilising influences on share prices and stock markets.

A topical example of one of these perceived threats to market stability – outside of politics this time – is the rise of passive investing. We recently heard news from Morningstar that in the US for the first time ever, 2023 saw passively managed mutual funds and ETFs reach total assets of greater than actively managed funds and ETFs. According to Morningstar, at the end of December 2023, passive US mutual funds and ETFs held about $13.3tn in assets while active ETFs and mutual funds had just over $13.2tn. Active managers typically decry the rise of passive investors as a systemic threat, while others see hedge funds as a systemic threat to markets. In reality, these market participants are all part of the stock market’s rich tapestry, and all are merely actors that help the market function efficiently. Borrowing the Daisyworld example above, one might rationalise that if passive investors become so dominant that they start to influence share prices too much, active managers should start to turn in better relative returns, attracting inflows at the expense of passives, and thereby restoring equilibrium. The system self-corrects, but is also more stable than if only one type of investor existed.

Ironically, regulation is the godlike external threat to this stability, to the extent that unintended consequences of seemingly ‘good regulation’ leads to extinctions in parts of capital markets. The current campaign to correct the inequalities of cost disclosures for investment trusts is one reaction to the unintended consequences of seemingly ‘good’ regulation. As long as regulators and governments listen (i.e. there is a feedback loop), then even regulation shouldn’t destabilise markets.

And so, back to 2024. What does Gaia or yin-yang tell us about the prospective year ahead? Let’s take the US election as a seemingly intractable problem. Here we have a very polarised election, with two opposing sides who seemingly stand for very different things. And if Trump is elected, his no-holds-barred attitude may conceivably see the US leave NATO, or the green incentives contained within the Inflation Reduction Act may be ripped up. Undoubtedly, the world will look very different depending on how a few floating voters in a small number of US states feel when they get out of bed on 5th November. Who can make a sensible long-term investment with this Sword of Damocles hanging over the world?

Obviously, diversification will help. However, perhaps trusts which exhibit Gaia-like, self-balancing portfolios are the answer. One trust springs to mind, which in our view could potentially demonstrate stability, irrespective of the US election result: BlackRock Energy & Resources Income (BERI). Following a shift in the mandate in 2020, BERI now has three proverbial legs to its investment stool. The team invest in mining and traditional energy companies, and also in ‘energy transition’ stocks. Allocations between these three are expected to be 40/30/30 respectively over the long term, but can be very dynamic. An example, which has led to very impressive performance, came in November 2020. At the time, energy transition stocks were riding high and the team took decisive action to rotate the portfolio into traditional energy stocks. At the time, these were trading at historically low valuations, but with the news of a COVID-19 vaccine, the thesis was that they would benefit from economic activity normalising. This led to significant outperformance in subsequent years – helped yet further by the underperformance of energy transition stocks and the tailwind to energy stocks from the invasion of Ukraine by Russia. It is interesting, in our view, that the team are now looking at the attractively valued energy transition sector once again.

Aside from the specifics, like the Gaia hypothesis showing that it is only unstable atmospheres that support life, BERI’s seemingly intractable contradictions in its portfolio mean that it offers potential protection for an event like the upcoming US election. Oversimplifying things, if Biden wins, then it is probably safe to say that the energy transition continues, which should benefit BERI’s energy transition stocks, not to mention traditional miners, who are set to benefit from supplying the required metals. On the other hand, if Trump wins there will undoubtedly be a significant degree of uncertainty for renewable energy companies, and their prospects will clearly be dimmer. In this scenario, BERI’s traditional energy stocks may perform strongly, with direct support from Trump and potentially less of a headwind from alternative energy.

This posed a thought – which other trusts also exhibit what might be seen as structurally contradictory portfolios, and would they also offer a way to ride out a bifurcated outlook such as the year we face ahead of us?

In the US’s home market, JPMorgan American (JAM) has been a standout performer since the current approach was adopted in 2019. It has two managers, running two distinct growth and value portfolios, both in a high-conviction manner. Outperformance relative to the benchmark and the competition has been impressive, especially when one considers how hard it is to deliver alpha from traditional US portfolios. The combination of two, at times contradictory, portfolios enables outperformance over what has been a difficult time for active management. JAM’s discount remains relatively narrow, a result of the board’s careful attention to buyback activity.

Closer to home, Invesco Perpetual UK Smaller Companies (IPU) stands out in a sector that is trading on wide discounts, and underlying valuations that are arguably very low. The UK smaller companies trust sector can be characterised by the majority of the peer group being very much in the growth camp, whilst Aberforth continue to plough a lonely furrow on the value side. IPU’s managers have adopted a barbell approach to the growth and value question, with significant exposure to both. Longer term, they have delivered above-average returns in the sector, with below-average volatility through a diversified portfolio and not exposing investors to any extremes in terms of valuations, sector exposures or balance-sheet strength. Historically ungeared, the managers have for the first time in our long experience of following them drawn down gearing. It is this sort of signal that we think investors should sit up at – prompted as it is by the manager’s contention that valuations are too cheap. If they are right, the prospect of a strong rebound will be compounded by gearing contributing to NAV returns and the prospect of the discount narrowing. However, IPU’s barbell portfolio potentially allows investors to not have to make a call whether it is growth or value that is going to perform most strongly.

Uncertainty and volatility, with diverging central bank responses, is ideal territory for macro hedge funds. As such, the economic and political uncertainty that lies ahead of us in 2024 could make it a banner year for such funds. Whilst many commentators bemoan the choice of interesting companies on the London Stock Exchange, UK investors may consider themselves fortunate to have a highly liquid access point to one of the foremost hedge funds of all time: the Brevan Howard Master Fund. BH Macro (BHMG) is a feeder fund into Brevan Howard’s flagship macro fund. Since IPO, BHMG has delivered equity-like NAV total returns of 8.7%, with significantly lower volatility than equities of 8%. Taking the theme of this article, BH Macro fits the bill because of how the BH Master Fund’s assets are allocated. The investment committee at Brevan Howard effectively allocates capital across a broad range of the firm’s macro traders, who tend to focus on global fixed-income and FX markets but with peripheral exposures to equity, credit, and commodities. Each trader has a very specific mandate, restricting them to areas of a market or even specific instruments. As long as they stay within their mandate and risk framework, each trader is free to position their book in whatever way they see fit. In some cases, it is possible that traders may at times have opposing views or trades. The portfolio and traders are policed by a highly resourced team of risk managers, who are central to everything that the firm does.

It is through this process that the Master Fund aims to provide compelling, asymmetric returns for investors, irrespective of market conditions. Capital is currently allocated across a team of over 170 portfolio managers/traders, aiming to diversify exposure across the best risk-adjusted opportunities within developed markets. Underlying exposures of the Master Fund can be very dynamic. Importantly from a portfolio-diversification perspective, it has historically delivered its strongest returns in periods when equity markets have struggled. Following a relatively poor 2023, and fears about a potential overhang in shares following the merger of its two largest shareholders, BHMG has fallen to a wide and seemingly persistent discount of 10%, which may prove to be an attractive entry point, should sentiment improve. At the time of writing, BHMG has had a very strong second week of 2023, with the NAV now having seen a rise of 0.77% since the start of the year to 12/01/2024.

Finally, one trust that specifically sets its stall out as aiming to have as many eventualities covered within its portfolio at the same time is Ruffer Investment Company (RICA), which invests in the highly flexible Ruffer investment strategy. The team aim to generate positive returns in all market environments, and not lose capital in any 12-month rolling window. Their approach involves, in the words of founder Jonathan Ruffer, “looking for the opportunities created by juxtaposing investments which benefit and those which suffer from the same impulse”. Typically this is achieved by having equity and bond positions, and the team mitigate the possibility that these two asset classes correlate by also employing protective derivative strategies and non-conventional assets within the portfolio. Historically, this has helped RICA to perform very well in falling markets and rarely lose money. That said, 2023 was uncharacteristically weak, with the strategy having returned -6.2% during the year.

Looking forward, the Ruffer team believe that if the market’s anticipated six US interest rate cuts come to pass, it will be because of the arrival of a recession. However, they reason a soft landing is not an impossibility, and so the fund holds over 20% across equities and commodities, which should benefit from a broader market rally and further economic strength. If recession arrives, the fund’s fixed-income positions and gold equities should rise in value if yields fall further. They believe that the portfolio’s balance, painfully elusive at points last year, is now much more secure. Crucially, if liquidity conditions and the economy do deteriorate – as is their central scenario – the derivative holdings (primarily credit protection and exposure to the VIX) should appreciate sharply. With the trust trading on a discount to NAV of 5%, this may be an opportune time to consider its attractions as a portfolio diversifier. That said, while they have some counterbalancing positions, RICA is likely to do best if the managers’ macro views are proved correct, and as such we think the trust stands out as a hedge against a hard-landing scenario.

Conclusion

At university – bound up with studenty enthusiasm – I smashed through the 10,000 word limit for my dissertation (‘The impact of Gaia on business organisations’), finally handing it in with 45,000 words. I did get a first for that particular bit of work, possibly a result of my tutor giving me the benefit of the doubt and certainly in the knowledge that no one else would ever read the whole thing to find out and say otherwise.

Whilst we all like to think we can see the future clearer than anyone, in reality no one can. Having a manager or portfolio that recognises this fact, and has an element of Gaian portfolio balance or yin-yang, likely enables a smoother ride. In the coming year it looks like having consistent inconsistency in portfolios may make plenty of sense.

Disclaimer

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Leave a Reply

You must be logged in to post a comment.