Sep

2021

Bitcoin’s investment thesis – Volatility and market manipulation

DIY Investor

14 September 2021

Cryptocurrencies – irrational hype or financial revolution? Part 6 of 8

Bitcoin (BTC) and other digital assets have been making the headlines in recent months, polarising the investment community with an equal number of strong advocates and fierce critics (even within the same financial institution or research house). Moreover, valid analysis, backed by in-depth research, is mixed up with ideological, poorly researched conclusions both for and against the theme. We have decided to look at both sides of the same (Bit)coin to extract the investment thesis behind this new asset class. Each part of this Edison Explains series looks at one feature of BTC and the broader cryptocurrency landscape (broadly referred to as ‘altcoins’). We conclude by summarizing our subjective view on how positive or negative we believe the feature is for BTC’s investment thesis.

![]()

Several reasons for BTC’s high volatility

Cryptocurrencies (including BTC) are a highly volatile asset class: daily price movements reaching high-single digit percentage levels are quite frequent and daily changes of +/- 10–20% are also not uncommon.

The average monthly BTC return in US dollars over the last five years is c 10%, while the standard deviation of monthly returns is c 25%. This may be due to a combination of several factors. First, it is worth pointing out that only c 20% of circulating BTC supply is being actively traded (see Glassnode or Chainalysis for details). Moreover, liquidity is dispersed across multiple trading venues (centralised and decentralised exchanges as well as OTC markets).

Second, unlike traditional trading venues there are no ‘circuit breakers’ on crypto exchanges. Third, volatility is elevated due to the high level of activity of speculative retail investors (given the early stages of institutional adoption) who often use excessive leverage. Finally, BTC is difficult to value, with no broadly accepted valuation method.

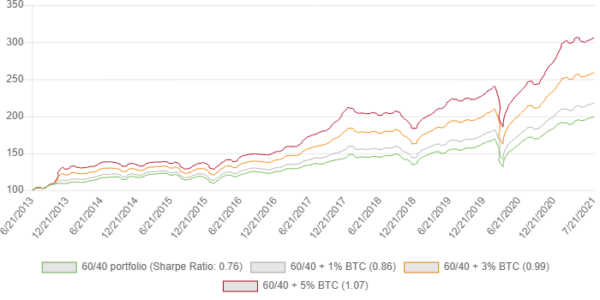

Visibly improving a portfolio’s Sharpe ratio

Having said that, we also note that BTC has historically been a good enhancer of the Sharpe ratio within a broader cross-asset portfolio.

This is because there has been only moderate positive correlation between monthly BTC returns versus major equity indices, with Pearson’s coefficient over the last five years at c 0.27–0.29 (c 0.16–0.18 over 10 years), according to our calculations. Moreover, BTC and gold have shown no meaningful correlation with each other.

Together with BTC’s strong performance over a longer time horizon (despite c 80–90% de-ratings from previous peak during bear markets), this translates into a positive impact even for a small 1–5% allocation to BTC (see below). Allocation to some of the major altcoins (eg Ether) had an even more positive impact on portfolios.

Having said that, we acknowledge that even a small crypto allocation may push the overall volatility of the portfolio beyond levels acceptable to some investors and investment managers. However, this may be at least partially mitigated by periodic (eg quarterly) portfolio rebalancing, as discussed in detail by CoinShares’ research.

Impact on returns of adding a minor BTC allocation to a 60% equity/40% government debt portfolio

As some crypto proponents say, ‘volatility is the price you pay for performance’. It is also worth noting that high volatility is attractive for traders with a short-term investment horizon.

Elon Musk accused of ‘pump and dump’ scheme

The BTC price is quite sensitive to individual news headlines or tweets, as illustrated for example by the impact of Elon Musk’s comments (which are quite vague at times). Amusingly, commenting on his private holdings of BTC during a recent ‘The B Word’ conference, Elon Musk said that: ‘I might pump, but I don’t dump.’

Until crypto markets mature, prices may continue responding not only to tangible signs of sustainable progress in terms of digital assets adoption, but also less concrete indications of interest in digital assets (or the lack of). In the meantime, investors have to cut through the noise themselves.

Liquidity inflated by ‘wash trading’

Moreover, as a significant number of crypto trading venues are still not regulated to the same extent as traditional exchanges, they are often subject to market manipulation. In particular this includes ‘wash trading’ (ie buying and selling an asset between trading accounts held by a given trader, group of traders or exchange for the sole purpose of feeding misleading price and volume information to the market).

A number of cryptocurrency exchanges allegedly use wash trading to overstate their liquidity to attract new investors and coin listings. While the extent of this practice is difficult to quantify without access to account-level data on exchanges (which they usually keep confidential), a recent academic study suggests that wash trading represents more than 70% of the volume on unregulated crypto exchanges (amounting in aggregate to over US$1trn per month).

Interestingly, even Coinbase, one of the most reputable crypto exchanges, which completed its IPO on Nasdaq earlier this year, agreed to pay US$6.5m in March 2021 to resolve a Commodity Futures Trading Commission (CFTC) investigation into claims of ‘reckless false, misleading, or inaccurate reporting’ and wash trading by a former employee between January 2015 and September 2018 on Coinbase’s GDAX platform (though Coinbase neither admitted nor denied the claims).

“While BTC tends to be highly volatile, a small 1–5% BTC allocation has historically improved the Sharpe ratio of a standard 60% equity/40% debt portfolio quite significantly. Nevertheless, the cryptocurrency market is yet to mature in terms of resistance to market manipulation (‘wash trading’ in particular) and systemic shocks.”

Controversies around the USDT stablecoin

A convenient way for crypto investors to add funds to their crypto holdings (ie to have an ‘on-ramp’ option) and keep a cash-like reserve without moving the funds off-chain are stablecoins (ie cryptocurrencies whose value is pegged to a given fiat currency such as the US dollar). They are issued in exchange for the fiat currency they are pegged to, which is then kept as a reserve by the stablecoins’ issuer.

The most important stablecoin (and at the same time the third-largest cryptocurrency overall) has been Tether (USDT) with a current market capitalisation of c US$65.5bn.

Some market participants have been concerned about the US dollar reserves backing USDT – if they cover all the stablecoins in circulation to justify the peg and in what kind of assets are they held.

Moreover, in a study published in 2018, authors from the University of Texas claimed that entities associated with the Bitfinex exchange (a sister company to Tether as both are owned by iFinex) used the stablecoin to push up BTC price following downturns between March 2017 and March 2018 (ie during a major crypto boom and bust).

The US Department of Justice and the CFTC have been investigating this since 2018, according to Bloomberg, but with no official results yet. Having said that, the approach behind the above-mentioned study faced some criticism (see for instance BloombergQuint or LongHash for reference). Another study from the University of Queensland Business School concluded that no empirical evidence for the USDT impact on BTC prices could be found.

Furthermore, In February 2021, Tether and Bitfinex agreed to pay a US$18.5m fine to settle a legal dispute related to the alleged use of at least US$700m of USDT reserves to help cover a US$850m loss of Bitfinex arising from the Crypto Capital fraud, without disclosing it to investors (as implied by the New York Attorney General). Bitfinex eventually repaid the full amount to Tether.

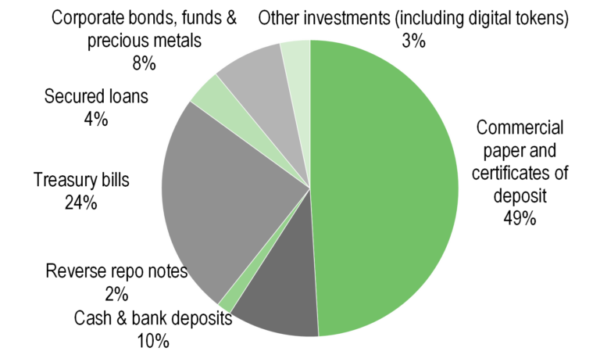

As part of the efforts to stay compliant with the above-mentioned settlement, Tether has started releasing a breakdown of its reserves. The latest available attestation as at end-June 2021 shows that close to 50% is invested in commercial paper and certificates of deposit, with a further c 8% in corporate bonds, funds and precious metals. According to the document, the commercial paper and certificates of deposit are predominantly rated A-2 (45%) or A-1 (47%) and have an average duration of 150 days.

Still, Fitch recently pointed out that given Tether’s commercial paper holdings may be larger than most prime money market funds in the United States and Europe, Middle East and Africa (EMEA), a sudden mass redemption of USDT could affect the stability of short-term credit markets amid wider selling pressure in the commercial paper market. In this context, we note that Tether’s assets exceeded its liabilities from issued USDT stablecoins by only 0.2%.

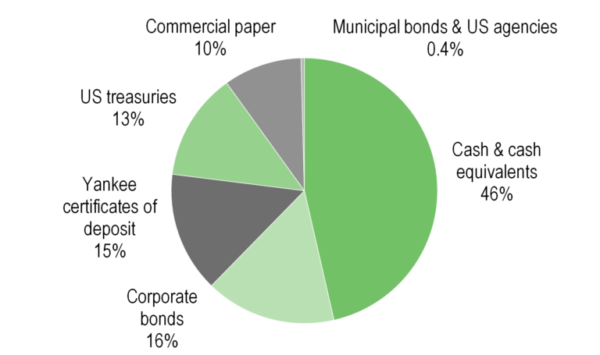

Meanwhile, the reserves of USDC, the second largest stablecoin with a market cap of c US$27.0bn, have been released by Circle (its administrator) as well, showing 46% held in cash and cash equivalents (see exhibit below), and the overall portfolio maintaining an average credit rating of A or better on the S&P scale and a weighted average maturity of less than or equal to 1.5 years.

Commercial paper made up just 10% of USDC reserves. Cash and cash equivalents include ‘US dollar deposits at banks and short-term, highly liquid investments that are readily convertible to known amounts of cash and have a maturity of less than or equal to 90 days from purchase’.

USDC’s assets were presented as being at least equal to the liabilities from the issued stablecoins. We note that in a recent tweet, Emilie Choi (president and COO of Coinbase, which is part of the consortium behind the stablecoin) said that all USDC’s reserves will be held in cash and short-duration US government treasuries starting in September 2021.

USDT reserves as at end-June 2021

USDC reserves as at end-June 2021

We note that USDC has been recently gaining market share in the stablecoins market assisted, among others, by high interest from the Decentralized Finance (DeFi) sector, with nearly 50% of its circulating supply locked in DeFi projects versus 20% of USDT supply.

Market manipulation, alongside price volatility, is likely one of the main reasons why a Bitcoin exchange traded fund (ETF) has to date not been approved in the United States, though a few have been approved in Canada this year (Purpose Bitcoin ETF, Evolve Bitcoin ETF, CI Galaxy Bitcoin ETF and 3iQ CoinShares Bitcoin ETF).

![]()

https://www.websiteplanet.com/blog/bitcoin-statistics

Leave a Reply

You must be logged in to post a comment.