Sep

2025

Banker on Wheels road-tests Vanguard Life Strategy Funds

DIY Investor

22 September 2025

Have you ever invested in that pharma stock that initially surged, then stagnated and underperformed the market – because most of them do – then been unable to sell it because of your emotional attachment? writes Banker on Wheels

If you don’t want to think about selling or buying, or even rebalancing, you may be pleased to know that the Golden Retriever Portfolio (with a little nuance) is now available in one UCITS fund – Vanguard LifeStrategy.

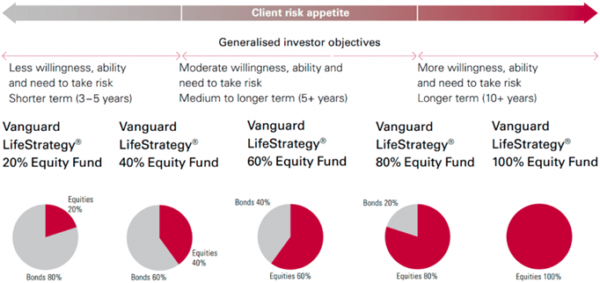

What is Vanguard LifeStrategy?

It may not be your cup of tea – some investors like flexibility; but if asked about the ‘best investment’ for a bear or a bull market at a (post Covid-19) family reunion, LifeStrategy may be the answer to save them money and stress.

If they ask about bonds, tell them this Babushka doll includes them as well; LifeStrategy is so easy to explain, even a Golden Retriever gets it.

Until now, it was fairly easy to buy a Equity World ETF. But you would usually want a World Bond ETF that goes with it; LifeStrategy are Funds of Funds offering a cheap global, diversified portfolio with a fixed level of equities determined by the share component of the portfolio.

Who are Vanguard LifeStrategy Funds for?

LifeStrategy funds are the perfect solution for you if:

- You are investing for the long term and want an established and reliable provider

- You are looking for simplicity and a cheap fund

- You want to have hands-off portfolio without the need to rebalance

- You want to lower transactions costs and taxes

Vanguard LifeStrategy Funds may not be suitable if:

- You like to build a portfolio to your personal needs or want full flexibility (e.g. Banker or Cyclistportfolios).

- You want to reduce costs to the absolute

- You want an asset allocation other than 80/20, 60/40, 40/60, 20/80, one that changes over time or don’t want bonds

Vanguard LifeStrategy may not fulfill all your needs, but can serve as the backbone of your portfolio if you add other investments around a core fund or tweak the allocation by adding a World ETF.

LifeStrategy Fund types

The underlying ETFs are the same for each LifeStrategy Fund, which are in turn composed of a wide range of ETFs:

Bonds – Vanguard Global Aggregate Bond UCITS ETF

Equity – Vanguard FTSE All-World UCITS ETF

Each fund is rebalanced regularly so that its asset allocation remains fixed over time –understand how rebalancing works.

The funds differ by the asset allocation or the proportion of Equity and Bond ETFs; Vanguard recommends 60% and 80% Equity ETFs for investors with a higher risk profile and 5+ years investment horizon.

The only difference with a Golden Retriever portfolio is that it does not include Inflation Linked Bonds/Gold which could be helpful in rare scenarios when both Equities and Bonds underperform at the same time (look here for the 1970s).

Vanguard LifeStrategy Funds have traded on the US Stock Exchanges since 1994, and launched in the UK in 2011; it started trading LifeStrategy ETFs on Germany’s Xetra exchange and Borsa Italiana in December 2020.

Choosing a LifeStrategy Fund

The primary criterion when choosing a fund is how much risk you can tolerate; you don’t want to end up like this guy.

Stress testing the funds in the decade starting just before the Dot Com crash and including 2008’s GFC showed a 100% Equity portfolio losing almost 55% of value during both stress periods. A 60% Equity portfolio dropped 25-30%. By comparison Covid-19 was a mere bagatelle.

However, returns expectations are where things get more challenging because the study period includes a ‘lost’ decade for equities and higher bond yields than are currently achievable.

Historical risk and return for Vanguard LifeStrategy benchmarks over the past two decades show a 100% Equity World ETF returned 5% annually, with a 100% bond portfolio delivering a not dissimilar 3.9%.

However in the last, exceptional decade, 100% Equity World ETF returned 10.4% annually and whilst adding bonds reduced risk, it added a drag with just 3% return

Looking ahead, equities are unpredictable, but a reasonable long term average is a return of 7% annually – doubling your investment after 10 years; given negative Bond yields in Europe, that portion should not be expected to make any meaningful contribution to returns in the next years

How to invest in a Lifestrategy Fund

Vanguard is not exactly selling dreams when you take into account that bonds won’t contribute much to the returns in a 60/40 portfolio, so what are the options?

For your relatives, keep it simple; for yourself, think about the right mix of assets – holding it longer or treating as the core part of your portfolio.

Given negative bond yields, holding a higher proportion of equities could be a solution, if you can stomach losses; since 1988 the chances of losses were reduced below 5% if holding World Equities above 5 years.

However, if you have a short to medium term investment horizon, the 20 to 40% Equity portfolios are probably still the most sensible choices.

Alternatively, adding satellites by having a, e.g. 90% Vanguard LifeStrategy core and 10% satellite portfolio could work as well; adding other asset classes could be a solution for a slightly more complex portfolio – like the Cyclist or the Banker.

Have a look at risk and return profiles of different asset classes over the past two decades.

Show me the Funds

|

Fund |

Income |

|

Accumulating |

|

|

Distributing |

|

|

Accumulating |

|

|

Distributing |

|

|

Accumulating |

|

|

Distributing |

|

|

Accumulating |

|

|

Distributing |

|

|

Accumulating |

|

|

Distributing |

What’s the difference between accumulating and distributing? Here is the answer.

Good Luck and keep’em* rolling !

(* Wheels & Dividends)

Click to visit:

Commentary » Exchange traded products Commentary » Exchange traded products Latest » Latest » Mutual funds Commentary » Mutual funds Latest » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.