Oct

2020

After the storm: Earnings estimates stabilise

DIY Investor

2 October 2020

![]()

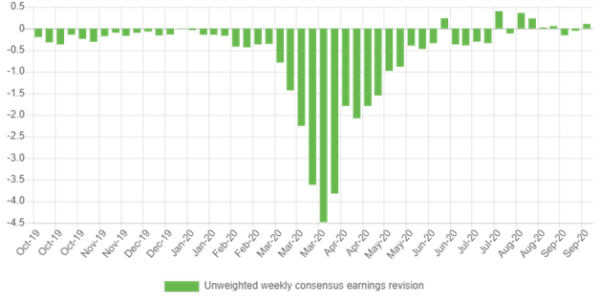

Despite increasing fears of a second wave of COVID-19 infections, consensus 2020 earnings forecasts have remained stable over the past 4 weeks. The COVID-19 downgrade cycle appears complete on a global basis, provided widespread second lockdowns can be avoided.

Exhibit 1: Global COVID-19 downgrade cycle complete

Source: Refinitiv, Edison calculations.

We recognise that the transition away from national government COVID-19 employment subsidies might lead to challenging unemployment data during Q4. However, for now at least there are no adverse trends in consensus revisions.

The new equity market equilibrium in Europe is lower earnings and lower interest rates which in combination result in stable but modestly lower markets compared to the start of 2020. US estimates have held up better during 2020 which may explain in part the relatively better US market performance observed year to date.

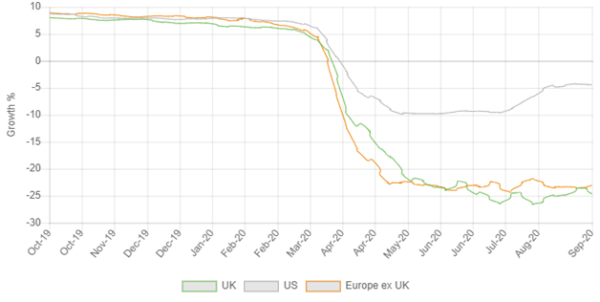

Exhibit 2: US earnings have held up better than Europe

US equities have benefited from smaller downgrades and the remarkable market performance of the “digital defensive” sector.

Although a significant proportion of the US market performance can be attributed to the high weighting of this sector, we note that despite the business interruption caused by COVID-19 the median US earnings forecast is now indicating a contraction of only 5% during 2020.

This compares favourably to Europe where consensus forecasts are now indicating a contraction of 25% for the year. Nevertheless, provided the widespread imposition of second-wave lockdowns can be avoided, the greater cyclicality of European equities may now count in their favour as investors look towards recovery in 2021.

Equity market volatility may be higher than during the exceptionally calm period prior to COVID-19, but as profit forecasts have stabilised volatility has fallen to a fraction of the peak levels seen earlier in the year.

The combination of a degree of stability in the fundamental outlook combined with relative market calm may also incentivise increased capital markets activity, both in terms of IPO and merger and acquisition activity during Q4.

We understand that the recent increase in infections in Europe is a concern and further restrictions on gatherings in the UK (the rule of six) highlight the residual uncertainty in the evolution of the COVID-19 pandemic.

Nevertheless, we believe the declines in European markets and significant lowering of profits expectations to date largely discount these risks. The peak demand for COVID-secure investments may have passed.

We remain neutral on the outlook for global markets in aggregate while becoming increasingly optimistic on cyclical industrial sectors which are insulated from any interruption by COVID-19 social restrictions.

Click to visit:

![]()

Commentary » Equities » Equities Commentary » Investment trusts Commentary » Investment trusts Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.