Jul

2020

Accelerating and emerging trends within U.S. equities

DIY Investor

1 July 2020

Key takeaways

- As we move further through the economic fallout from the COVID-19 pandemic, many pre-existing long-term secular* themes continue to accelerate.

- While a number of industries may face negative long-term impacts, others may be poised to benefit from behavioral changes in the wake of the crisis.

- Companies with stronger balance sheets and ample liquidity may be able to invest and adjust accordingly to emerge in a position of strength relative to their competition.

Long-term secular trends accelerate

In the face of the near-term uncertainty resulting from the COVID-19 crisis, we believe many long-term secular themes remain in place, to the potential benefit of specific industries and companies.

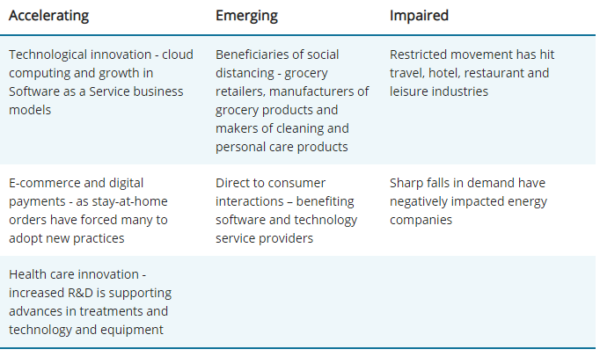

Themes associated with technological innovation, for instance, have in some cases accelerated in the face of social distancing. The shift to cloud computing and growth in Software as a Service business models has been spurred along by a need to provide information technology resources to employees forced to work remotely.

Before the crisis, these themes were providing individuals and enterprises with improved economics, flexibility and ease of use – traits that have led to increased adoption during the crisis, further strengthening the secular trends.

Changes in consumer behavior have also quickened the pace of long-term trends like e-commerce and digital payments, as widespread stay-at-home orders have forced many to adopt these services.

These behavioral changes will likely remain entrenched after the pandemic now that individuals have become more comfortable using the services and accustomed to the conveniences they provide.

‘we believe many long-term secular themes remain in place, to the potential benefit of specific industries and companies’

Payment companies may suffer from lower volumes as a result of spending cuts, rising unemployment and stay-at-home restrictions. However, as the economy recovers, the shift to digital payments should continue to strengthen.

Lastly, the importance of innovation within the health care sector has been heightened by this crisis.

Research and development (R&D) within the sector is driving advances in both treatment for patients and the technology and equipment used by health care professionals, leading to increased safety and productivity.

Health care companies that are improving treatments and outcomes for patients and providing more economical medical solutions should be pos itioned for success once we emerge from the crisis.

Other industries may be permanently impaired

In the wake of an historic shutdown of commerce driven by restrictions on people’s ability to travel and congregate, a tremendous amount of economic strain has been placed on certain industries.

While some may see a delayed recovery in demand for products and services, others may experience permanent demand destruction.

For instance, despite being recently positioned to benefit from long-term secular tailwinds, the travel, hotel, restaurant and leisure industries may face significant long-term structural change as a result of this crisis.

As we continue to have little clarity around the trajectory of the virus and the ultimate economic impact, companies in these industries have limited visibility into when, or if, demand may return.

‘the travel, hotel, restaurant and leisure industries may face significant long-term structural change as a result of this crisis’

Many will be forced to issue debt through the public markets or borrow cash from the government, repaying the loans through equity ownership stakes, further hampering their recovery efforts.

The energy sector is another area that has suffered and may be permanently impaired. Markets were already burdened with excess supply as a result of an oil market-share war between Saudi Arabia and Russia. COVID-19 has only exacerbated that situation by creating a demand shock leading to further swelling of inventories.

Oil prices have fallen below economically profitable levels for many U.S. energy firms, and companies are being forced to navigate through the crisis by taking on debt, cutting capital expenditures and reducing dividends, among other tactics.

Emerging themes to watch

Some industries, fortunately, have been able to remain stable, and, indeed, some have seen an acceleration in demand as a result of the crisis. Social-distancing restrictions have clearly benefited grocery retailers, manufacturers of grocery products and makers of cleaning and personal care products.

These companies have witnessed an uptick in demand as consumers stock their pantries, preparing to stay at home for an extended time. These industries should continue to be positively impacted for as long as people will be forced to stay at home and, potentially, after, depending on how consumer habits change as a result.

‘benefited grocery retailers, manufacturers of grocery products and makers of cleaning and personal care products’

Another subset of companies that have profited are those that have been able to forge direct-to-consumer relationships. With restrictions on non-essential businesses, those with remote engagement capabilities have enjoyed an advantage, in industries as diverse as footwear and insurance.

These companies control their own destiny, so to speak, by dictating the interactions with their customer.

Indirectly enabling those relationships are software and technology service providers, including consultants, who have worked with companies to help them through the process of digitization.

Companies that have forged or strengthened direct-to-consumer bonds during the crisis, as well as the software and technology service providers needed to support them, could be well placed to benefit from permanent change in consumer behavior on the other side of the pandemic.

How will secular themes be impacted by the pandemic?

COVID-19 has accelerated and altered the growth dynamic for many companies and industries. Here is a summary of the potential impact on some secular themes:

The value of balance sheet strength

In general, we expect companies with stronger balance sheets and ample liquidity to better adjust to the current environment. And by investing now, these entities could even emerge in a position of strength.

As these companies assess their cash flow levels and liquidity options, some may draw on available credit lines, and others may issue debt in the investment-grade market, which has been active and relatively low cost to date.

‘it is now more important than ever to identify companies that are in a position of financial strength and those in a favorable competitive position’

Their goal is to not only ensure that their balance sheets are in a healthy position to weather the current crisis, but also to invest in marketing and positioning their businesses for growth after the storm. Some entities may even seek to acquire assets from distressed sellers to eventually take substantial market share.

Crises like these generally allow the best-positioned companies to thrive at the expense of those in weaker financial situations. As investors, it is now more important than ever to identify companies that are in a position of financial strength and those in a favorable competitive position to capitalize on long-term secular themes.

*Secular: Secular themes and trends are not seasonal or cyclical. They are long term in nature.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Click to visit:

Commentary » Equities » Equities Commentary » Equities Latest » Henderson Partner Page » Investment trusts Commentary » Latest » Mutual funds Commentary » Mutual funds Latest » Uncategorized

Leave a Reply

You must be logged in to post a comment.